The agricultural financial sector is currently navigating a period of normalization, following several years of record-high cash flows and historic liquidity. Jackson Takach, Chief Economist at Farmer Mac, provided a deep dive into the credit quality and lending trends shaping the industry during his presentation at the 2026 USDA Agricultural Outlook Forum and Why Farmland Values Remain Resilient.

The Resilience of Farmland Values

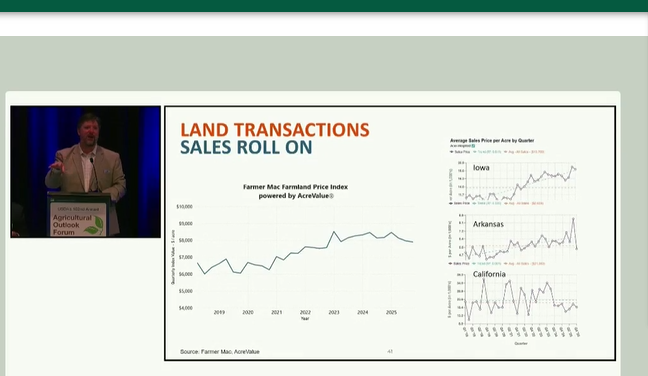

Despite rising interest rates and a tightening farm economy, farmland values have remained remarkably stable. Takach points to a significant lack of supply as the primary driver.

“One of the big drivers in the last two years has been—well, no one’s had any pressure or need to sell,” Takach explained. “They have very low interest rates on their farms, or no debt at all. What’s the impetus to sell?”

This supply constraint means that when a piece of land does hit the market, it is often snatched up by neighbors or well-capitalized producers. Takach noted that current “marquee numbers” seen in headlines—ranging from $30,000 to $50,000 per acre—are typically driven by local buyers with long-term interests rather than outside investors.

The Credit Quality “Floor”

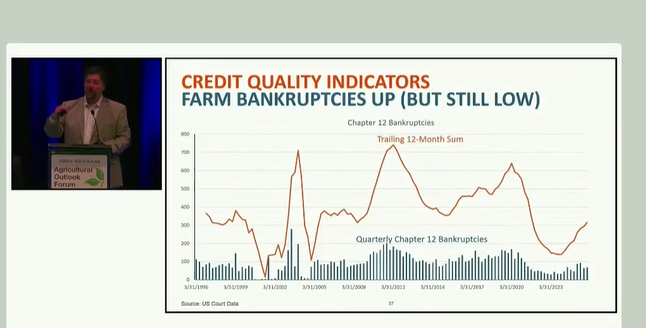

Agricultural credit quality is currently coming off historic highs. During 2024 and 2025, delinquency rates reached near-zero levels as producers benefited from high commodity prices and robust government support programs.

“If no one is defaulting, if people don’t feel stress or pressure to change their balance sheet or to liquidate assets, how much land do you think is going to come up for sale?” Takach asked. “Very, very little.”

While bankruptcies (specifically Chapter 12 filings) are beginning to tick upward from their recent lows, they remain below long-term averages. However, Takach highlighted a regional concentration of stress, particularly in the Delta region due to challenges in the soybean, cotton, and rice markets.

Lending Trends and Underwriting

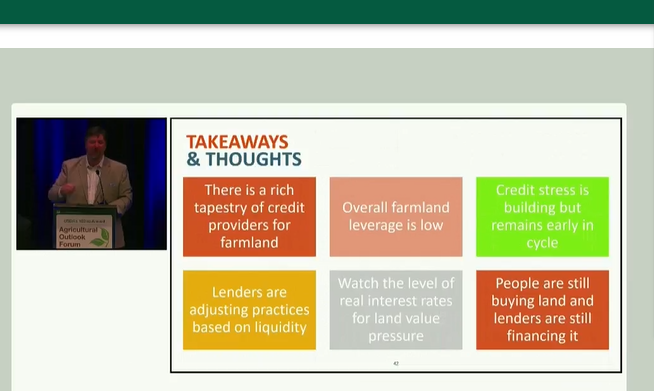

The lending landscape remains a “rich tapestry” of providers, including the Farm Credit System, commercial banks, and insurance companies. While the Farm Credit System was particularly active during the low-interest-rate environment of 2020–2023, commercial banks have recently regained momentum.

Current trends in lending include:

- Consistently Low Leverage: Overall farm mortgage debt results in a loan-to-value ratio of approximately 11%, significantly lower than residential or commercial real estate (both around 30%).

- Locked-in Rates: Many producers successfully “termed out” their debt between 2020 and 2023, securing 30-year mortgages at rates as low as 3%.

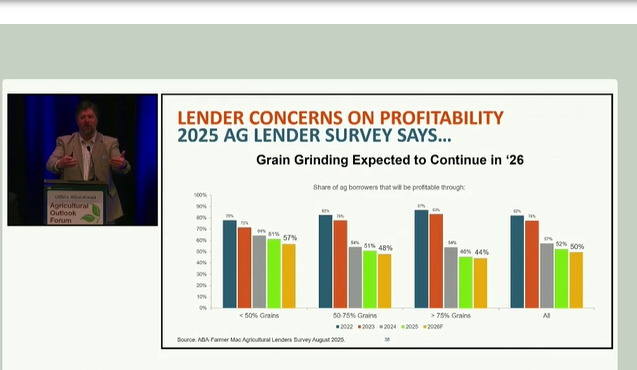

- Tightening Standards: As profitability expectations for 2026 decline, lenders are increasing scrutiny at both the cash flow and collateral levels.

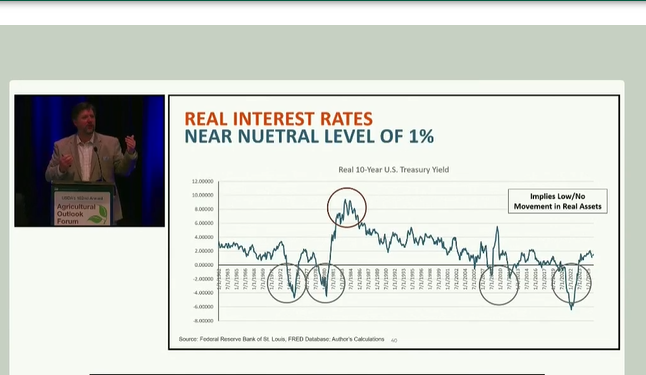

The “Real” Metric to Watch

For those trying to predict the future of land values, Takach recommends looking past the Federal Funds Rate and focusing on the Real Interest Rate (the 10-year Treasury minus inflation).

“This is my favorite metric,” Takach said. “It has predicted every time I think farmland’s going to go up or I think farmland’s going to go down.”

Currently, the real interest rate is in a “neutral” zone, roughly 1% to 1.5% above inflation. This suggests a plateauing of land values rather than a sharp decline, as the cost of capital is now catching up with cash flow increases.

Regional Variations: A Tale of Three Markets

While the national average provides a broad overview, Jackson Takach emphasized that agricultural land remains a local market driven by specific regional pressures. Examining Iowa, Arkansas, and California reveals how different commodities and economic stressors influence land values.

Iowa: The Gold Standard of Resilience

In Iowa, the trend remains “up and to the right,” despite the broader economic cooling. Takach identified Iowa as a prime example of a market where local demand overrides national interest rate trends.

“In Iowa, land sales are happening and the values are going up,” Takach noted. “A lot of those land sales are to very wealthy farmers in the area who love the land. Again, it’s that supply issue—they don’t see the land come up very often, so when they do, they buy it”.

Arkansas: Navigating Commodity Stress

The Arkansas market presents a more volatile picture, largely due to its concentration in the Delta region. This area is currently the primary focus for agricultural financial stress in the U.S..

Takach pointed out that the concentration of Chapter 12 bankruptcies and liquidations is currently localized along the Delta, affecting states like Arkansas. Producers here have had to work through a “very challenging set of commodities” over the last year, including soybeans, cotton, and rice, leading to more volatility in land transactions compared to the Midwest.

California: Volatility in Permanent Crops

California’s land market has experienced significant dislocation, particularly within the permanent crop sector. Takach used the almond industry as a prime example of how rapid shifts in supply and demand can impact regional land values.

“We said, ‘Oh, we want as many almonds as we can have,’ and then we said, ‘Actually, we don’t want that many almonds,'” Takach explained. This reversal has led to a much more volatile market in California than the national average would suggest, highlighting the importance of understanding local supply and demand elements for every specific state and county.