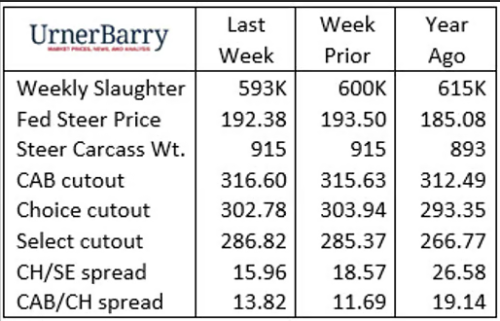

The negotiated cash fed cattle trade last week was technically lower than the week prior by a little more than $1/cwt. For all practical purposes prices have been steadily sideways for the past four weeks, trading in the low to mid-$190s for the period. Weekly packer needs for spot market cattle reflect good demand. This remains especially true in the northern feeding region, where last week‘s prices remained stout at $196/cwt., down from the $198/cwt., live basis, highs recently achieved.

The headline news in cattle presently surrounds the massive sell-off in both Live Cattle and Feeder Cattle futures beginning July 29. In a week’s time the free-fall devalued the August Live Cattle contract by roughly $7/cwt. while the October and December contracts dropped $10/cwt.

As is often the case, beef market fundamentals were no factor in the multi-day routing of cattle contracts. Rather, the headline-grabbing correction in equities fueled the sell-off as hedge funds exited positions and algorithm trading created continuation of the snowball effect. Meanwhile, the August Live Cattle contract is currently priced $10/cwt. lower than last week’s cash fed steer price.

Create emails quickly with structures

The small 593,000 head of federally inspected cattle harvest signals a continuation of the slowed harvest pace. Looking at fed steers and heifers alone, the week’s 483,000 head harvest total was interestingly 2,000 head larger than the same week last year. The prior week ran 3,000 head larger than a year ago.

Boxed beef cutout values were mixed in Urner Barry’s data with Choice reported $1.16/cwt. lower on the week and Select up by $1.55/cwt. The Select cutout is still finding support on increased 90% lean grinding material values.

The CAB cutout gained $0.97/cwt. last week, increasing its premium over USDA Choice to $13.82/cwt. for the week. This is a modest spread compared to a year ago, reflecting relaxed middle meat demand so typical of late July and early August. Carcass tonnage supply for the brand has recently been quite strong compared to the past two years as marbling rates, on average, continue to show a quality-rich fed cattle offering in recent weeks.

Big Departure for Branded Carcasses

During the 1980s, new restaurants and grocery chains stepped up to acknowledge the quality advantage of the Certified Angus Beef® brand, and it was relatively easy to fulfill the added demand. By licensing another packing plant to join the CAB supply chain, the supply reach expanded. Today opportunities for supply growth are more challenging, given that 85% of the U.S. packing volume is licensed under the brand. Thus, supply dynamics come down to one fickle component: the quality of the cattle.

Nearly two decades have passed since the carcass quality low-point was realized with a mere 14% of Angus-influenced cattle meeting the brand’s 10 carcass specifications. Advancements in genetics, feedstuffs, feeding technology and methods have all culminated in the latest highs with over 40% of eligible carcasses meeting brand specifications.

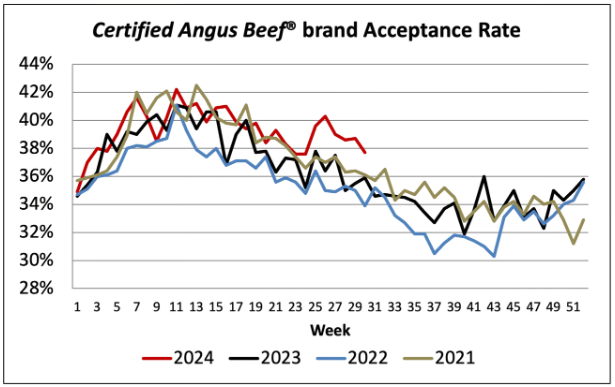

This summer’s timeline shows the brand’s acceptance rate breaking out to the high side, even compared to the already-strong year to date trend. The two-week leap from a 37.6% certification rate to 40.3% began in mid-June, presenting an anomaly data point. But, the trend held higher than expected in the ensuing weeks. This comes in a period when the national fed steer and heifer quality grade trend historically weakens precipitously to the September low.

We’ve documented this year’s USDA Prime grade trend, which has either charted record-highs or near-record highs for several weeks since April. The CAB brand’s Prime and traditional Premium Choice product offerings combined to boost this summer’s certification pace to seasonal record highs.

Heavy carcass weights continue to play a key role in this trend. The country’s USDA Prime grade share is impressive for mid-summer, recently pulling back from a lofty 12% to 10% of fed cattle carcasses. The share of heavy Prime carcasses meeting the brand’s specifications consequently pushed up to 12.3% of the the CAB total in June and July, compared to 11% for the period a year ago. Although average carcass weights are far from last winter’s heaviest weights, the heaviest pens of long-fed steers are presenting an outsized proportion of CAB Prime carcasses compared to recent summers. This seemingly small percentage point change equates to a significant move in CAB Prime carcass supplies.

If carcass weights continue to run more than 15 lb. heavier than a year ago, the tables will turn in the fourth quarter. In December 2023, the heaviest steer weights ever were recorded, reaching a 942 lb. average –partially fueled by a major futures market setback. Still, if unchecked by a trend change this year, steer weights will be massive late in the fourth quarter. Should that develop, a disproportionate share of steer carcasses will not meet the brand’s standards due to one or more factors. Those factors could include excess weight, large ribeye size and too much backfat thickness.