The release of the April World Agricultural Supply and Demand Estimates (WASDE) has provided the market with a clearer picture of the 2025/26 marketing year, signaling a shift toward more comfortable supply levels. Farm Director KC Sheperd sat down with Rich Nelson, Chief Strategist at Allendale, to provide an April WASDE analysis that goes beyond the balance sheets. While the report pointed to growing supplies for several major commodities, Nelson suggests that the market is now entering a phase where domestic demand and South American production revisions will dictate the next move for prices

Corn and Soybeans: Watching the Balance Sheet

A primary driver for the upcoming report remains the production numbers coming out of Brazil and Argentina. For months, the USDA has maintained a more conservative outlook on crop reductions compared to local agencies like CONAB. Nelson indicates that the gap between these estimates may finally begin to close.

“The market is really looking for the USDA to catch up with some of the private and local estimates we’ve seen out of South America,” Nelson noted. “We’ve seen significant stress on the Brazilian second-crop corn. If the USDA trims these production numbers, it could tighten the global balance sheet more than some expect.”

Regarding soybeans, the focus remains on domestic crush and the impact of renewable diesel. “The crush numbers have been strong, and while the USDA has been slow to move, the underlying demand is there,” Nelson added. “We are seeing a market that is trying to find its footing after a heavy harvest, and any downward revision in global stocks will be viewed as a win for the bulls.”

Wheat: Stability Amid Global Competition

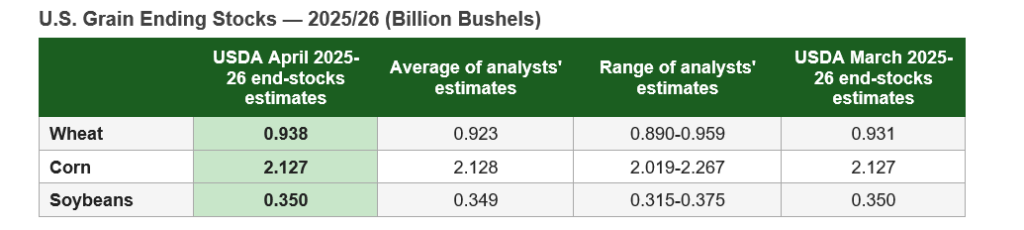

The wheat market enters the April report with relatively stable domestic expectations, though global competition remains a concern. Nelson pointed out that while U.S. ending stocks have remained steady around 915 to 926 million bushels, the real story is international.

“Wheat supplies have loosened slightly on the global stage, but we are watching the export pace from Russia and Ukraine closely,” Nelson explained. “For the U.S. producer, the question is whether we can maintain our current price floor. We haven’t seen major changes in domestic food use, so the market is really waiting for a supply-side shock that hasn’t materialized yet.”

Cotton: Searching for a Bottom

The cotton market has been characterized by a “long-term downtrend,” and the April report is expected to show whether that trend has any hope of leveling off. Nelson observes that the market is currently searching for a firm bottom amid rising ending stocks and lowered export views.

“Cotton producers are facing a tough environment right now,” Nelson said. “We’ve seen ending stocks drift higher—now sitting around 4.4 to 4.5 million bales—which is significantly larger than what we saw over the last two years. Until we see a shift in the export viewpoint or a significant change in global consumption, the market remains under pressure.”

Livestock: Beef Imports and Production Shifts

On the livestock front, the conversation centered on the USDA’s recent adjustments to beef production and the dramatic spike in imports. The agency previously added nearly 200 million pounds to its 2026 production estimate, but the import side of the ledger tells a more complex story.

“The USDA made a massive jump in their view on beef imports—up 100 million pounds in just one month,” Nelson explained. “This adjustment suggests that U.S. consumers will see similar beef availability in 2026 as they did in 2025. Effectively, this removes the immediate expectation of a supply drop, which may take some of the ‘heat’ out of the market. We are likely looking at these higher prices sticking around for the next three to four years rather than a quick spike and drop.”

Market Sentiment and Positioning

Entering the report, managed money remains heavily short in the grain markets. Nelson believes this positioning makes the market sensitive to any “bullish surprises” that might emerge from the data, especially if South American numbers are revised downward.

“The funds are carrying a significant short position,” Nelson said. “In a neutral-to-bullish scenario, where we see even modest cuts to global ending stocks, we could see a quick round of short-covering. This isn’t necessarily the report that starts a new bull market, but it could certainly prevent further significant slides as we move into the North American planting season.”

You can find Rich Nelson at Allendale.

You can see the full WASDE Report here: