Thu, 06 Oct 2022 09:21:26 CDT

The fed cattle slaughter pace continues on a strong course with last week’s steer/heifer total coming in at 521,000 head. Friday’s smaller head count of 89,000 head stood out from the Monday through Thursday pace, which averaged 99,000 head per day. In the most recent three weeks, fed cattle slaughter has been 3.6% larger than last year at this time, with an additional 18,000 head per week processed.

Fed cattle prices have trended slightly stronger in the past three weeks. The six-state fed steer average increased from $142.58/cwt. to last week’s average of $144.06/cwt.

Four of five of the most recent years featured a distinct late summer market bottom in the first half of September before moving higher. The average across all five years shows a 12.5% price increase from the September low to the fall high in early December.

Live Cattle and Feeder Cattle futures have been exceptionally choppy in the past two weeks. Equity market jitters are generating more price pressure to these contracts than supply and demand fundamentals indicate is warranted. The October Live Cattle contract has converged with current cash cattle values in the $144/cwt. area, dropping $2/cwt. since September 21.

Boxed beef values have continued lower in the past two weeks. The market expectation is a short-term bottom in mid-October before cruising higher on holiday rib demand to a late November peak, then drifting down again into the end of the year. However, given the recent concern with the equity markets and the United States’ economic health, there is less certainty about what this year’s fourth quarter demand will be. Consumers may be more apt to save money this holiday season when and where they can, including the meat counter.

Even as questions may arise about fourth-quarter demand, the rib complex moved decidedly higher last week with the CAB rib up $6.35/cwt. The rest of the cuts showed less aggressive price moves, with some end cuts like chuck rolls, chuck tenders and peeled knuckles from the round complex slightly higher. Thin meats are pricing seasonally weaker with inside skirts touching an annual low and outside skirts cheaper as well. Wholesale briskets aren’t a fall highlight for consumers but some may want to keep the smoker handy given the wholesale price point of just $3.15/lb.

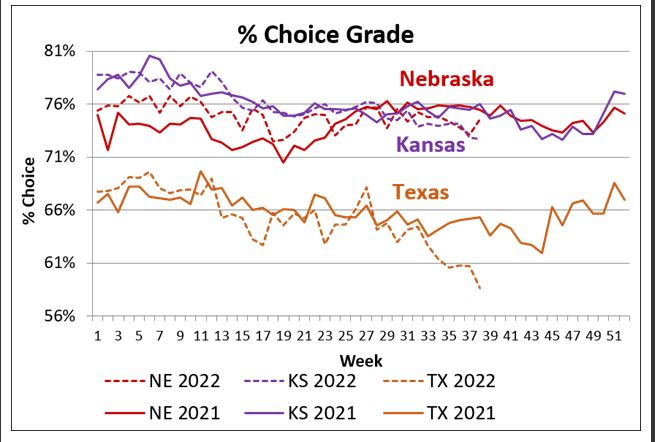

TEXAS GRADE TUMBLES

Following beef quality grade trends may not be as exciting as college football, but for beef marketers quality grade is the game. This season is nothing short of dynamic, as we’ve been waiting on improvement in what has been a subpar carcass marbling achievement across the northern tier of cattle feeding country most of this year.

We hope and expect the fed cattle supply to turn quality higher in late October, when inevitable carcass weight increases pull quality up. Yet, just as we’re nearing the red zone, there’s another snag, and this time it’s not the dip in Prime carcasses in Nebraska that is concerning. Instead, it’s the plummeting Choice grade in Texas that sticks out on the chart.

The improvement in Texas quality grade has been exemplary over the past 15 years, with a 23 percentage point (ppt.) gain in percent Choice, up from 43% in 2007 to 66% Choice in 2021. Granted, Texas is easily the softest hitter when it comes to the Prime category with just 4.3% of fed cattle harvested there reaching Prime in 2021, while the national average touched 10%. Even so, that’s a fivefold improvement from the state’s 2007 Prime grade share.

However, the current trend with the Texas quality grade shows a 5.8 ppt. decline in Choice carcasses since early August. This is a major departure from the trend in a production environment where 2 ppt. changes are impactful. In comparison, the seasonal grade dip since early August puts Nebraska’s Choice decline at just 0.7 ppt. and the Kansas decline at 1.2 ppt. The U.S. total Choice grade was down 1.9 ppt. from early August through the recent late September report. The latest U.S. total percent Choice is 1.4% below a year ago, and 1.7% below the same week in 2021.

Small percentages may seem trivial to most, but they have affected retail and foodservice customers in the market. Large retail grocers intending to feature front page sale ads need to secure large quantities of any beef item before implementing the sale. The retailer needs their entire order (think truckloads) to be fulfilled by the packer or distributor in order to meet their ad requirements. When there is not enough premium product available in the market place to fulfill their specific order, the ad doesn’t run and the supply chain loses a large sale.

What does this mean to cattlemen? First, there is still a need for higher carcass quality achievement in the supply chain despite near-record production of CAB and Prime beef. Second, cattle feeders are again in a position to reap meaningful quality premiums through the fourth quarter. The decline, however slight, in premium grade carcasses has kept the Choice-Select spread elevated, currently at $24.87/cwt. on the USDA grid report. The Prime premium to Choice continues to advance, last quoted at $31.69/cwt. while the CAB premium to Choice is averaging $4.64/cwt. with the top of the range at $8/cwt. again this week.