The Tweet That Moved the Market

OSU’s Dr. Todd Hubbs write in his weekly Newsletter about the market-moving news last week:

On February 10, 2026, agricultural markets experienced a sudden burst of volatility, sparked not by weather or supply reports but by a social media post from President Trump.

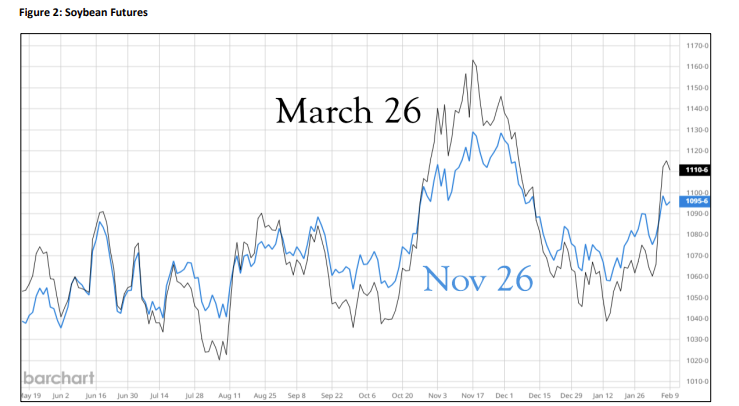

The previous Wednesday, the President posted about a potential agreement with China to purchase an additional 8 million metric tons of soybeans for the current marketing year. While the claim’s veracity remained in doubt, the market took the statement to heart. Soybean futures exploded, rallying over 45 cents on the week for nearby contracts, dragging the rest of the agricultural commodity complex upward with them.

However, the rally’s momentum was fleeting. By Friday, commodities other than soybeans had retreated, leaving the market to face the fundamental realities of supply and demand.

The Soybean Situation: Optimism Meets Reality

Despite the excitement, the March soybean futures closed at $11.15 on Friday, returning to levels seen prior to the USDA report release. The rally was a welcome sight for farmers, particularly because February sets the harvest crop insurance price.

However, the underlying data presents a mixed picture:

- Strong Crush, Weak Oil Demand: The domestic crush pace is strong, totaling 893 million bushels through the first four months of the marketing year—up 13% from the previous year. Yet, soybean oil stocks have swelled by 29% because the expected demand for biofuel usage has not materialized.

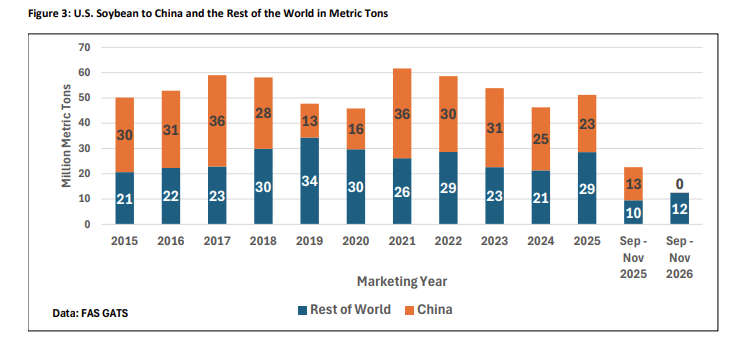

- Global Competition: While the U.S. hopes for Chinese buys, harvest is currently underway in Brazil, where the crop is expected to be record large. As shown in historical data, China can purchase substantial amounts from the U.S. without raising overall U.S. exports if they simply switch other purchases to competitors.

The Wheat Watch: Waiting for Rain in Oklahoma

While soybeans enjoyed a speculative rally, the wheat market remained constrained by well-supplied domestic and global markets.

In Oklahoma, conditions remain “very dry,” posing a threat to wheat potential moving forward. Despite this, broader market concerns regarding winterkill have faded due to warmer temperatures.

- Prices: KC hard red winter wheat prices pulled back, with the March contract closing at $5.29, down two cents.

- The Trend: Prices have been oscillating in a tight range between $5.05 and $5.50 for three months. Breaking out of this range seems unlikely without a major geopolitical event or significant crop deterioration.

A Primer on the New Policy Landscape

Beyond the daily price ticks, the agricultural sector is navigating a complex web of evolving biofuel policies for 2026 and 2027.

1. The Renewable Fuel Standard (RFS)

The EPA is expected to finalize the Renewable Volume Obligations (RVOs) for 2026-2027 within the next two months. The proposal includes high stakes for producers:

- Volume Increases: The EPA proposed significant increases in volume requirements.

- The “Half-RIN” Proposal: A controversial proposal to reduce RINs (credits) generated by imported biofuels by 50% appears to be effectively dead, though it was intended to favor domestic feedstock.

2. Tax Credit Overhaul: The 45Z and “OB3”

The financial incentives for biofuels underwent a major shift on January 1, 2025, when the “45Z” tax credit replaced the traditional blender’s tax credit (BTC).

- Performance-Based: Unlike the old flat credit, 45Z credits are based on carbon intensity scoring.

- The “OB3” Act: Last July, Congress passed the “One Big Beautiful Bill Act” (OB3). This legislation extended the 45Z credit through 2029 but introduced a crucial limitation: starting in 2026, eligibility is limited to fuels produced and feedstock sourced strictly from the U.S., Canada, and Mexico.