As expected by the grain trade, USDA on Wednesday lowered corn export demand 75 million bushels (mb) and also bumped up ending stocks for the crop by 75 mb as well.

USDA trimmed soybean ending stocks to 210 mb, 15 mb from last month’s estimate. USDA lowered its crush estimate by 10 mb but raised its export estimate 25 mb.

USDA on Wednesday released its March Crop Production and World Agricultural Supply and Demand Estimates (WASDE) reports.

You can also access the full reports here:

— Crop Production: https://www.nass.usda.gov/…

— World Agricultural Supply and Demand Estimates (WASDE): http://www.usda.gov/…

WHEAT

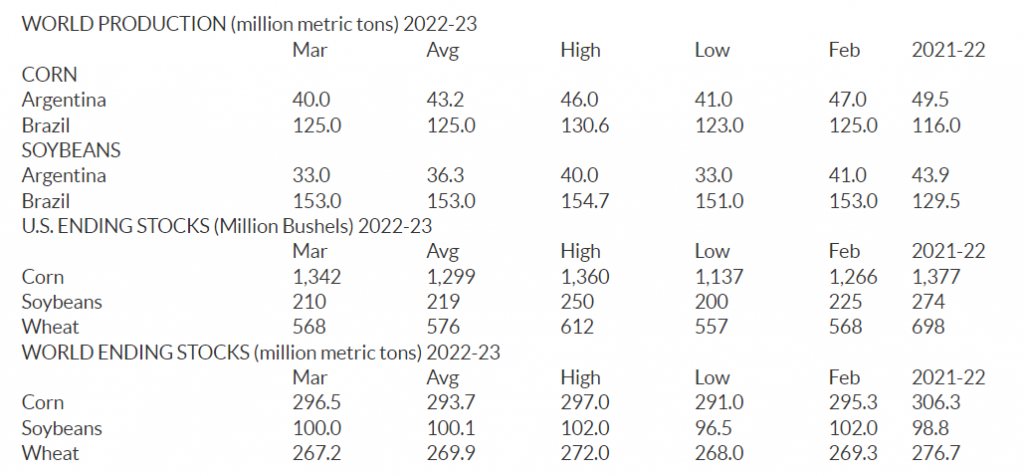

USDA estimates for U.S. 2022-23 wheat ending stocks were left unchanged at 568 mb in March. USDA estimates wheat exports also are unchanged at 775 mb in March.

The average U.S. farmgate price for wheat was pegged at $9.00 in the March report.

USDA estimates world wheat production at 788.94 mmt, an increase from 783.8 mmt in February.

USDA estimates wheat production in Russia at 92.0 mmt, unchanged from February estimates.

Wheat exports from Russia were estimated at 43.5 mmt, also unchanged from February. USDA estimates Ukraine exports at 13.5 mmt. Australian wheat exports were estimated at 28.5 mmt, an increase from 28.0 last month.

USDA’s estimates world ending wheat stocks at 267.2 mmt in March, down from 269.34 mmt in February.

CORN

USDA made one significant change to corn supply and demand in the 2022-23 corn crop.

Export demand was pegged 1.85 billion bushels (bb), a 75 mb decline. That was actually more than the pre-report expectations.

All of those adjustments put corn ending stocks at 1.342 bb — still the second lowest ending stocks in a corn crop over the last nine years.

Production for the corn crop remained at 13.730 bb, the lowest in three years, and yield remained unchanged at 173.3 bushels per acre.

Total supply was held at 15.157 bb.

Feed and Residual use was pegged 5.275 bb. Ethanol use was held pat at 5.25 bb. Total domestic use came in at 11.965 bb.

Total use came in at 13.815 bb, down the 75 mb from exports.

The farmgate price was pegged at $6.60 per bushel, down 10 cents from last month.

Globally, USDA’s 2022-23 beginning stocks for corn were pegged at 305.69 million metric tons (mmt), down .59 mmt. Total production was estimated at 1,147.52, down 3.84 mmt. Global ending stocks for 2022-23 were 296.46 mmt, down 1.18 mmt.

Brazil’s production held pat at 125 mmt for 2022-23 and exports were pegged at 50 mmt. Argentina was pegged at 40 mmt, down 7 mmt and exports were dropped 7 mmt as well to 28 mmt as drought continues to take its toll there. Ukraine’s production held firm at 27 mmt and Ukraine’s exports were increased to 23.5 mmt.

SOYBEANS

USDA trimmed soybean ending stocks to 210 mb. That’s 15 mb from last month’s estimate but within the range of pre-report expectations. USDA left supply numbers unchanged, but lowered the crush estimate by 10 mb and raised its export estimate 25 mb. It also increased the residual use category by 1 mb. The national average farm gate price was $14.30, unchanged from last month.

Globally, USDA lowered its 2022-23 ending stocks estimate by 2 mmt to 100.01 million metric tons, within the range of pre-report expectations. Brazilian production was left unchanged at 153 mmt, while slashing Argentina’s production estimate 8 mmt to 33 mmt. USDA said it raised export estimate for Brazil and the U.S. to accommodate the shortfall in Argentina.

LIVESTOCK

Wednesday’s WASDE report shared exciting news for the cattle and beef markets. Production for 2023 was increased by 170 million pounds, which largely stems from more aggressive beef cow slaughter than originally assumed. The first three quarters of 2023 saw production increases to contribute to the 170 million additional pounds, but the fourth quarter remained unchanged. Quarterly price projections showed a bullish outlook for steer prices as all four quarters of 2023 saw a price increase. Compared to last month, the first quarter was raised by $3.00 to average $161.00, the second quarter was raised by $4.00 to average $163.00, the third quarter was raised by $2.00 to average $159.00 and the fourth quarter was raised by $2.00 to average $164.00. Beef imports remained unchanged at 3,425 million pounds, and exports remained unchanged at 3,090 million pounds.

Wednesday’s WASDE report shared disappointing news for the hog and pork markets. Pork production was lowered from a month ago as higher than previously expected slaughter speeds in the first quarter were more than offset by lighter first half of 2023 carcass weights. Pork production in 2023 fell by 25 million pounds. In terms of quarterly price projections, the market received mixed news as both the first and second quarter of 2023 saw price reductions, but the third and fourth quarter of the year remained unchanged. Barrows and gilts in the first quarter were reduced by $2.00 to average $56.00, prices in the second quarter were reduced by a $1.00 to average $70.00, and both the third and fourth quarter remained unchanged at $73.00 and $64.00. Pork imports remained unchanged at 1,005 million pounds and exports also remained unchanged at 6,350 million pounds.