OSU’s Dr. Todd Hubbs writes in his weekly newsletter: USDA’s May reports put a jolt into hard red winter wheat markets as production estimates came in well below market expectations. In general, the initial forecasts for the 2026-27 marketing year held few surprises beyond wheat production levels. Volatility and uncertainty remain prominent. The administration’s announcement that China agreed to purchase $17 billion worth of agricultural products supported the markets on Monday after the initial surge following the May USDA reports faded. The veracity of the announcement remains in question.

Wheat Market Outlook: Hard Red Wheat futures prices moved sharply higher on Monday. July HRW contract prices hit $7.50 after the release of the May Crop Production report but faded over the remainder of the week. July HRW futures broke out of the short-term range of $6.50 – $7.00 only to fall back and hover in the $6.90’s. July HRW closed at $7.03 on Monday.

HRW cash prices around Oklahoma moved above $6.90 on the major price rally but have ended at $6.53- $6.63 range after Monday’s rally.

It seems increasingly unlikely that HRW cash prices in Oklahoma will move through that $6.90 – $7.00 range without a substantial deterioration in spring crop prospects, like corn, or continued trouble for international wheat crops.

Recent crop tours are raising mild questions about the USDA’s dreary production forecast, as a Kansas wheat tour last week pegged yield at 38.9 bushels per acre. Wheat tour participants expect Kansas to outperform the USDA’s 37 bushels per acre. Given the Kansas harvested acreage estimate of 5.8 million acres, the crop tour estimate would add 11 million bushels of wheat to the count. Given drought stress and other issues, one should not count those bushels before they are harvested.

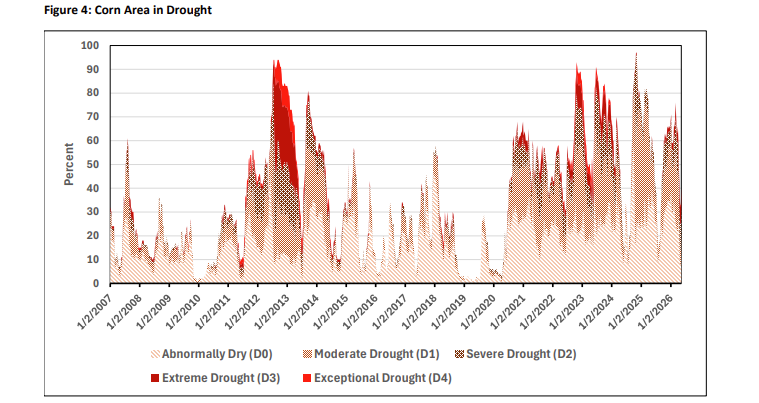

Last Thursday’s drought readings for May 12 placed 71 percent of the winter wheat crop in various levels of drought, with expansion in the extreme drought category by two percent to seventeen. This is the third week in a row that the extreme drought category has increased. Since mid-January, the drought footprint for winter wheat has expanded by 30 percent. USDA crop conditions continue to deteriorate amid the drought.

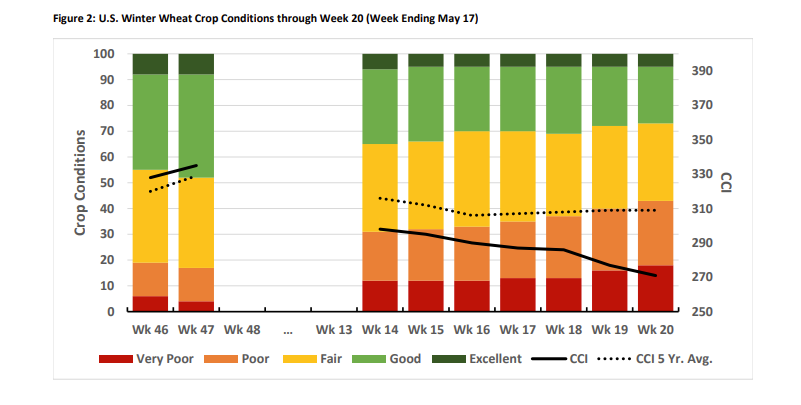

The crop condition ratings for Week 20 (through May 17) are presented for U.S. winter wheat. The percentage of the national winter wheat crop rated good or excellent fell one percent to 27 percent this week. Oklahoma’s good and excellent categories tallied 12 percent, a slight decline from last week. Kansas totaled 15 percent good and excellent. In terms of a commonly used crop condition index, the national index fell 6 points to 271 from last week’s conditions and sit well below the five-year average for this week of the year.

Hard red winter wheat export pace continues to show decent demand despite all the uncertainty. Export data for HRW remains on pace to hit USDA’s 320 million bushels as we close the marketing year. Outstanding sales for the next marketing year come into focus with export sales data through May 7 showing HRW sales at 11.5 million bushels, down from 28.5 million at this point last year. Mexico is on record for holding 4.3 million bushels of those outstanding sales. Taiwan, Korea, and Thailand have 3.9 million bushels of sales. Given the smaller crop, a reduction in exports seems certain. Food usage for HRW remains stable in any given marketing year.

The potential for HRW prices to take another leg up may rely on production elsewhere. HRW production forecasts for competitors provided by USDA in the 2025-26 trade year are lower across the board. Russia, Ukraine, Canada, Australia, Argentina, and the EU have lower production forecasts. The developments of the crops in the Southern Hemisphere seem important, given the forecasts of an extraordinarily strong El Niño arriving later this year and the impact such an event has on those regions. Australia is vulnerable to dryness under El Niño.

Corn Market Outlook: Corn prices continue to struggle to gain momentum despite uncertainty over production prospects and geopolitical issues. The 2026-27 balance sheet forecast for corn held few surprises. A trend yield of 183 bushels per acre will come under criticism, but a more muted version than previous years after the 186.5 bushels per acre registered last year. Forecasting demand for the new crop this far out provides an idea of demand possibilities but the turns and twists possible in the market between now and September are massive.

Corn area in drought equaled 26 percent as of May 12. Drought affected the U.S. corn area, which fell 25 percent from early March as rains in key areas of the Corn Belt came before planting got underway in earnest. The dryest areas for corn acreage are in the plains and the deep South. The corn crop is going in at a timely pace. Planting pace for May 17 sat at 76 percent, which is six percent above the 5-year average and well on pace to hit key planting levels by the end of May. The lack of extreme dryness in the heart of the Corn Belt along with the crop progressing in a timely manner takes speculation on acreage down a bit. At present, there is not a strong supply side issue available for rallying prices. Demand remains on pace to hit USDA’s forecasts.

Exports and ethanol grind maintain support for corn demand. Export sales data for corn through May 7 place total commitments at 3.06 billion bushels, with outstanding sales accounting for 785 million bushels of that total. Corn exports need to average 15 million bushels per week for the remainder of the marketing year to hit the 3.3-billion-bushel forecast. Over the last month, weekly net sales averaged 49 million bushels. Total commitments stand at 93 percent of the forecast. The 5-year average for corn at this point is 95 percent of the total. The final tally depends on corn production in South America, as well as the impacts of the energy price shock on transportation costs and global economic growth.

Corn use for ethanol totals 3.224 billion bushels through March, up 20 million bushels over the previous marketing year. Ethanol production from the beginning of April is up 3.7 percent over the same period last year, which is on par with the pace thus far in the current marketing year. To hit USDA’s forecast implies corn accounting for a higher percentage of the feedstock used in production than in earlier months. Gas demand remains stable despite higher prices, highlighting how inelastic gasoline is for the American consumer. The higher prices may cut into the summer driving season and reduce demand. At present, USDA’s ethanol forecast is slightly high but not egregiously so.

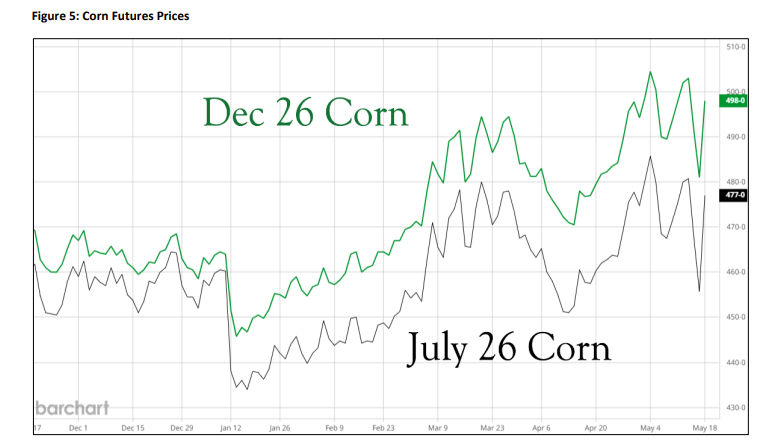

December corn futures moved lower after the USDA reports and struggled to break out of the $4.70-$5.00 range that has held since early March. December prices settled at $4.98 per bushel yesterday. Corn prices reflect the massive carry along with the USDA’s current demand level as a potential maximum with downside potential. The July contract closed at $4.77 on Monday, up from last week. Cash prices across Oklahoma locations range between $4.22 – $4.27 with higher prices reported in some locations.