On Tuesday May 12, USDA released the Crop Production and WASDE reports. The May Crop Production report provides the initial projection of the winter wheat crop and the WASDE puts forth the first balance sheets for the 2026-27 crop marketing years. The reports capped another volatile week in which the futures markets moved dramatically due to news on the Iran war and the release of the USDA forecasts.

The reports came in particularly bullish for wheat markets on lower-than-expected production. This newsletter reviews the major takeaways and implications from those reports.

Wheat Market Outlook

The USDA reports reflected the production issues in wheat seen around the world and provided greater support to the wheat market. Prices moved higher across all major wheat futures contracts after the release of the data. Wheat prices continue to work through the information from geopolitical events. In combination with expectations of lower production, HRW prices should remain strong with the potential for extreme volatility due to developing crop potential around the globe and issues surrounding the Iran conflict.

On the domestic balance sheet, the WASDE report lowered domestic use of wheat by dropping food usage seven million bushels to 960 on the 2025-26 balance sheet. Most of the lost food usage, six million bushels, was in hard red winter. Exports offset the food drop with a 10 million bushel increase to 910 million. The export increase came from increasing soft red winter and hard red spring exports by 5 million bushels each. Ending stocks came in at 935 million bushels, three down from last month. The overall impact from old crop balance sheet changes is neutral for prices. New crop developments tell an entirely different story.

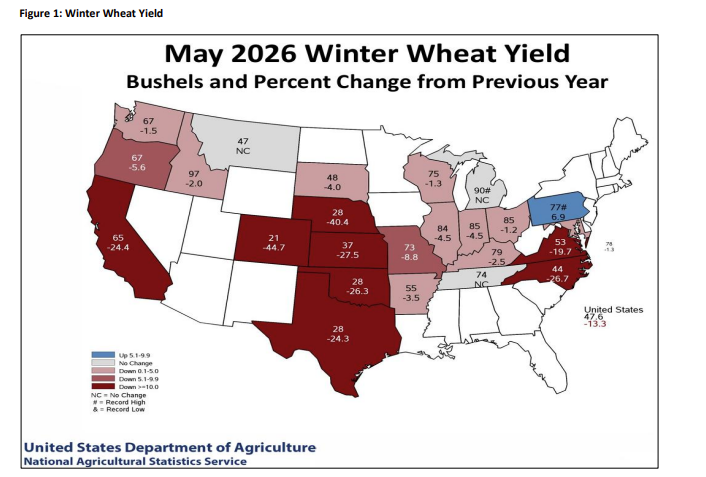

The USDA winter wheat production report for May came in below analysts’ estimates. At 1.047 billion bushels, the estimated winter wheat crop dropped 25.3 percent from last year. Harvested acreage and yields fell across the country. Harvested acreage totaled 22.015 million acres, down 13.7 percent from last year. The harvested to planted acreage ratio equaled 67.9 percent, slightly above the 66.9 seen in 2023. Oklahoma harvested acreage came in at 2.3 million, down 17.9 percent from last year. Harvest acreage across the plains came in low and supported the poor conditions reported across the region.

Winter wheat yield is estimated at 47.6 bushel per acre. Like harvested acreage, yield across the region is down sharply. Oklahoma’s estimated yield of 28 bushel per acre in on par with yields seen in 2022 and 2023 in the state. Total production for hard red winter wheat sits at 515 million bushels, down 36 percent from last year. Soft red winter production totaled 301 million bushels, down 14.7 percent. Even white winter wheat came in 5 percent down from last year at 232 million bushels.

Lower production for winter wheat is reflected in the new crop balance sheet for wheat. By class forecasts are not released until July so the wheat balance sheet reflects all the classes. Wheat production is forecast at 1.56 billion bushels with supply equaling 2.64 billion, down 328 million bushels from last marketing year. Lower supply is reflected in feed and residual falling to 80 million bushels and exports being lowered to 775 million bushels from the old crop total of 910. Ending stocks for the marketing year equate to 762 million bushels under these projections. While usage is down, the domestic production scenario remains bullish for prices.

2026-27 world wheat production came in at 30.95 billion bushels, down 910 million bushels from the 2025-26 crop. Smaller projected crops in Argentina, Australia, Canada, the EU, Kazakhstan, Ukraine, and Russia combined with the U.S. forecast to lower wheat production around the globe. A significant amount of discussion over the last month about crop issues related to fertilizer, acreage, and weather materialized in this report. Australia and Argentinian wheat production came in 254 and 220 million bushels lower than last crop year. The Russia crop totaled 3.2 billion bushels, down an additional 158 million bushels. EU production was lowered 335 million bushels from last year to total 4.997 billion bushels. Production in major importers is projected up 517 million bushels year over year to 8.07 billion bushels.

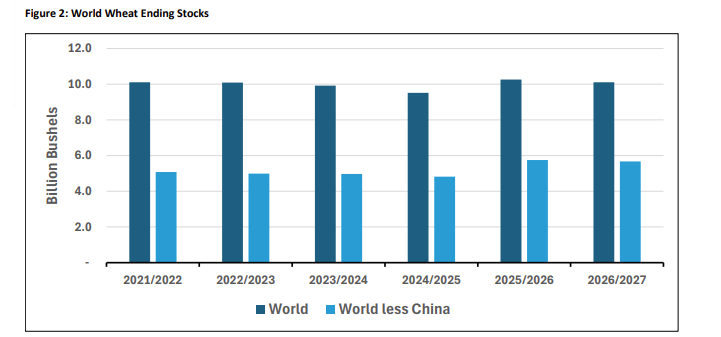

Ending stocks outside of China are forecast at 5.67 billion bushels, a decrease of 80 million bushels from the prior year. In compensation for lower production, global trade in wheat is expected to fall with trade year exports for 2026-27 totaling 7.8 billion bushels, down 440 million bushels year over year.

The result of the stark production forecasts is KC hard red winter wheat prices exploded higher on Tuesday to close at $7.31 in the July futures contract. The limit up gain in futures pushed HRW prices well above recent ranges and reflects the bullish scenario over the near term. In Oklahoma, cash prices for delivery and July delivery converged with prices seen in the $6.81 – $6.91 range.

Soybean Market Outlook

Soybean futures prices moved higher across the forward curve yesterday on the USDA data release. The July soybean contract popped thirteen cents higher to sit at $12.27 and the November contract closed at $12.05, up ten cents. The rally came despite a forecast of larger global production in 2026-27 and global ending stocks coming in slightly lower than 2025-26. Cash prices in Oklahoma sat at $11.31 – $11.37 for delivery. Harvest prices came in at $11.15.

Old crop soybean balance sheet saw crush raised 20 million bushels to 2.63 billion on strong pace thus far in the 2025-26 marketing year. Ending stocks were lowered to 340 million bushels as exports dropped 10 million to 1.53 billion bushels. The probability of these adjustments continuing as the marketing year progresses appears high at this point.

The initial forecast for the 2026-27 marketing year placed soybean yield at 53 bushels per acre which is no change from last year. Supply increased year over year on higher harvested acreage of 83.7 million and a minor increase of beginning stocks. Supply of 4.8 billion bushels was a 188-million-bushel increase. New crop soybean crush is forecast at 2.75 billion bushels, up 120 million over the current year estimate. Driven by supportive biofuels policy and strong demand for soybean meal both domestically and overseas, this crush forecast is ambitious but doable. USDA projected soybean exports at 1.63 billion bushels, up 100 million bushels from last year. The increase came despite U.S. prices sitting well above competitors and projecting Brazilian production up 220 million bushels at 6.8 billion bushels. One must assume Chinese purchases helping this forecast with the expectation of intense competition out of South America. Ending stocks were down 30 million to 310 million bushels.

Soybean oil production came in higher on stronger crush with soybean oil use for biofuels forecast to hit 17.8 billion pounds in 2026-27. Decreased exports and food usage offset the drop in biofuels usage. Soybean meal production is up with a projected increase in exports and domestic usage. Lower prices for meal are expected to drive a strong demand in 2026-27.

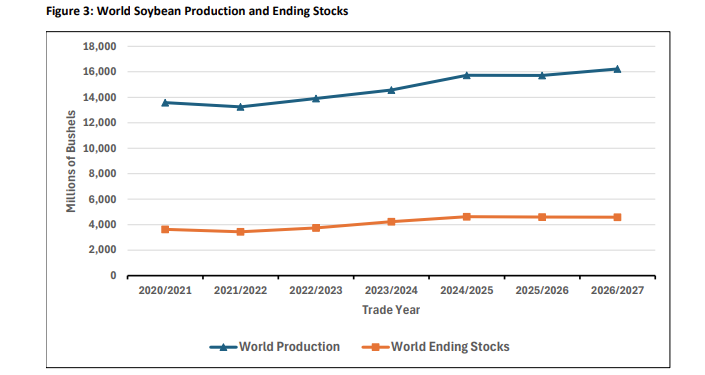

Global soybean production for 2026-27 was forecast 512 million bushels higher at 16.2 billion bushels. Major exporters in South America are expected to increase production by 276 million bushels to 9.2 billion bushels but exports out of the region are forecast to fall slightly. Time will tell if domestic usage, particularly for biodiesel, in South America materializes to support this curious development. Global ending stocks are projected to fall slightly.

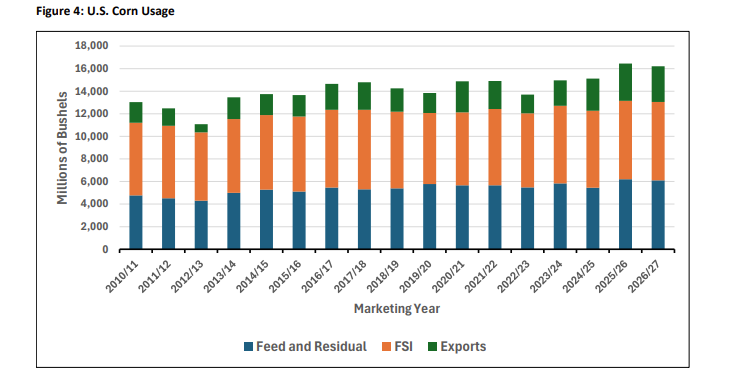

Corn/Milo Outlook

Corn markets saw a more muted price change after the reports. July corn futures increased four cents after the report to $4.80 per bushel. December corn futures followed suit to close at $5.02. Corn in Oklahoma was priced on average around $4.25 per bushel with harvest prices in the $4.62 – $4.67 range. It appears likely that corn markets hold a slightly positive tone for the near future.

The corn balance sheet saw one change to the old crop balance sheet as FSI was lowered 15 million bushels which led to ending stocks being raised to 2.142 billion bushels. New crop corn supply came in lower than last year with the initial forecast which should come as no surprise to anyone. USDA’s corn yield forecast of 183 million bushels follows a trend yield model that has come under question by analysts. It is not farfetched. Harvested acres of 87.4 million is based off the planted acreage of 95.3 put forth in the March reports. Supply came in at 18.6 billion bushels on 16 billion bushels of production. A significant amount of speculation and consternation will revolve around these acreage and yield numbers for the next few months.

Corn usage is forecast to hit 16.2 billion bushels for 2026-27 marketing year with exports and feed/residual usage projected slightly lower than last year. While exports are forecast lower, the U.S. share of the world corn trade is projected to have a modest drop to 38.6 percent and remain well above the normal average of around 30 percent typically seen over the last decade under normal conditions.

Corn global production is forecast at 51 billion bushels, down 681 million from last marketing year. The largest reductions in production are for the United States, Argentina, South Africa, Mexico, and Ukraine. Larger crops projected for China, Brazil, Serbia, Kenya, and Russia offset some of the production loss. World corn consumption is forecast up less than 1 percent to a record 51.8 billion bushels. Ending stocks decreased to 10.93 billion bushels, down from 11.69 billion in 2025-26 and would be the lowest since 2013-14 if they happen.

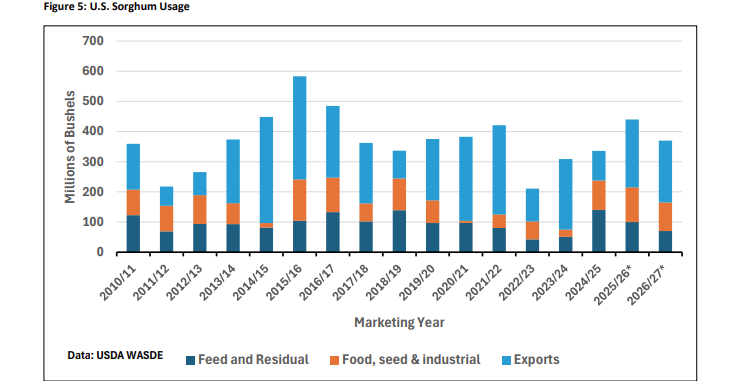

Milo production was forecast at 367 million bushels, down 70 million from 2025-26. Harvested acreage at 5.3 million acres, down 700,000, combined with a trend yield of 69.2 bushels per acre composes the 2026-27 production total. Milo supply of 404 million bushels is down 73 million.

USDA forecast ending stocks at 34 million bushels, down three million from last year. The smaller supply sees usage revert lower. Food, seed, and industrial use is projected at 95 million bushels, down 20 million year-over-year and indicating an expectation of lower milo totals in the ethanol grind. Feed and residual fell to 70 million on the smaller crop. Exports are forecast at 205 million bushels which indicates on expectation of China buying once again. Cash milo prices in Oklahoma were reported in the $3.70 range with harvest prices at $4.02 – $4.07.