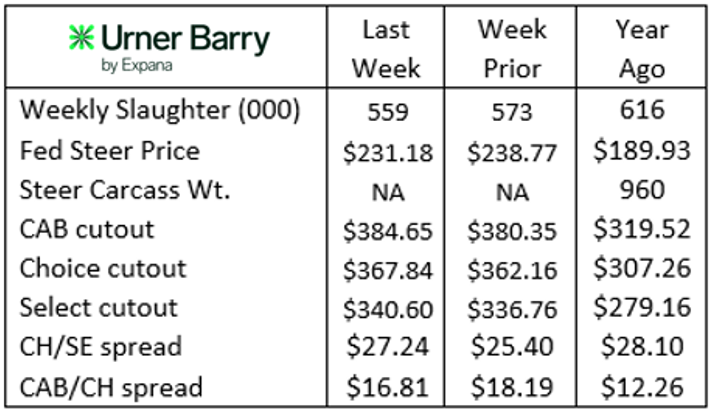

Last week’s federally inspected cattle harvest was 14,000 head smaller than the prior week at 559,000 head. However, the last three weeks have averaged 11,000 head more than the prior four-week period. Prices ranged from $230/cwt. to $235/cwt. with the average steer price at $231.18/cwt. This week, early indications hold promise for a steady to slightly stronger trend. Early November cash fed cattle have trended either direction in the past few years. The complexity of current market conditions suggests that historical trends are of little importance. As basis has turned positive, fundamental supply and demand rule the day. Political rhetoric has, so far, proven to be just that, with no actionable changes to the demand-driven market. Downward pressure on futures this Wednesday is firm, however, and will challenge the cash market mentality.

Since headlines fell upon the beef complex October 16, fed and feeder cattle values have taken it on the chin. Feedyards watching the board for their opportunity to hedge their recent “unhedgable” feeder cattle purchases will be forced to wait it out as upper $240’s futures values vanished amidst a stout uptrend. Typically, large October feeder cattle market runs reflect the futures fallout as well. Even so, the latest report shows 550 lb. feeder steers valued at $555 per head more than at the beginning of the year. Boxed beef cutout values are behaving in line with seasonal expectations following a dramatic correction down from the early September high. This is reasonable given percentage changes on prices at least 20% higher than a year ago have resulted in big swings in actual dollar values. Even so, the uptick toward fourth quarter highs has begun with great middle meat demand leading the way. Price trajectory for ribeyes, tenderloins, strip loins and sirloins have all been quite bullish to the cutout values. Grind values have been unseasonally higher, as have peeled knuckles (from the round), with demand apparently the driver under more positive supply of 90% lean trim.

Quality is the Hedge

The past two weeks have brought about much emotion and even more misinformation surrounding U.S. beef economics. The focus of recent market commentary has primarily featured import tariffs and tariff quota adjustments as a political bargaining chip. Undoubtedly, global supply of lean grinding beef is important to the U.S. consumer, with 53% of per capita beef consumption assigned to the ground beef category. With domestic cow harvest volume down 30% from the cycle high, supplemental imports of 90% lean grinding material have been necessary to fulfill U.S. consumer demand. The mere discussion of shifts in this supply has created uncertainty in cattle futures prices, consequential to the cash market as well. What many are missing in the discussion is the fact that North American grain fed steer and heifer carcasses are vastly different than beef produced elsewhere. Sure, advancements in beef genetics and grain based diets have evolved, to an extent, in countries that have been primary import sources for U.S. beef. Yet fed steer and heifer carcasses produced in the U.S. (and Canada) hold the enviable position of the most preferred product not only domestically but across the globe. Of course, competition in the lean grinding cow beef category is a significant economic factor for our producers. Record-high 90% lean beef prices have made those domestic cull cows a historically profitable revenue source in the past few years. The commodity end of the beef market features products like lean grinds that are easily substituted from different sources and even countries. As a contributor to nearly half of the per capita beef consumption, this is not to be ignored and certainly hasn’t been in the recent few weeks.

This discussion leads to an important point. A few decades of advances in carcass quality have created an insulating factor for our fed steer and heifer product, by comparison. Spectacular quality achievements on the part of our collective producers have culminated in unmatched domestic and global beef demand for our product, especially as volume compared to other large exporting countries is accounted for. The fact that some $400 per head of fed cattle value can be attributed to exports stands as proof that consumers in an ever-growing number of countries demand high quality U.S. beef. This is a synopsis of what a branded product, like Certified Angus Beef ®, can accomplish. When customers come to expect a repeatable eating experience where product quality, satisfaction and safety are built in, demand will only increase. USDA Choice and Prime carcasses constitute 84% of U.S. fed cattle production, pulling beef demand sharply higher today than in the late 1990s when USDA Select was roughly half of our supply and beef demand was at a modern day low. The Certified Angus Beef ® brand now constitutes nearly 25% of U.S. fed cattle production. Ten carcass specifications and a label that has become recognizable by 84% of consumers have carved out a premium space in the market that is not easily substituted. It’s the achievement of cattlemen and scores of downstream suppliers buying in to focus on quality, while competing protein models almost exclusively focus on efficiency and affordability While government policy is not readily in our control, product quality remains a unique advantage that we can continue to use to maintain a competitive moat.