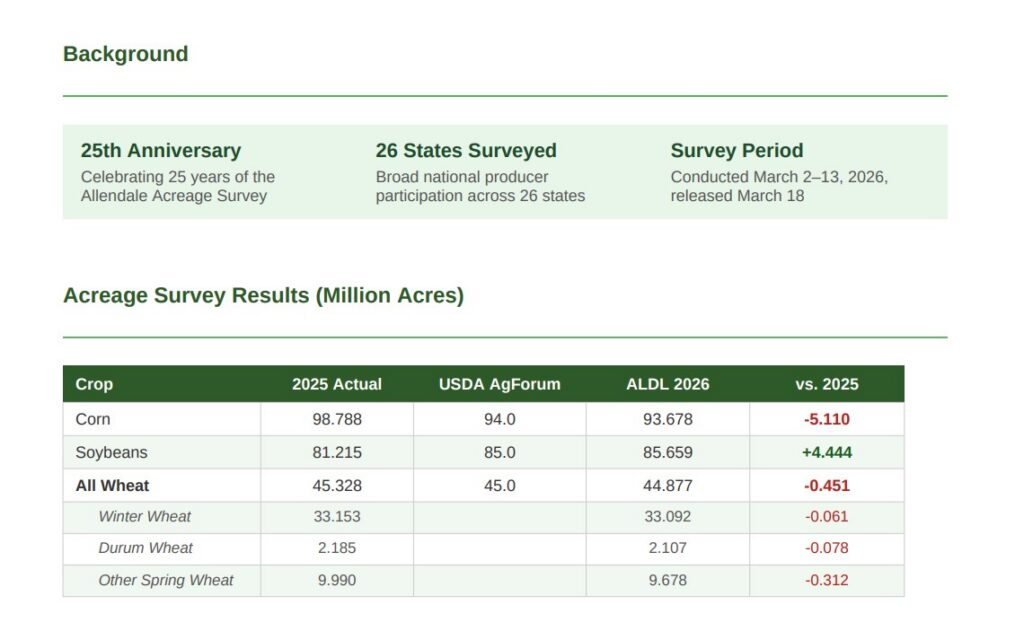

Allendale, Inc. has released the results of its 25th annual nationwide acreage survey, providing a critical look at producer planting intentions for the 2026 season. Conducted from March 2 to March 13, the survey captured data from producers across 26 states, revealing a significant shift in acreage away from corn and toward soybeans compared to the previous year.

Acreage Shift and Planting Intentions

The most notable takeaway from the survey is the projected decline in corn acreage. Allendale’s 2026 survey estimates corn planting at 93.678 million acres, a substantial decrease of 5.110 million acres from the 2025 actual of 98.788 million. This figure also sits slightly below the USDA AgForum estimate of 94.0 million acres.

In contrast, soybean acreage is seeing a marked increase. Producers intend to plant 85.659 million acres of soybeans, up 4.444 million acres from 2025. This projection exceeds the USDA AgForum estimate of 85.0 million acres.

Wheat acreage is expected to remain relatively stable but trending lower, with total wheat planting estimated at 44.877 million acres. This represents a decrease of 0.451 million acres from the previous year. Within the wheat complex:

- Winter Wheat: 33.092 million acres

- Other Spring Wheat: 9.678 million acres

- Durum Wheat: 2.107 million acres

Production Potential

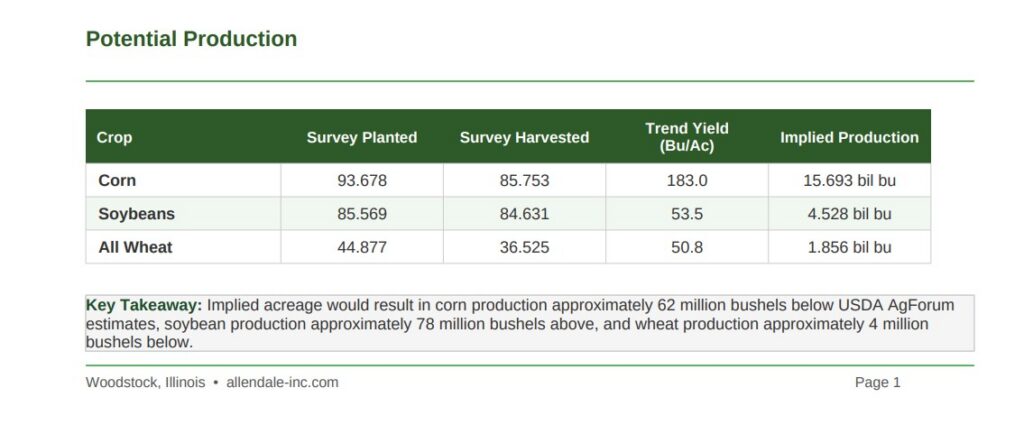

Based on these acreage intentions and Allendale’s trend yield projections, implied production for the 2026 season is as follows:

| Crop | Survey Harvested (Million Ac) | Trend Yield (Bu/Ac) | Implied Production |

| Corn | 85.753 | 183.0 | 15.693 billion bu |

| Soybeans | 84.631 | 53.5 | 4.528 billion bu |

| All Wheat | 36.525 | 50.8 | 1.856 billion bu |

According to Allendale, these acreage levels would result in corn production approximately 62 million bushels below USDA AgForum estimates, while soybean production would likely land 78 million bushels above.

Producer Sales and Market Sentiment

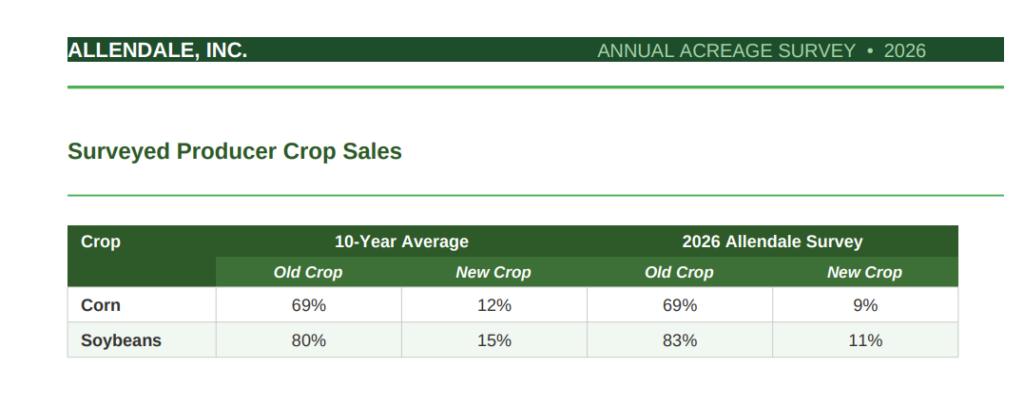

The survey also tracked the progress of producer crop sales, comparing current activity to 10-year averages. For corn, producers are currently 69% sold on old crop, matching the long-term average, while new crop sales are lagging slightly at 9% (compared to the 12% average).

For soybeans, producers have been more aggressive with old crop sales, reaching 83% sold versus the 80% average. However, new crop soybean sales are also behind the pace at 11%, compared to the 15% 10-year average.