The global agricultural landscape is currently navigating a period of rare intensity as energy price shocks, geopolitical conflict, and persistent environmental challenges converge. According to Dr. Todd Hubbs of Oklahoma State University, the ongoing conflict with Iran has generated a level of market volatility and uncertainty seldom seen, with global oil prices showing no signs of returning to pre-war levels.

Farm Director KC Sheperd notes that these external pressures are filtering directly down to the farm gate, influencing everything from input speculation to daily cash bids across the Southern Plains.

Energy Shocks and Economic Headwinds

The energy crisis has hit Europe, the Middle East, and Asia with particular severity due to their heavy reliance on regional energy sources. Currently, Brent crude continues to trade at a significant premium over West Texas Intermediate, while natural gas prices in Europe and Asia remain elevated.

This environment of higher costs and slower global growth has set a negative tone for the broader economic outlook. In the agricultural sector, grain and oilseed prices have largely mirrored the movements of the energy complex. Speculators are increasingly entering the commodity markets as a hedge against inflation, while concerns over fertilizer availability and costs continue to cast a shadow over potential acreage shifts and future yields.

Wheat Market: Supply Uncertainty and Drought

Wheat fundamentals have remained relatively stable over the past month, but supply concerns for the next marketing year are intensifying. The Southern Plains remains gripped by drought, with 55 percent of the winter wheat crop currently affected.

Forecasts for the end of March offer the next possibility for rain, though current models suggest the moisture may follow previous patterns this year, potentially missing areas west of I-35 in Oklahoma. Key observations for the wheat market include:

- Export Progress: Total wheat commitments stand at 870 million bushels, keeping the industry on track to meet USDA forecasts.

- Acreage Expectations: The upcoming March 31 Prospective Plantings report is expected to show a decline in spring wheat and durum acreage, with industry estimates hovering around 11.8 million acres compared to last year’s 12.175 million.

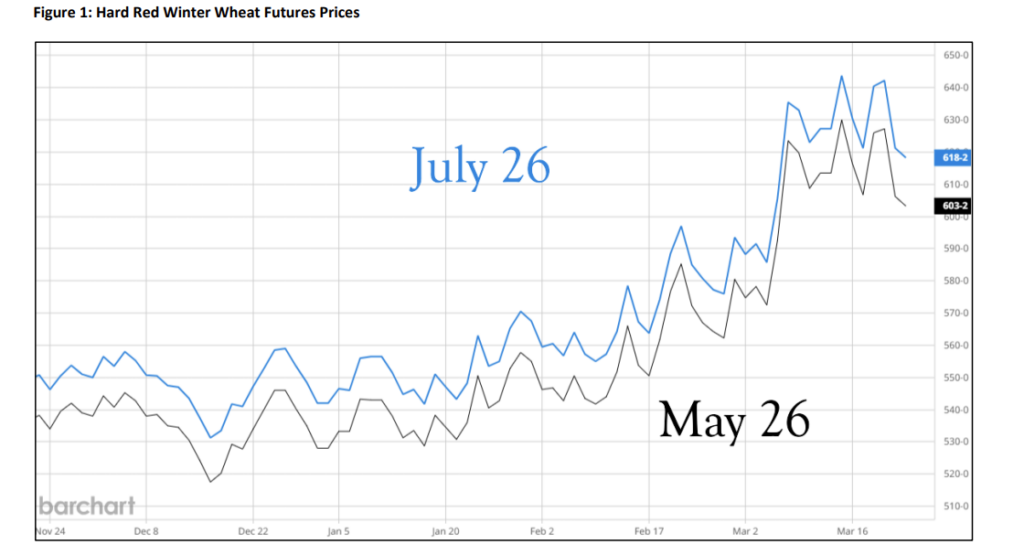

- Price Movements: KC Hard Red Winter (HRW) wheat futures have been erratic. While prices saw a slight retreat following reports of potential negotiations with Iran, the May contract recently closed at $6.03, with July harvest prices at $6.18.

In Oklahoma, cash prices reached the mid-$5.50 range for spot delivery, with some locations seeing July delivery bids as high as $5.97. Producers are encouraged to set target prices and keep bids current to take advantage of potential price spikes in overnight trading.

Soybean Market: Domestic Crush vs. Export Lag

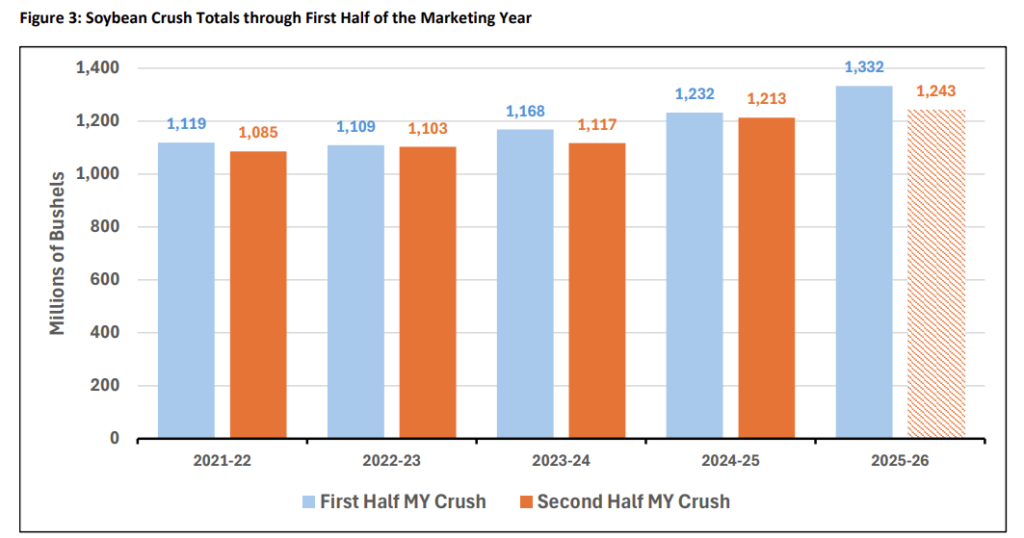

The soybean complex is finding its strongest support from the domestic crush sector rather than international sales. Driven by expectations of supportive Renewable Volume Obligations from the EPA, the U.S. soybean crush is moving at a historic pace. Through February, the crush totaled an estimated 1,332 million bushels, an 8.1 percent increase over the previous year.

However, the export side of the ledger remains a point of concern:

- Export Gap: Total commitments currently sit at 86 percent of the USDA projection, trailing the five-year average of 91 percent for this time of year.

- Global Competition: While there is hope that China may increase U.S. buying due to shipping slowdowns in Brazil, U.S. Gulf prices remain $38 per ton higher than Brazilian port prices, impacting global competitiveness.

- Futures Status: May soybean futures closed at $11.63, struggling to recover fully from a recent limit-down event triggered by doubts over Chinese demand.

As the market awaits the pivotal USDA reports at the end of March, the balance between record-breaking domestic demand for biofuels and a sluggish export pace will likely dictate the next trend for soybean values.