Commodity Market Overview Commodity markets remain focused on the Iranian conflict showing lots of market volatility. Closure of the Strait of Hormuz staunched the flow of energy and fertilizer products out of the Gulf. Uncertainty around the activities in this conflict remains elevated. Volatility around public announcements and events in the region will impact prices for the near future.

Monday began with weakness in soybeans due to uncertainty around the scheduled meeting between the U.S. and China. It then snowballed into a massive rundown across the grain and oilseed complex. Last week’s WASDE release contained minor changes as is common during the March release. The focus of the market on government reports sits directly on the Prospective Plantings and Grain Stocks reports due out on March 31.

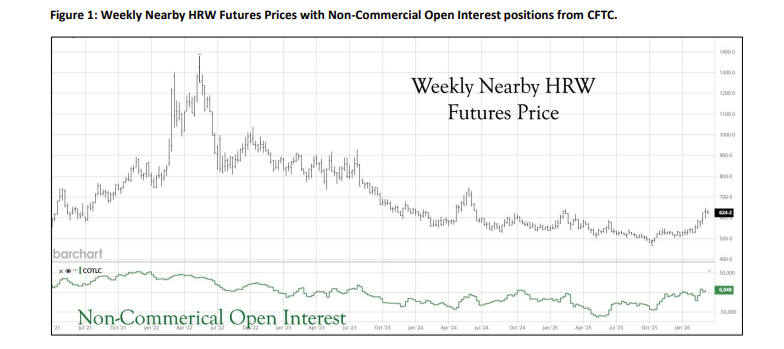

Wheat Market Outlook Futures prices across the wheat complex moved higher last week on war concerns. An influx of speculative money into the commodity sector saw open interest from large speculators hit 52-week highs over the last three weeks in the grain and oilseed futures markets. Monday witnessed a massive selloff which took back most of the gain from the previous week.

Open interest in hard red winter wheat by large non-commercials (often a proxy for speculators and index funds) increased to levels not seen in a few years. The closing of the Strait of Hormuz to sea traffic created a bullish scenario for the energy and petrochemicals. Energy price shocks bring with them the specter of higher inflation and slower economic growth. Speculators take positions in commodity funds that act as a hedge against inflation in investment portfolios.

While geopolitical issues crowd out information on fundamentals in hard red winter wheat markets, weather remains an issue. Dryness continues to impact large swathes of the Southern Plains with rapidly changing weather conditions bringing the potential for crop issues into play. The demand situation both domestically and around the world remains stable for now. A lengthy continuation of the conflict will create issues with sourcing grain for importers in the Middle East region.

WASDE and Domestic Wheat Data In last week’s WASDE report, USDA moved global ending stocks lower on minor adjustments. Production in Ukraine increased one million metric tons (MMT) to reach 24 MMT. Argentine wheat exports increased 1.5 MMT on a stronger pace, while European Union exports fell by 1 MMT. Ukraine and Russian exports were dropped by half a million metric tons each.

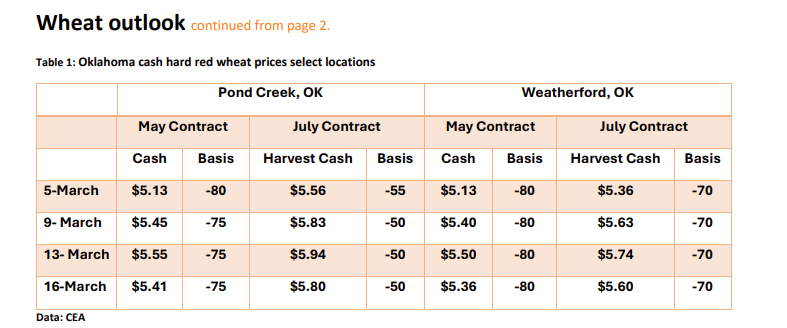

Domestically, U.S. wheat balance sheets were left untouched. Both hard red wheat and all wheat exports remain on track to hit USDA forecasts. Last week’s export sales report placed HRW total commitments through March 5 at 306 million bushels, which is 94 percent of USDA’s forecast. May HRW futures closed at $6.16 on Monday after climbing as high as $6.38. July harvest contract prices closed at $6.30.

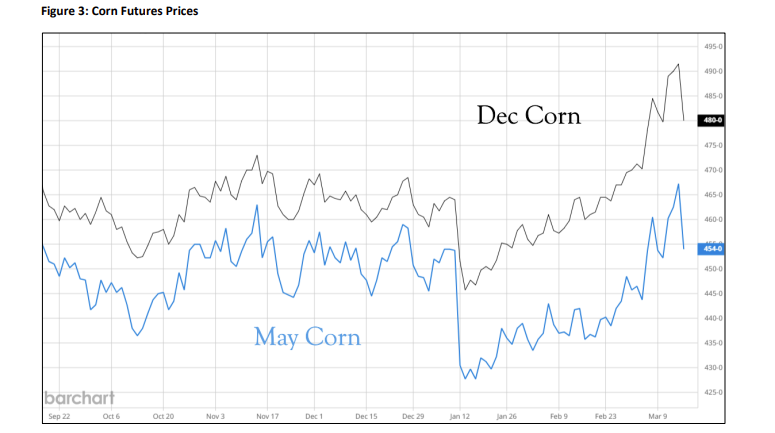

Corn and Milo Market Outlook Corn demand remains consistent with healthy export levels and ethanol grind maintaining the pace to hit USDA’s forecasts. USDA’s recent WASDE report left the domestic corn balance sheet unchanged, though global ending stocks for 2025-26 increased by 3.8 MMT to 292.75 MMT.

December corn futures gave back most last week’s gains on Monday, settling at $4.80 per bushel. Higher oil prices should boost blending of ethanol, but the geopolitical nature of this rally makes it tentative. Oklahoma cash prices for delivery on new crop settled at $4.40-$4.50 on Monday.

Milo cash prices ranged from $3.39 – $3.49, while harvest prices ranged from $3.70 – $3.85. USDA made minor changes to the milo domestic balance sheet, increasing food, seed, and industrial use by five million bushels, offset by a five million bushel drop in feed/residual. Export sales data place total commitments of milo at 163 million bushels through March 5, with the potential for reaching USDA’s 225-million-bushel forecast remaining dependent on Chinese buying.