US Wheat Associates Weekly Price Report for June 2, 2023

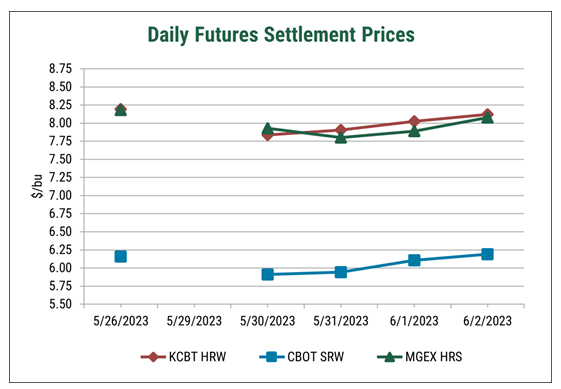

Following the U.S. Memorial Day holiday on May 29, wheat futures ended the week mixed. Futures dipped mid-week, with some contracts reaching lows not seen since 2020. July 2023 CBOT soft red winter (SRW) futures were up 3 cents on the week, closing at $6.19/bu after touching a 30-month low on Tuesday. KCBT HRW futures were down 7 cents, at $8.12/bu. HRS futures were down 10 cents at $8.08/bu. CBOT corn futures were up 5 cents at $6.09/bu. CBOT soybean futures were up 15 cents, at $13.53/bu.

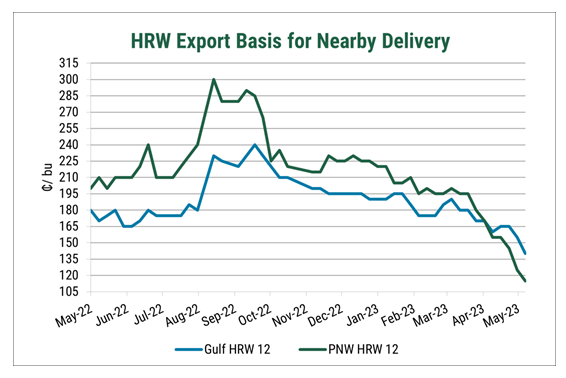

Basis ended the week down for nearly all classes and export regions, as seasonal pressure weighs on the market. HRS basis was unchanged in the Gulf and down in the Pacific Northwest (PNW). Little interest in selling from the farmer and low demand made for an unexciting week, though the PNW basis softened some as exporters repositioned themselves to incentivize buying interest. HRW basis was down in the Gulf and the PNW, weighed by a lack of demand and harvest campaigns beginning in Texas and Oklahoma. The PNW HRW and Gulf HRS spread continues to widen as production prospects remain optimistic in Montana. SRW basis and SW prices continue to decrease, in line with competitor prices though dryness in the SRW and SW growing regions lent some support.

The USDA crop progress report ranked winter wheat as 34% good or excellent, up 3 points from last week and up 5 points from the previous year. Winter wheat rated as fair was 31%, and winter wheat rated poor to very poor was 35%. Winter wheat headed was 72%, up 11 points from last week and practically even with the 5-year average. You can read more about the current wheat harvest progress here.

Spring wheat planting progress has been rapid, with 85% of the crop planted as of May 28, up 21 points from the previous week and hovering near the five-year average. Spring wheat emergence is 57%, a 25-point increase from last week.

Commercial Sales

For the week ending May 25, 2023, net U.S. commercial wheat sales of 466,537 metric tons (MT) were reported for delivery in 2023/24, above trade expectations of 200,000 to 450,000 MT. Year-to-date 2023/24 commercial sales total 2.6 million metric tons (MMT), 21% behind the 2022/23 pace. USDA expects 2023/24 U.S. wheat exports of 19.73 MMT, and commitments to date are 13% of total projected exports.

Areas in Nebraska, western Kansas, and eastern Colorado received two to 10 inches of rain, causing flooding in some areas. Dryness expanded in Washington and Oregon after a month of hot temperatures. Above-normal temperatures will persist in the Northern Plains and PNW, while showers are expected in the Texas Panhandle, southern Kansas, Colorado, and Montana.

The effectiveness of the Black Sea Grain Initiative continues to be questioned as Russia pushes for the transit of ammonia through the Ukrainian port of Pivdennyi in exchange for the continuation of the agreement. Ukraine has repeatedly accused Russia of purposefully impeding inspections by the Joint Coordination Center, which Russia denies. The inspection pace for vessels departing the Black Sea has slowed, and reports indicate that 50 ships await inspection in Turkey.

Heavy rains in China’s major wheat-growing province, Henan, stalled harvest campaigns and may damage the 2023 crop according to trade media. The forecast predicts more rain over the weekend.

Russian wheat prices continue to soften as harvest approaches and global demand weakens. According to IKAR, Russian wheat prices dropped to $230.00/MT from $242.00/MT the week prior.

According to FranceAgriMer, wheat ratings hover at record-high levels, demonstrating the potential for an above-average crop in Europe. An estimated 93 percent of the crop sits in good to excellent condition, well above last year’s 69 percent.

Baltic and U.S. Dollar Indices

The Baltic Dry Index (BDI), which assesses the average cost of shipping raw materials such as grains, coal, and iron ore, experienced a 21% decrease during the week, ending at 919. The market still awaits increased vessel demand from China, though the uptick has not yet materialized.

The U.S. Dollar Index finished the week steady at 104.0. Market sentiment remains mixed regarding the likelihood of an interest rate increase at the June Federal Reserve policy meeting. Economic signals remain mixed. Despite increased employment in Friday’s payroll data, the unemployment rate rose to 3.7% from a 53-year low of 3.4% in April.