PORTFOLIO PERFORMANCE, DIVERSIFICATION, AND STRATEGY

April portfolio yielded 3.66%, up from 3.31% last year, with a weighted average maturity of 792 days.

Total assets under management of $17.9 billion, up $1.5 billion in comparison to April 2024.

Total portfolio contained 64.7% in U.S. Treasurys, 1.7% in U.S. government agencies,

12.8% in mortgage-backed securities, 19.7% money market mutual funds, 0.3% in certificates of deposit,

and 0.8% in state and foreign bonds, comprising the balance of funds invested.

TOTAL FUNDS INVESTED

Funds available for investment at market value include the State Treasurer’s investments at $12,798,077,809 and State Agency balances in OK Invest at $3,254,680,934, American Rescue Plan investments at $1,072,598,967, and the Oklahoma Capitol Improvement Authority Legacy Fund at $795,571,795 for a total of $17,920,929,505.

MARKET CONDITIONS

In April the 2-year and 10-year treasury note yields fell 0.28% and 0.04% respectfully to close at 3.61% and 4.16%. Changes in yields were mixed as middle maturity yields fell, and long-term bond yields were up. The tariff announcement followed by a 90-day pause set the bond and equity markets off on a rollercoaster where the 10-year note moved from 4.01% to 4.48% over the course of the month before settling.

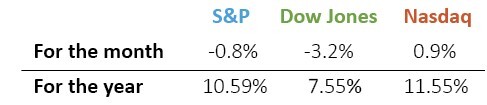

Returns for April show the S&P 500 and Dow Jones fell by 0.8% and 3.2% respectively, while Nasdaq rose 0.9%. Volatility, as measured by the Chicago Board Options Exchange’s Volatility Index, reached the highest level since December 2008 before cooling at the end of the month. Indexes ended mixed after some of the best and worst days on record.

On May 7 the Federal Open Market Committee (FOMC) voted to maintain the current target federal funds rate at 4.25-4.50% and continue reducing the size of the balance sheet. In an official statement the Fed reported that the risks of higher unemployment and higher inflation appear to have risen. The Fed redoubled that unemployment remains low, inflation has come down, and they are well positioned to respond in a timely way to potential economic developments. The Fed seems concerned large tariffs may be sustained, and the inflationary effect could result a one-time shift in the price level. Avoiding persistent inflation will depend on keeping longer-term inflation expectations well anchored to avoid drifting back up and even regaining momentum.

ECONOMIC DEVELOPMENTS

In April, unemployment was unchanged at 4.2%. According to the Bureau of Labor Statistics (BLS), total non-farm payroll employment increased by 177,000 jobs in April, coming in above consensus expectations of 133,000 jobs. Employment increased in health care, social assistance, transportation and warehousing, financial activities, and social assistance. Employment in February and March were revised downwards by a combined 58,000 jobs.

The consumer price index (CPI) rose 0.2% in April, after a 0.1% fall in March, and 2.3% for the year, the smallest 12-month increase since February 2021. The BLS wrote, the index for shelter rose 0.3% in April, accounting for more than half of the all items monthly increase. Annual core personal consumption expenditures (PCE), the Fed’s preferred measure of inflation was 2.6% in March. The producer price index (PPI) decreased 0.5% in April and March was revised to no change. The decline is attributable to prices for final demand services, which moved down 0.7%, the largest decline since the index began in December 2009, per BLS.

Retail sales adjusted for seasonal variation rose 0.1% in April and were revised up to 1.7% for March. There is insufficient statistical evidence that this month’s data is different from zero, given the confidence interval. Sales at home improvement stores increased 0.8% and contributed to the gain. Motor vehicle and parts dealers’ sales were up 9.4% from last year while sales at food service and drinking places were up 7.8% per the Census Bureau.

In March, the National Association of Realtors reported that existing home sales fell 5.9% to a seasonally adjusted annual rate of 4.02 million homes, down 2.4% from last year. Total housing inventory rose to 1.33 million. At the end of March, the average 30-year fixed rate mortgage was 6.65%, down 2.1% from a year ago. The median existing home sales price in March was $403,700, up 2.7% from last year.

The U.S. economy, measured by real GDP, contracted at a 0.3% annualized rate in Q1, in comparison to a Q4 increase of 2.4%. In Q1 trade was a 4.8% drag on GDP growth, the largest effect from net exports since the 1940s. The Bureau of Economic Analysis writes, the decrease in real GDP in the first quarter primarily reflected an increase in imports, which are a subtraction in the calculation of GDP, and a decrease in government spending. These movements were partly offset by increases in investment, consumer spending, and exports.

COLLATERALIZATION

All funds under the control of this office requiring collateralization were secured at rates ranging from 100% to 110%, depending on the type of investment.

Best regards,

View full report below.