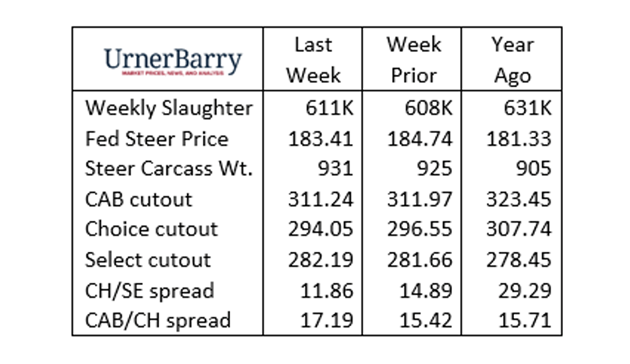

The past two weeks have featured increases in total federally inspected cattle harvest with 608,000 and 611,000 head counts. Last week’s increase was logically a bit larger due to this week’s holiday-shortened production schedule. Packers continue to operate well below capacity, lessening the importance of holiday throughput, relative to the volume of weekly production.

As August drew to a close, the fed cattle market continued to show price weakness from the pressure of three factors: heavy carcass weights, relatively weak cutout values, and the dramatic devaluation of Live Cattle futures. As a consequence, fed cattle traded more than a $1/cwt. lower on a live basis last week with latest prices just a couple of dollars per hundredweight higher than a year ago.

Live Cattle (LC) futures have charted a course toward recovery from the tumultuous August action that saw the current, front-month October contract drop from $186/cwt. on August 1 to the low of $174/cwt. on August 22. The recovery through mid-week positioned the October LC contract $4.99/cwt. higher than the August low at a current $179/cwt.

Carcass cutout values in Urner Barry’s weekly average data were lower last week as spot market demand just ahead of the Labor Day holiday did not spark any uptick. As well, in several recent years, August cutout values have been characterized by large retailers increasing middle meat purchases for long-term “deep chill” storage (winter holiday supply needs.) If spot market price is any indicator, this does not seem to have been the trend in the past month. In most recent data, ribeye and tenderloin prices have been pressured to lower wholesale values, down 14% and 17% respectively, lower than a year ago.

Don’t Fade the Trend

In 2024, wholesale carcass cutout values have signaled an unfulfilled gap for lean beef in the supply chain. The Choice-Select price spread has long been held as the industry’s barometer for the differential in consumer demand for high-quality, well-marbled beef and the leaner counterpart consisting of only slight degrees of marbling. However, using the current Choice carcass premium to Select as a guage for consumer demand is misleading.

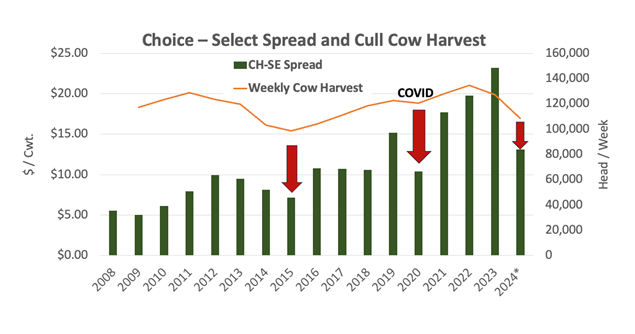

In the first 35 weeks of the year, the Choice-Select spread has averaged $11.68/cwt., a 37% decline from a year ago. A decline of this magnitude suggests consideration of a significant shift in demand. This change is even more notable given that the Choice carcass premium has essentially quadrupled in the past 15 years with a $5/cwt. average in 2009 and a $23/cwt. average in 2023, according to USDA. All of this while the “Choice and higher” quality grades simultaneously grew from 62% of fed cattle product to 82%.

In the same 15-year period, the Choice-Select spread has marked an annual decrease in just three years. Similar to this year’s supply scenario, 2015 was marked by a significant reduction in domestic cull cow harvest as the industry began the rebuilding phase. The other dip in the Choice-Select spread was in 2020, a year forever remembered due to the COVID-19 impacts to the supply chain and wildy erratic price trends.

The supply and price spread data combine to illustrate that this year’s muted Choice-Select spread is an indication of 90% lean trim supply suffering from the decline in cull cow harvest, down 16% year-to-date and 20% for the period in 2022. This has resulted in the 90% lean trim price rocketing to record-highs, currently 20% higher than a year ago. This void in grinding trim has partially been filled with Select end meats from the fed steer and heifer supply. Consequently, the Select carcass cutout price has temporarily been propped up in relation to Choice carcasses. This condition is likely to persist until cull cow volume increases, likely many months in the future.

By contrast, the CAB carcass cutout, relative to Choice, remains robust in 2024 at a year-to-date average of $15.82/cwt., just 3% below last year for the same period. This, with the brand’s certification rate for Angus-type carcasses more than 39% since January 1, on pace for a record year. Although current supply metrics continue to boost the value of Select carcasses, it does not mean that consumers are showing preference toward Select whole muscle cuts. Feed costs and other input resources in the fed cattle sector continue to find the highest return as carcass quality grades and CAB carcass certification percentages increase. We need more cows in the supply chain, not Select grade steers and heifers. Any directional shift away from the long-term trend toward marbling-rich quality grades and brands that deliver on an exceptional eating experience would be misguided.