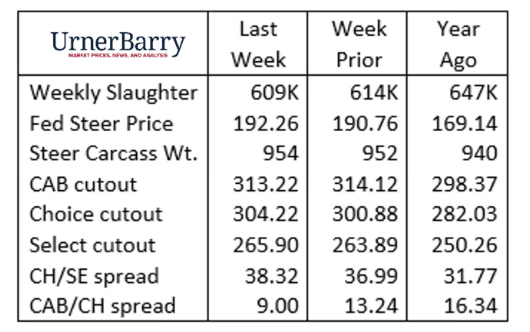

Last week’s federally inspected cattle harvest was 5,000 head smaller than the prior week and 38,000 head smaller than the same week a year ago. A large contribution gap between classes of cattle in the harvested total remains in place. In the past four weeks, fed steer and heifer head counts have increased 0.6% from a year ago, whereas the cull cow harvest was down 14.6%.

With sharply higher Live Cattle futures last Tuesday and Wednesday, cattle feeders were feeling encouraged by mid-week. The Texas cash trade missed out on the rally as packers purchased cattle there early in the week at prices steady with the prior week. The northern trading region capitalized on the upswing later, with packer bids following futures higher. Highs of $198/cwt. were reported for Iowa live sales and $303/cwt. dressed. Nebraska prices were just below the Iowa average generating a $4/cwt. gap between the northern and southern regions for the week’s summary pricing. The disparity pales in comparison to the record-wide north-south price spread observed for many weeks earlier this year.

The boxed beef market continued to price carcasses generally higher last week with Prime, Choice and Select cutout averages higher for the week. The CAB cutout, however, was quoted $1.10/cwt. lower, the only cutout quote with a reporting cutoff on Thursday rather than Friday, like the USDA quality grades. Nonetheless, last minute rib demand has been the predictable highlight, adding $0.50/cwt. for CAB ribeyes above the prior week, pressuring all-time highs seen in 2020. CAB tenderloins finalized their price rally the week prior, ending their seasonal demand surge a full $1.00/cwt., wholesale, cheaper than the same time a year ago.

Optimism surrounding pre-holiday middle meat demand is tempered only by end meat price corrections. While winter roast demand points to cheaper end meats as targeted cuts, that demand won’t set in until later in the first quarter of 2025. For now, several end meats, especially from the round, are correcting toward lower prices within their historically correct seasonal December patterns.

Robust Prime Supplies Prompt Sales

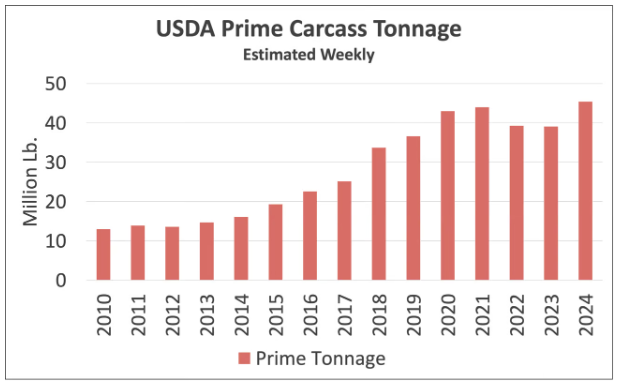

The storied improvement in beef carcass quality improvement will soon close the chapter on the 18th year since the percentage mix of Choice, CAB® and Prime carcasses touched a modern day low. In 2006 the marbling-dependent quality grade distribution pegged USDA Prime at 2.6% of total fed cattle, Choice at 51.6% and Select at 40.9%. The CAB carcass acceptance rate had dipped to a paltry 14% of all brand-eligible carcasses.

Genetic improvement and multiple management factors have since combined to press carcass quality to new heights. Observations during the 2020 pandemic backlog suggested that we’d never again see quality grade as rich as what was induced by supply chain disruptions forcing extended days on feed. Yet in 2024 economics and technology drove feedlot stays to their longest yet due to economic factors rather than supply logistics disruptions. We can only guess at what marbling achievement may have been this year without the benefit of 20-30 added pounds of carcass weight and record-long feedlot stays. Yet it’s logical that quality outcomes would have been slightly lower without those conditions.

Outlook factors for 2025 suggest that tighter feeder cattle supplies and projected continuation of low grain prices will further entrench current cattle feeding patterns. Heavier carcass weights and nominal additions to days-on-feed should remain in place, especially given potential for even higher feeder cattle prices.

These realities will continue to provide ancillary benefits to the quality grade mix and CAB acceptance rate, pressing the latter measure higher than this year’s record 37%. USDA Prime carcasses, averaging 10.5% of fed cattle this year, may push even higher in 2025, potentially adding another half of a percentage point.

Total USDA Prime carcass tonnage was record-large in 2024 despite harvested fed cattle head counts well below historic levels. The combination of the largest Prime percentage and heaviest carcass weights in history joined to accomplish this feat. Given the probability that elevated Prime carcass production remains a factor, increased focus on Prime product sales will be necessary.

Since less than 100 lb. of each Prime carcass is sold at wholesale under a USDA Prime-specific order, there is a concentration of premiums for the Prime grade on middle meat cuts and briskets, generally speaking. Growth in sales and net dollars may have the most opportunity in the Prime category, whether USDA Prime or under the Certified Angus Beef ® brand Prime label. Opportunity to capture a Prime-specific premium across more of the carcass rests on the industry’s sales force to educate end-users about the eating characteristics of additional Prime cuts, as well as broader availability. Absent a return to tighten supplies and rationing of Prime boxed beef, enhanced sales focus is the only path to maintaining premiums for Prime carcasses