Dr. Derrell Peel, Oklahoma State University Extension Livestock Marketing Specialist, offers his economic analysis of the beef cattle industry as part of the weekly series known as the “Cow Calf Corner,” published electronically by Dr. Peel and Mark Johnson. Today, Dr. Peel advises on Beef Production and Fall Beef Demand.

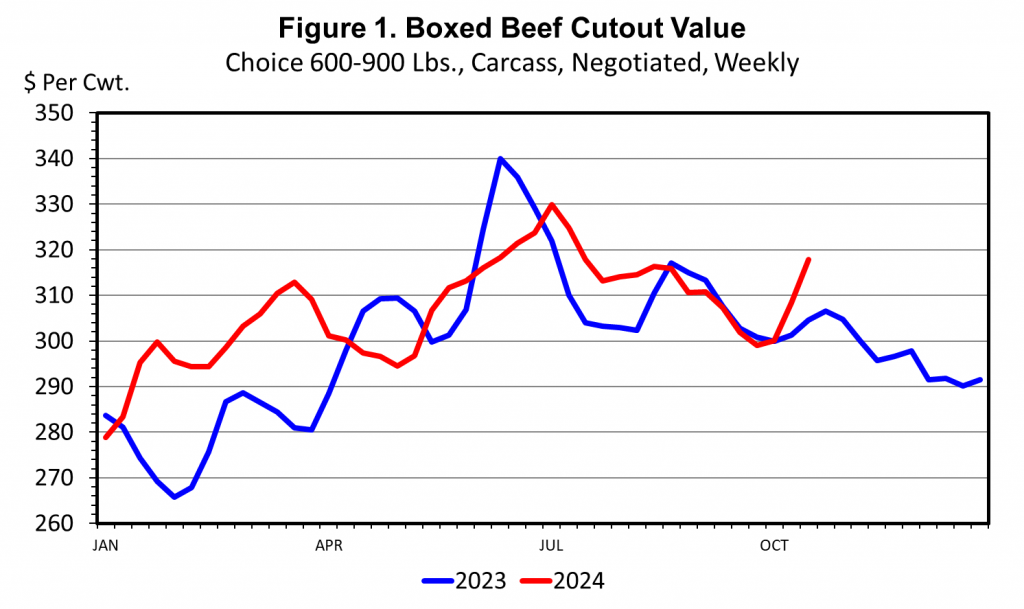

As of October 18, the daily Choice boxed beef price was $320.65/cwt., up from a recent low of $296.37/cwt on September 26 and the highest price since July 15. The weekly Choice boxed beef price is also at the highest level since July and has averaged 2.2 percent higher year over year and a record high for the year-to-date (Figure 1). Numerous wholesale cuts have moved higher recently including chuck arm roast (IMPS 114E), chuck roll (116A), chuck mock tender (116B), and chuck flap (116G). Wholesale round cuts have also moved higher including round knuckle (167A), top inside round (169A), bottom (gooseneck) round (170), outside round (171B), and eye of round (171C). Middle meat prices from the loin and rib have also increased including bottom sirloin flap (185A), sirloin tri-tip (185D), loin strip (180), and tenderloin (189A). Likewise, wholesale ribeye prices (112A) have increased recently and are showing an early seasonal demand for the holidays.

Thus far in 2024, steer slaughter is unchanged from one year ago. Heifer slaughter is down 1.6 percent year over year. Total fed slaughter is down 0.7 percent compared to last year, less than earlier expected. For the year-to-date, steer carcasses have averaged 25.5 pounds heavier than last year, and heifer carcasses are averaging 22.6 pounds heavier than one year ago. The result of stronger than expected fed slaughter and heavier carcass weights has been an increase in fed beef production of 1.9 percent year over year thus far in 2024. In fact, for the last 16 weeks, fed beef production has been 3.7 percent larger year over year. The increase in boxed beef prices is perhaps even more surprising in the face of increased fed beef production. Higher prices and increased quantities suggest that beef demand continues to be very robust.

In contrast to fed beef production, nonfed beef production is sharply lower this year, down 12.8 percent year over year. Total cow slaughter is down 15.3 percent, consisting of a 13.8 percent year over year decrease in dairy cow slaughter and a 16.8 percent decrease in beef cow slaughter so far this year. Bull slaughter is also down 8.1 percent compared to last year. Tighter supplies of lean trimmings have kept processing beef prices higher this year and the demand for lean has increased demand for lean carcass cuts. For example, the current wholesale price of 90 percent lean trimmings is higher than wholesale prices for top inside round, bottom (gooseneck) round, and outside round.

In the fall, summer grilling demand gives way to seasonally stronger demand for roasts, crock pot cooking and increased middle meat demand in restaurants. Wholesale ground beef prices have moderated recently as hamburger grilling demand slows but prices remain well above year ago levels. Total beef production is down a scant 0.7 percent so far this year and may end the year equal to year ago levels. Despite this, wholesale and retail beef prices are higher thus far in 2024.