Amidst shifting geopolitical landscapes and the anticipation of pivotal USDA reports, grain markets are experiencing a period of strategic recalibration. Dr. Todd Hubbs, Oklahoma State University Extension Crops Market Specialist, recently discussed the current market trajectory and geopolitical tensions with Farm Director KC Sheperd, noting that while some sectors remain flat, others are finding new momentum.

Wheat Rallies Amid Global Uncertainty and Weather Concerns

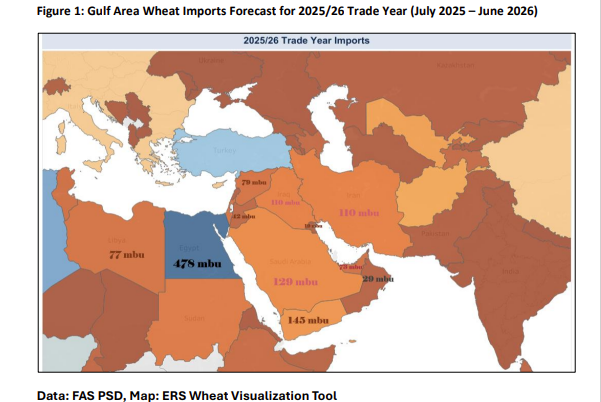

The hard red winter wheat market has seen a recent rally, driven in part by uncertainties surrounding Middle East conflicts. While Dr. Hubbs notes the current situation differs from the massive supply shocks seen previously in the Black Sea, the potential for escalation remains a key factor for Oklahoma producers to watch.

“Those nations around the Arabian Gulf do import a lot of grain, particularly wheat,” Hubbs explained. “One of the big importers is Iran and they get it mostly from Russia. But if it did spread over into the Red Sea area and the maritime shipping lanes over there got impacted, then we’re looking at something completely different”.

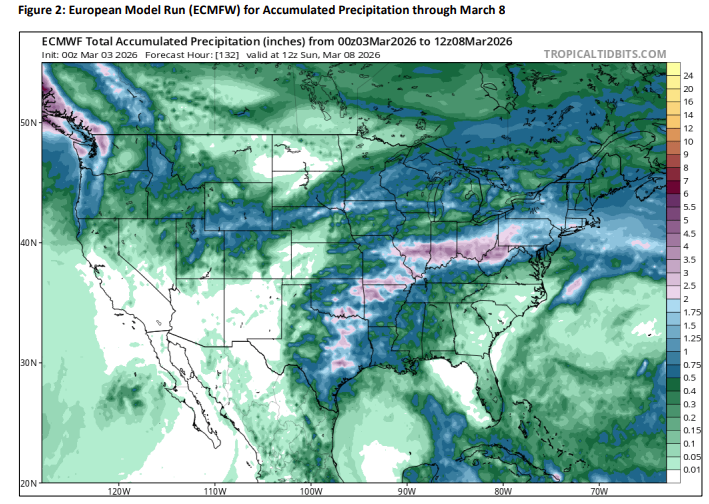

Supporting this rally is a recent report from Statistics Canada, which indicated a decrease of over one million acres in winter wheat planting. Locally, the market is also reacting to abnormally dry conditions. While Eastern Oklahoma has received some rain, Western Oklahoma and Kansas remain short on moisture as the crop comes out of dormancy.

“I would like to see more rain out west in Oklahoma,” Hubbs said. “I don’t feel like we’ve gotten near as much out of these systems so far as I wanted or maybe some people expected”. Hubbs noted that if significant rain does not materialize by the latter part of March, the dry conditions could lead to a realized yield loss.

Biofuels and the Soy Complex

In the soybean market, prices continue to be heavily influenced by biofuel policy and the demand for soybean oil. While the year began with “anemic” demand, Hubbs expects a pickup once volume obligations for the Renewable Fuel Standard are finalized.

This demand is also spilling over into other oilseeds. “This feeds into canola too for the canola farmers here in Oklahoma,” Hubbs noted. “I think canola oil is going to be in hot demand. We’ve seen soybean oil prices move up into the near mid-60s, and I think you’re going to see that continue”.

Anticipation for March USDA Reports

The agricultural community is now looking toward the end of March for the Prospective Plantings and Grain Stocks reports, which will set the tone for the spring. Current market expectations include:

- Corn Acreage: Generally pegged around 94 million acres.

- Soybean Acreage: Expected to land in the mid-80 million range.

- Spring Wheat: Likely to remain flat compared to previous years.

Hubbs cautioned that these initial numbers are rarely the final word. “The changes from the Prospective Plantings report on something like corn acres to the final number have been quite large in the last few years—we’re talking three million acres,” he said.

Producer Strategy: A “Wait and See” Approach

With July wheat contracts nearing the $6.00 mark, the market appears to be “coiling up” for its next move. Hubbs suggests that while the current rally offers pricing opportunities, the high level of volatility and uncertainty regarding spring rainfall makes a cautious approach necessary.

“I’m a sort of ‘wait and see’ mode just because of all this uncertainty and volatility right now,” Hubbs concluded. “But it feels like we’re building a little bit, coiling up a little bit in the wheat market”.