Allendale’s Rich Nelson recently shared insights on the USDA Prospective Plantings and Quarterly Grain Stocks reports with Farm Director KC Sheperd, highlighting key data and market implications. The reports, released on March 31, 2026, offer a comprehensive look at old-crop stocks and initial planting intentions for the 2026 season.

Quarterly Grain Stocks: A Look at Old-Crop Supplies

The Quarterly Grain Stocks report provides a mid-year snapshot of remaining old-crop supplies as of March 1. For corn and soybeans, these figures represent the amount left after two quarters of usage, while for wheat, it reflects stocks after three quarters.

- Corn: Stocks are slightly tighter than previously anticipated.

- Soybeans: There’s a minor increase in the old-crop supply story.

- Wheat: No significant changes were noted in overall wheat stocks.

Prospective Plantings: Initial 2026 Acreage Intentions

The Prospective Plantings report is based on a survey of producers conducted during the first two weeks of March. Nelson noted that the timing of the survey may not fully reflect recent concerns, such as the fertilizer issue that gained prominence in mid-March.

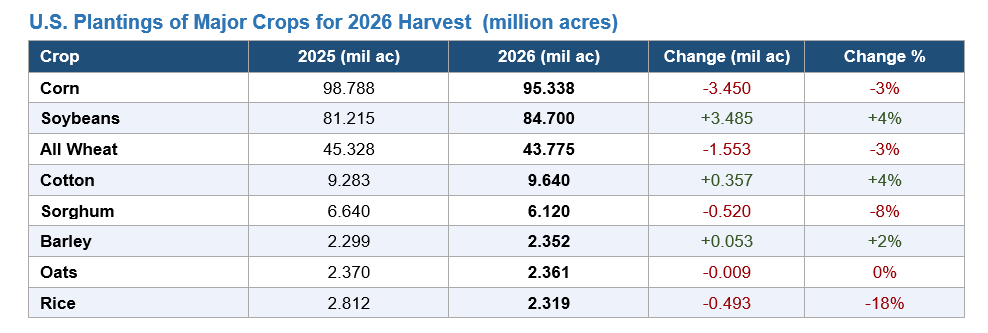

- Corn and Soybeans: The survey suggests a “muted” acreage switch. Corn acres are down approximately 3.5 million, while soybean acres are up by about the same amount. This shift is smaller than the 4 to 4.4 million-acre switch the trade had expected.

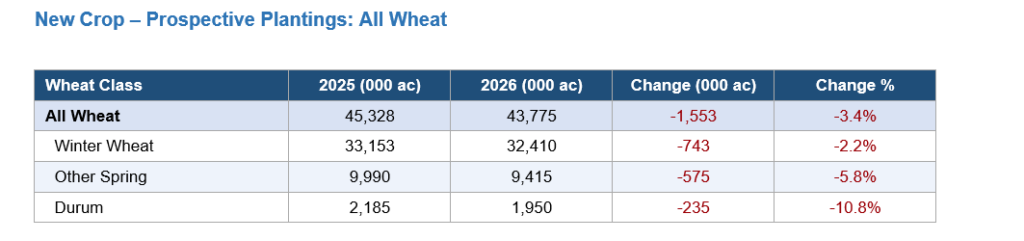

- Wheat: Total wheat acreage is down 1.6 million acres from last year, totaling 43.8 million acres, which is lower than trade estimates.

- Winter Wheat: USDA slightly lowered its acreage estimate from January.

- Other Spring Wheat: A decrease of 575,000 acres was reported.

- Durum Wheat: An additional decline of 200,000 acres was noted.

Market Implications and Pricing

If the market accepts these acreage numbers at face value, Nelson suggests the following price implications:

- December Corn: Approximately $4.70, slightly lower than current levels.

- November Soybeans: Approximately $11.80, slightly higher than current levels.

Nelson emphasized that these numbers are a starting point and are “not set in stone”. Further updates are expected with the June acreage survey and as final acreage is incorporated later in the year.

Factors Influencing the Wheat Market

Despite the lower-than-expected wheat acreage, significant price reactions haven’t been seen yet. Nelson believes the focus will shift to yield determination in the coming months.

- Chicago Wheat: Concerns about yield have lessened due to above-normal rainfall forecasts for April.

- KC Wheat (Hard Red): Potential yield issues remain a concern, and the trade will likely pay more attention to this starting next month.

- Global Factors: Energy products and conflicts in the Middle East continue to be significant drivers for the entire commodity sector.

Looking Ahead

The next major update will be the USDA’s World Agricultural Supply and Demand Estimates (WASDE) report on April 9, which will focus on old-crop numbers. New-crop figures will not be introduced until the May report.

For more information and analysis, visit Allendale’s website at allendalehub.com or call 1-800-2-MARKET.

You can also view the full reports here:

— Prospective Plantings and Grain Stocks: