Cotton at a Crossroads: The United States cotton industry finds itself at a critical juncture, facing a complex landscape of shifting global demand, intense competition from synthetic fibers, and rising production costs. Abigail Hoelscher, a senior market analyst at the Plains Cotton Cooperative Association (PCCA), recently provided a comprehensive overview of these challenges and potential paths forward for the industry.

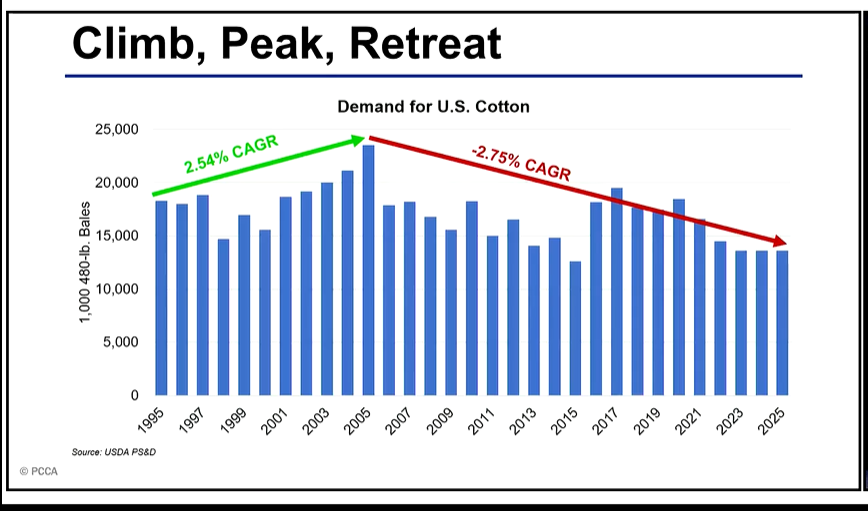

The Shift in Global Fiber Demand

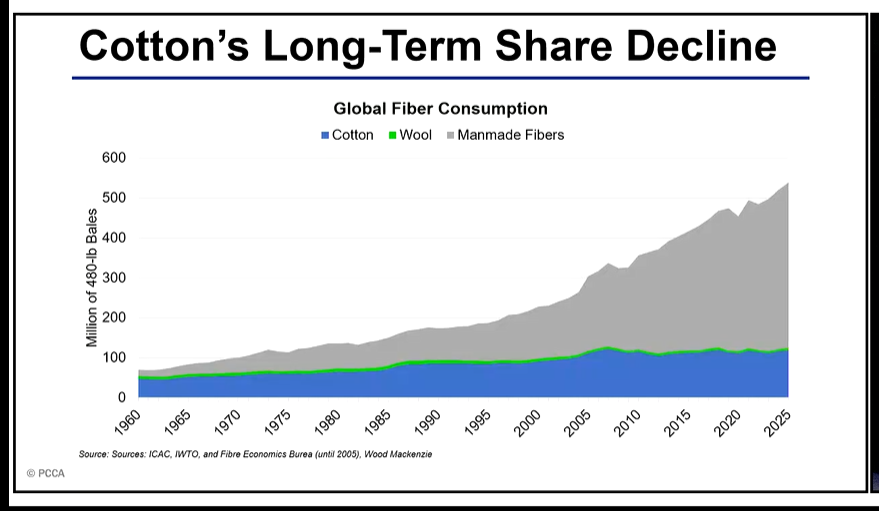

Historically, cotton held the majority share of the global fiber market. However, this dynamic has flipped significantly since the 1960s:

- Market Share Decline: In the 1960s, cotton dominated the market. Today, man-made fibers account for 77% of global fiber consumption, while cotton has fallen to 22%.

- Consumption Growth Gap: While total fiber consumption has surged by 674% since the 1960s, cotton consumption has grown by 150%, reaching approximately 120 million bales today.

- Flatlining Demand: Global cotton demand has largely plateaued at the 120-million-bale mark since recovering from the COVID-19 pandemic, showing only marginal growth.

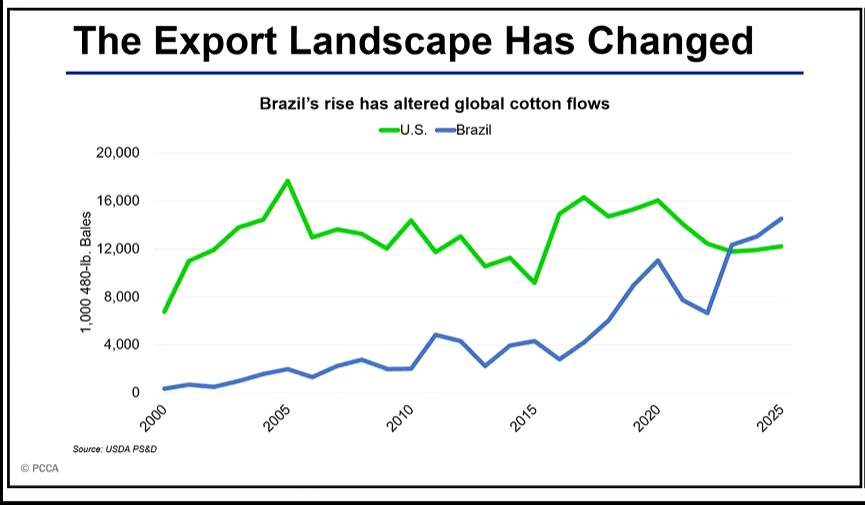

The Competitive Landscape: Brazil and Australia

The U.S. is facing intensified competition from other major cotton exporters, most notably Brazil and Australia:

Brazil’s Rise: In 2023, Brazil surpassed the United States in cotton exports, a significant shift in the global landscape.

Australian Recovery: Australia has seen strong crops in recent years, with both Australia and Brazil currently ahead of their five-year export averages, while the U.S. lags behind.

Currency Factors: A strong U.S. dollar compared to currencies like the Brazilian Real has made Brazilian cotton more price-attractive on the international market.

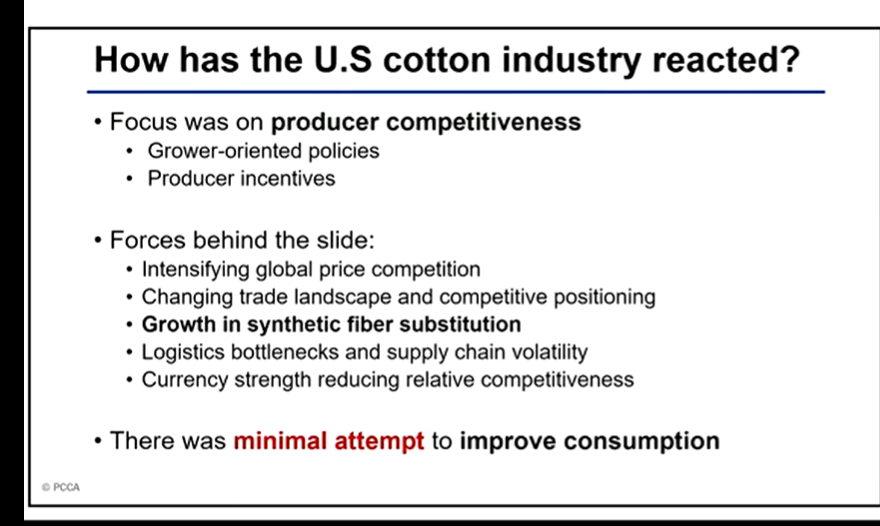

The Domestic “Cost Squeeze”

For the U.S. cotton farmer, the primary challenge is the escalating cost of production:

- Rising Expenses: Production costs for U.S. farmers have increased by 164% since 1997.

- Seed Costs: Seed costs have skyrocketed by nearly 600% over the same period.

- Efficiency Gap: While production costs have risen by 80% since 1997, yields have only increased by less than 20%, leading to a significant cost-efficiency problem.

- Regional Variation: Depending on the region and irrigation methods, U.S. production costs range from the high 60s to 80 cents per pound, whereas Brazil and Australia remain consistently in the 60-cent range.

The Synthetic Threat and Overcapacity

The primary competitor for cotton is not just other growers, but synthetic fibers like polyester:

- Price Advantage of Synthetics: Hoelscher notes that cotton hasn’t necessarily become more expensive, but polyester has become significantly cheaper on the global marketplace.

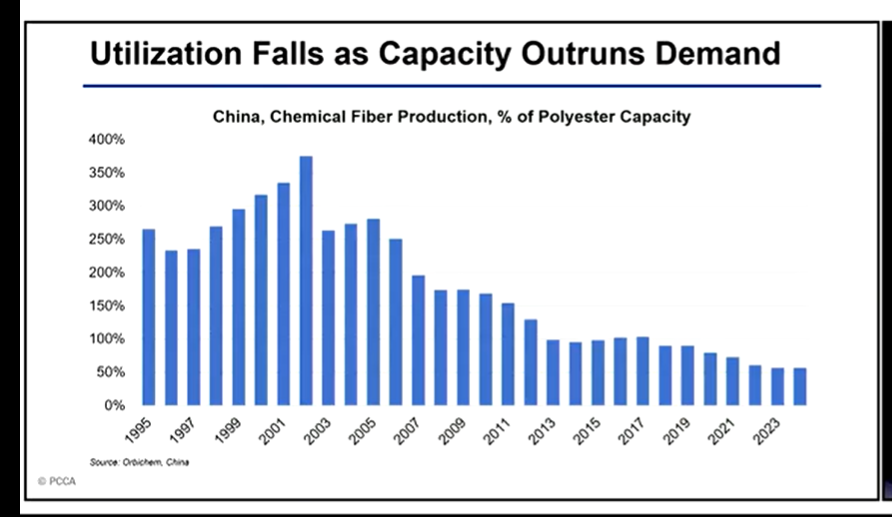

- China’s Role: China has transitioned from a major importer of PTA (the primary feedstock for polyester) to a major exporter.

- Structural Overcapacity: China built polyester production capacity faster than its own demand grew, leading to a structural overcapacity that may require policy intervention or industry consolidation to correct.

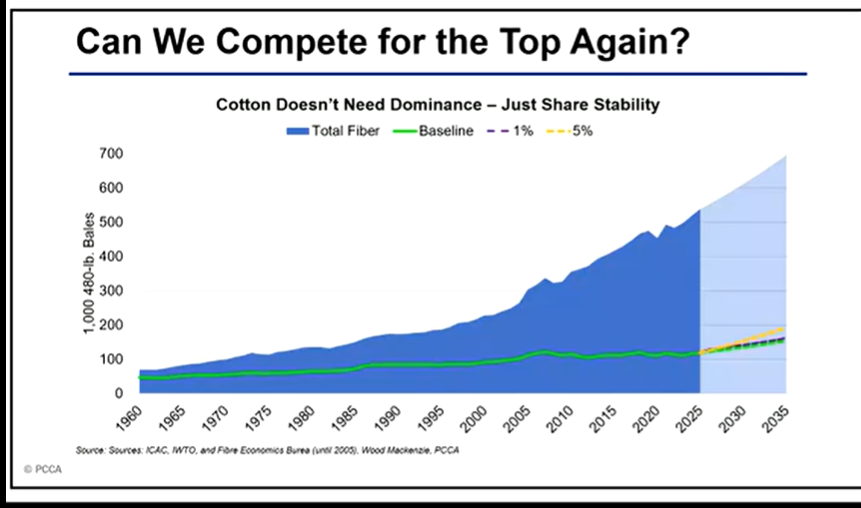

Looking Ahead: Policy and Consumption

Despite these challenges, Hoelscher highlights several factors that could stabilize the industry over the next decade:

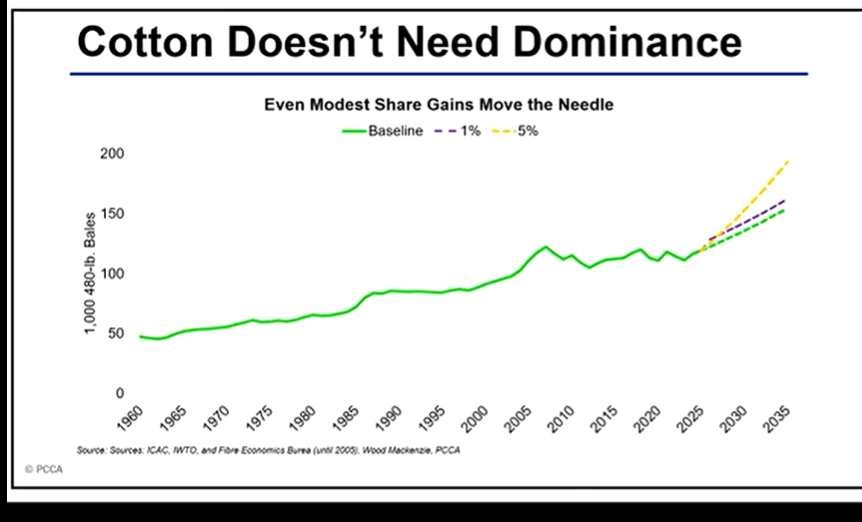

- Policy Support: Initiatives like the Buying American Cotton Act (BACA) could provide a retail tax credit for U.S. cotton content, potentially increasing domestic consumption by approximately 4 million bales.

- Market Positioning: The industry’s future may depend on its ability to compete with synthetics and improve its market share.

“We’ve created a margin in the system… but who is actually benefiting from this? How much is going back to the grower? …That’s something that needs to be re-evaluated as well.”

Hoelscher concludes that the next decade will not be decided by a single crop or policy, but by a combination of policy support, market positioning, and the ability of U.S. farmers to remain cost-competitive in a volatile global landscape.