Steady demand for operating and feeder livestock loans boosted farm lending at commercial banks in the third quarter. According to the National Survey of Terms of Lending to Farmers, the volume and average size of loans for operating expenses and feeder livestock continued to grow considerably. Demand for larger loans has grown as cattle prices have surged and production costs have remained elevated. Farm loan interest rates decreased slightly, but the drop was less pronounced for feeder livestock loans and rates on those loans remained comparatively higher than other loan types.

Conditions in the U.S. agricultural economy remained disparate as weak crop prices weighed on growers and strong cattle prices boosted profits for many operations. Despite strength in the cattle and other livestock industries, farm financial conditions have deteriorated gradually and weak crop prices moving into harvest could further deplete working capital for many producers. The distribution of assistance from the American Relief Act earlier in the year provided modest support to the sector and financial stress has remained relatively limited, but further deterioration in farm finances and credit conditions is likely in the coming months.

Third Quarter National Survey of Terms of Lending to Farmers

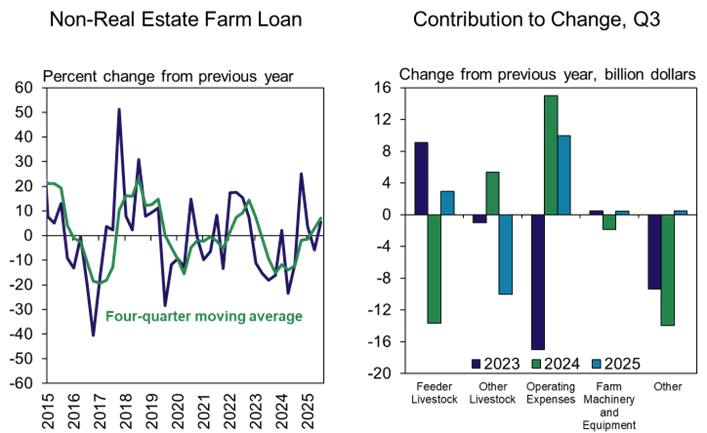

Demand for farm lending at commercial banks appeared to remain strong in the third quarter of 2025. The volume of new non-real estate farm loans was about 7% higher than a year ago following a slight decline during the previous quarter (Chart 1, left panel). Growth during the third quarter was attributed to an increase in operating and feeder livestock loans (Chart 1, right panel).

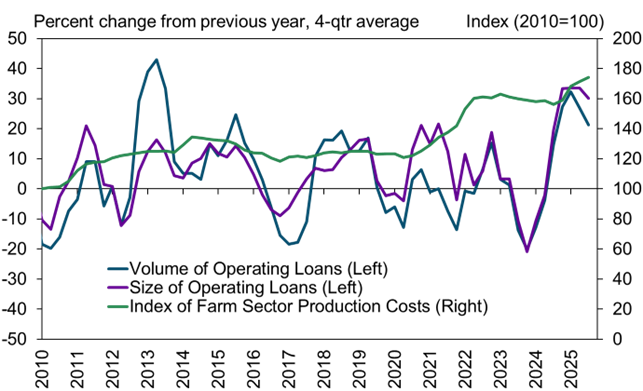

The volume and size of operating loans continued to grow alongside a steady rise in farm production expenses. Production costs measured by the index of prices paid by producers were more than 10% higher than a year ago (Chart 2, green line). At the same time, the average size and volume of operating loans increased at an average pace of about 30% and 20%, respectively.

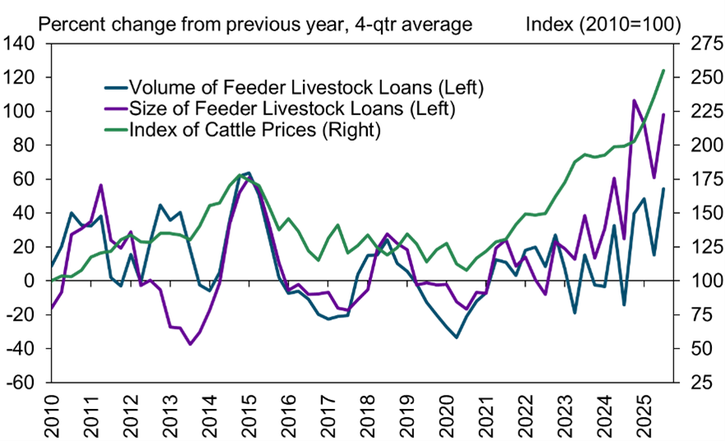

Feeder livestock lending similarly increased alongside significant strength in cattle prices. The average cattle price was nearly 30% higher than a year ago in the third quarter (Chart 3, green line). At the same time, the average size and volume of operating loans increased at an average pace of about 100% and 50%, respectively.

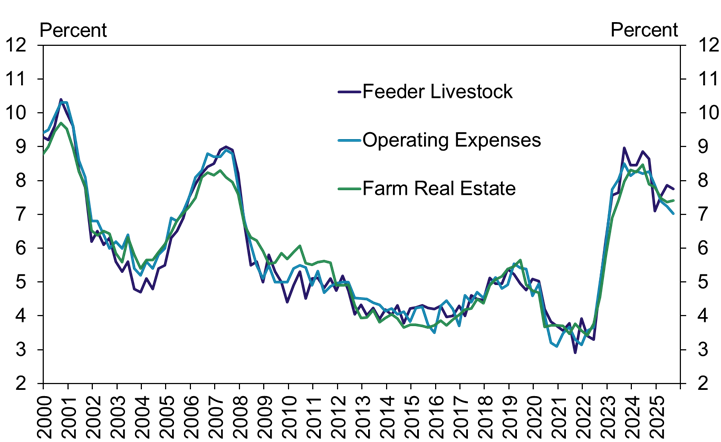

Interest rates on farm loans declined slightly alongside the recent reduction in the target range of the federal funds rate. During the survey period in early August, the average rate on operating loans decreased about 20 basis points from the previous quarter (Chart 4). The average rate on feeder livestock loans declined only 10 basis points. As the size of cattle loans has grown dramatically, the risk of those loans has likely increased and rates on those notes have remained relatively higher than other types.

National Survey of Terms of Lending to Farmers Historical Data

National Survey of Terms of Lending to Farmers Data Tables

External LinkAbout National Survey of Terms of Lending to Farmers Data

Article by Ty Kreitman