Grain markets experienced a significant rally over the past week, reaching price levels not seen since last summer. According to Dr. Todd Hubbs from Oklahoma State University, the upward movement in major grain commodities followed a sharp increase in oil prices triggered by the ongoing Iran conflict.

As optimism for a quick resolution to the conflict fades, West Texas Intermediate (WTI) oil has moved higher. Simultaneously, equity markets lost value following a weak jobs report last Friday, signaling potential economic fragility. This combination of high energy prices and slow growth has reignited discussions regarding stagflation, though the outcome remains contingent on how markets continue to respond to geopolitical developments.

Wheat Market: Technical Rallies and Export Questions

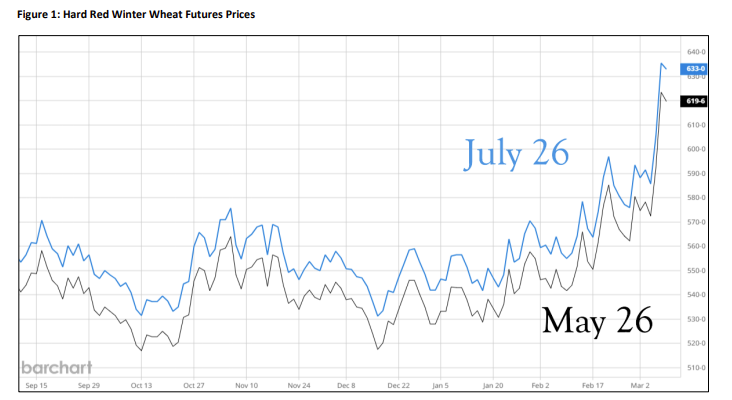

Wheat futures saw an explosive move last Friday, with prices breaking out of their recent range to climb above $6.00. The rally was underpinned by the Iran conflict, concerns over commodity trade flows, and rising fertilizer and energy costs.

Despite the price surge, Dr. Hubbs notes that the rally appears more technically driven than grounded in supply-and-demand fundamentals. While the KC hard red winter wheat March contract closed at $6.19 (up 44 cents from the previous week), actual buyers in the cash market have not yet stepped up to validate these higher levels.

Key Wheat Market Factors:

- Acreage and Production: Statistics Canada projected 2026 wheat acreage at 26.74 million acres, slightly exceeding trade estimates.

- Regional Weather: Drought remains a concern for winter wheat in the Southern Plains, as many areas received sub-optimal precipitation recently.

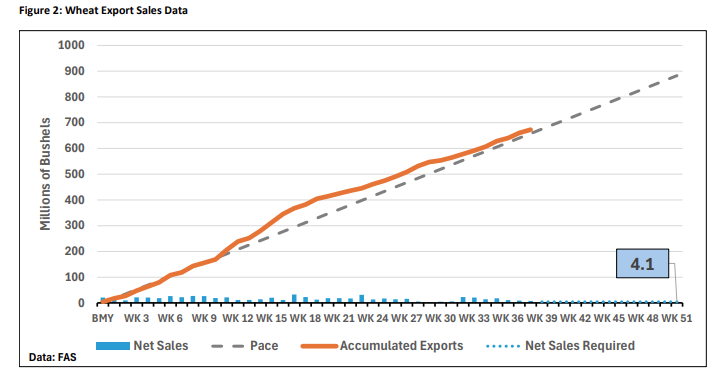

- Export Pace: Total wheat commitments sit at 845 million bushels, with net sales averaging 8.2 million bushels over the last two weeks—a decline from the 15.7 million bushel average seen in the month prior.

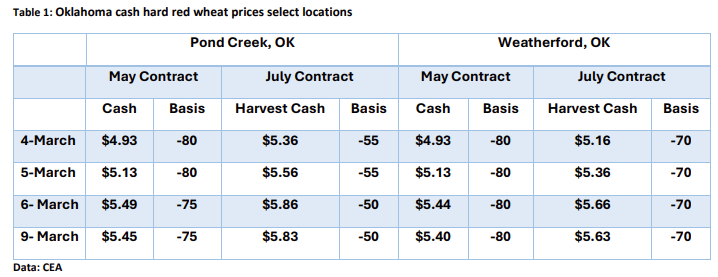

- Oklahoma Cash Prices: In locations like Pond Creek and Weatherford, basis strengthened slightly on Friday, but not enough to definitively support the massive three-day rally.

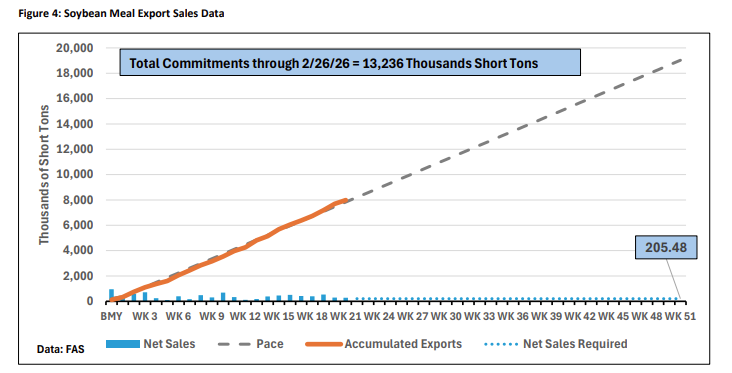

Soybean Market: Biofuels and Crush Demand

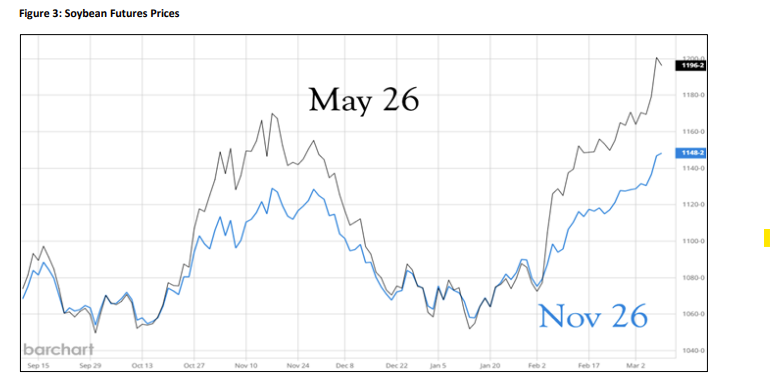

Soybean futures have also strengthened, surpassing levels seen last November. This momentum is largely attributed to rising diesel prices, which have made renewable diesel and biodiesel more competitive. Speculation surrounding new biofuels policy under the Renewable Fuels Standard (RFS) has pushed soybean oil prices above 65 cents per pound.

Soybean Market Outlook Highlights:

- Record Crush Potential: Domestic soybean crush is on a record pace. If this continues, totals could exceed 2.6 billion bushels, requiring an upward revision in the USDA’s WASDE forecast.

- Export Struggles: While domestic demand is high, soybean exports are unlikely to reach the USDA’s 1,575-million-bushel forecast. U.S. total commitments currently sit at 84% of the projection, lagging behind the typical 92% seen at this time of year.

- Global Competition: Brazilian port prices remain significantly lower than U.S. prices. With the Brazilian harvest 51% complete on a 6.6-billion-bushel crop, the U.S. faces stiff competition for international buyers.

Looking Ahead

The market’s attention is now turned toward the March WASDE report. While major shifts are unlikely today, significant volatility is expected to persist as the industry moves toward the pivotal March 31 reports. Traders and producers alike are watching to see if domestic crush demand can offset the current lag in export sales.