Happy Thanksgiving, everyone. I wish you the best over the holiday. Last week witnessed significant volatility across agricultural futures markets. The markets gave back many of the gains seen on last Monday. Uncertainty over Chinese buying and trade deals in general combined with geopolitical developments kept the futures markets under pressure through the end of the week.

Wheat Market Outlook:

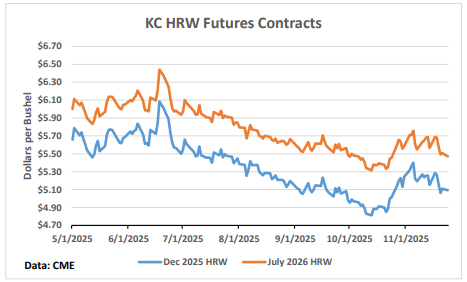

KC hard red winter wheat prices fell over the last week as they were dragged down by uncertainty that leaned bearish in the wheat market. The KC December HRW futures contract closed Monday at $5.07 per bushel down approximately twenty cents over the last week. Basis in Oklahoma has remained stable in the lower range of the five-year average. A strong carry is still in place between nearby and deferred KC HRW contracts. The Crop Progress report on Monday showed moderate improvements in conditions as planting wrapped up. Recent rains across the Southern Plains may take some drought risk premium out of the market. At present, the market fundamentals look to keep wheat prices range bound.

Exports continue to be a key demand focus for the wheat market. Export sales were released for October 2 last week. Releasing data this delayed does not really impact the market but only confirms the shipments that occurred over the last couple of months. China did buy 4.8 million bushels of white wheat that was reported on November 20. Export inspections on Monday for movements through November 20 came in stronger than the last few weeks at 17.4 million bushels placing wheat 19.6 percent above last year’s pace. This week’s data showed a jump in hard red spring exports out of the Pacific northwest that are headed to our Asian trading partners.

The potential for a peace agreement between Russia and Ukraine appears to be providing weakness as well. While the amount of risk premium in the wheat market pertaining to the Black Sea seemed minimal, the probability of a peace deal shot up and places the larger Black Sea wheat production this year on a more favorable footing if the transportation risk is taken out of their price. Romania and Bulgaria produced particularly good crops this year and look to be particularly competitive for trade in the European Union and the Middle East/ North Africa regions. The Russian crop came in around 3.2 billion bushels, and their trade has been lagging. An expectation of stronger exports out the Black Sea region was in place without a peace deal.

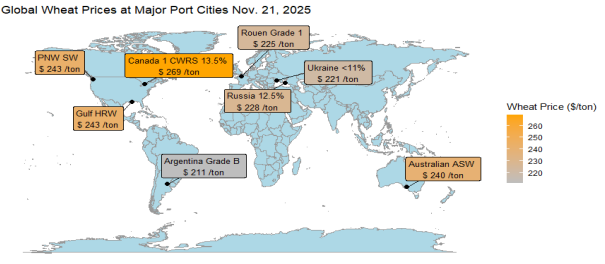

While the 2026 Russian crop is being forecast lower by local analysts by around 150 million bushels on smaller acreage, the world wheat supply looks to remain quite robust over the next year. Reports out of the southern hemisphere place Australian (1.3 billion bushels) and Argentinian (825 million bushels) wheat crops at higher levels as they get confirmation of good yields during harvest. Global prices reflect this reality.

Soybean Market Outlook:

Soybean prices saw massive levels of volatility over the last week. China and South America are expected to dominate the outlook on soybeans despite the potential domestically for crush. Prices drove higher last Monday on growing belief that China would indeed buy U.S. soybeans. China followed through, in a limited fashion, by buying approximately 58 million bushels over three straight days from November 18 – 20. An additional flash sale of 123,000 metric tons was announced on Monday. The total of those flash sales brought soybeans purchased for the marketing year to around 71 million bushels. Sales totals equate to 1.94 million metric tons which is a decent distance from the 12 million metric ton announced as the agreed buying under the trade deal. Doubt on the veracity of the 12-million-ton figure hangs over the market and saw futures give back over forty cents in the January contract over the end of the week. Export inspections through November 20 released on Monday came in at 29.4 million bushels, down by 33 percent from last week and over 60 percent from the same week last year. Reports of continued buying out of Brazil as export prices converged with U.S.

prices do not bring more confidence.

Soybean outlook:

Brazilian crop analysts started to fade the new crop in Brazil recently by bringing the forecast down a couple of million tons. The forecasts range from 177 – 179 million metric tons. Those cuts remain 3 to 4 percent above the old crop estimates that saw massive Brazilian exports to China this year. Planting in Brazil has lagged the typical pace due to irregular rainfall in areas (Bahia, Piaui, and Tocantins). Argentina witnessed flooding in Buenos Aires province, a major growing region, which has planting well behind the five-year pace. South America is approaching crucial periods of the growing season and bears monitoring. Recent weather forecasts indicate potential improvement in the dry areas of

South America that could inject additional bearishness into the market.

Crush continues to be a positive as USDA released the Fats and Oils report on Friday which showed 198 million bushels processed in August and confirmed the old crop estimate from USDA of 2,445 million bushels. When combined with the huge crush number from NOPA for October, the prospects for domestic crush remain bright. The issue with soybean prices remains that we will not crush ourselves out of this situation over the next year. Reward strong price rallies for old and new crop soybean marketing.