Dr. Derrell Peel, Oklahoma State University Extension Livestock Marketing Specialist, offers his economic analysis of the beef cattle industry as part of the weekly series known as the “Cow Calf Corner,” published electronically by Dr. Peel, Mark Johnson, and Paul Beck. Today, Dr. Peel discusses drought conditions in Oklahoma.

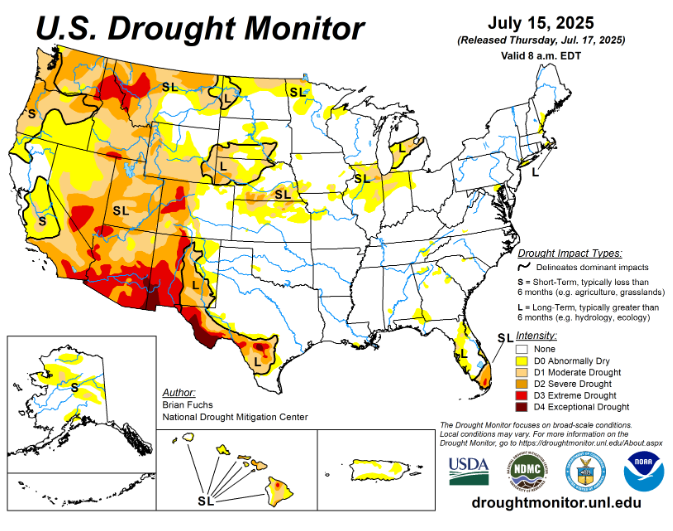

Drought conditions have diminished significantly in much of the eastern two-thirds of the country while drought continues to expand and deepen in the west, Pacific Northwest and across the northern plains areas of Montana and North Dakota (Figure 1). Drought conditions have improved in the past two months in several major beef cow states including Texas, Oklahoma, Kansas, Nebraska and South Dakota.

Range and pasture conditions in the eight western states (AZ, CA, ID, NV, NM, OR, UT, WA) include 39.9 percent poor and very poor conditions, worse than last year and the five-year average for this date. In the Great Plains region (CO, KS, MT, NE, ND, SD, WY), 25.7 percent of pastures and ranges are in poor to very poor condition, higher than last year and the five-year average. In contrast, Texas and Oklahoma have just 15 percent of ranges and pastures in poor and very poor condition, compared to year-ago and five-year averages both over 26 percent for this date.

To what extent is drought limiting efforts or potential to initiate beef cow herd rebuilding this summer? Probably not a great deal and certainly less in total than any time in recent years. Although some producers are still being impacted by drought, most of the current drought regions have relatively low beef cow numbers and would not offset increases in other regions.

By contrast, ample moisture in some regions is resulting in forage production that is outpacing animal grazing. In some cases, excessively wet conditions are hindering hay production, at least in terms of quality, if not quantity. Anecdotal reports from producers and lenders suggest considerable producer interest in retaining heifers but the indications are that the pace is slow. Upcoming USDA reports will hopefully provide more insight into whether and how much herd building is underway.

Heifer slaughter has been declining in recent weeks and is down 3.5 percent year over year thus far in 2025 (down 5.6 percent in recent weeks). Beef cow slaughter is down 16.5 percent year over year. If the current beef cow slaughter rate persists for the remainder of the year, herd culling in 2025 may drop below 9.0 percent, a level that is certainly consistent with herd rebuilding. Taken together, heifer and beef cow slaughter suggest that the beef cow herd may stabilize and possibly increase fractionally by the end of the year.

Feeder and fed cattle markets have shrugged off the summer doldrums and moved higher in the past week. Choice boxed beef prices, which pulled back about five percent from the late June highs, stabilized last week and will likely move mostly sideways through the heat of the summer. Cattle prices are expected to remain very strong with muted seasonal tendencies in the fall.