Sen. Cyndy Hyde-Smith (R-MS) introduced legislation developed in cooperation with the National Cotton Council to boost demand for U.S. cotton.

Titled the “Buying American Cotton Act,” this bill would offer a transferrable tax credit to end-stage sellers of products that are made in whole or in part from U.S. cotton.

Under the legislation’s framework, items either fully manufactured in the U.S. or imported into the U.S. would be eligible for the credit, which is scalable depending on the degree of domestic cotton content or cotton processing. In addition, the seller would receive a higher credit for eligible items processed either wholly in the U.S. or in a country with which the U.S. has a free trade agreement.

Agriculture, Nutrition and Forestry Committee Chairman John Boozman (R-AR) has cosponsored the “Buying American Cotton Act,” along with Sens. Katie Britt (R-AL) and Roger Marshall (R-KS).

Buying American Cotton Act of 2025–May 2025

Objective: By leveraging the traceability of U.S. cotton and the purchasing power of U.S. consumers,

the Buying American Cotton Act authorizes transferable tax credits to incentivize the consumption of

U.S. cotton and U.S. cotton manufactured products.

Eligible Articles: Cotton products, including but not limited to apparel, home textiles, and nonwovens,

either fully manufactured in the United States or imported into the United States, that are made in

whole or in part from U.S. extra-long staple cotton or upland cotton.

Eligible Taxpayer: The first U.S. entity who sells an eligible article in the United States in its final

condition, meaning the product is now “ready for sale” at retail to the consumer. The taxpayer may

claim the credit based on the value of the U.S.-grown cotton in the eligible article, or instead, may

elect to claim a higher-value credit based on the value of the U.S.-manufactured yarn or the U.S.

manufactured fabric, if the taxpayer can demonstrate the eligible article was made from U.S.

manufactured yarn or fabric, respectively.

Documenting the Use of U.S. Cotton: Entities claiming the tax credits must be able to demonstrate

proof of U.S. origin through a trustworthy supply chain tracing system that certifies the provenance

and volume of the cotton in the eligible article, or of the yarn or fabric if either of those credit options

are selected.

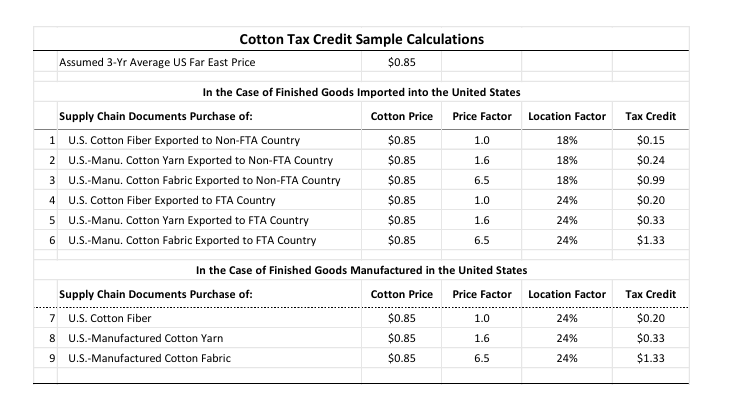

Calculation of the Tax Credits: The value of the tax credit is determined as the product of the volume

of U.S.-grown cotton in the eligible article and a factored percentage of the rolling three-year average

market price. If the taxpayer elects a credit based on U.S.-manufactured yarn, the value is multiplied

by a price factor of 1.6, and for U.S.-manufactured fabric, multiplied by a price factor of 6.5, to

incentivize and reward the consumption of U.S.-manufactured goods.

Factors Determining the Value of the Tax Credits: In the case of an eligible article that is processed

either wholly in the United States or in a country or countries with which the United States has

entered into a free trade agreement or for which the United States has extended benefits through a

preferential trade arrangement, a location factor of 24% is used. In the case of an eligible article that

was subject to processing at any stage in any other country, a location factor of 18% is used.

Tax Credit = (3-Yr Average Cotton Price) * (Price Factor) * (Location Factor)

Sample calculations are shown in the following table.