The current agricultural trade landscape is heavily defined by drifting grain markets as prices slide into familiar territory due to a distinct lack of fresh fundamental news. The combination of early harvest progress, fluctuating international trade policies, and looming weather patterns has left traders searching for clear direction.

Farm Director KC Sheperd recently sat down with Oklahoma State University Crop Marketing Specialist Todd Hubbs to break down the technical factors driving the current market conditions and what producers should look for in the months ahead.

Wheat Markets Driven by Technical Moves and International Spillovers

The winter wheat harvest is officially underway in areas fortunate enough to avoid recent rain delays, but the overall condition of the winter wheat crop remains poor. Despite the lackluster crop conditions, July hard red winter wheat futures have retreated, erasing the gains prompted by the bullish May crop production report. Hubbs attributed this downward trend primarily to technical trading rather than shifts in supply and demand.

“There’s not a lot of fundamental information coming into the markets,” Hubbs stated. “The wheat crop conditions are still poor for winter wheat… This week we’ve seen the prices for July futures, hard red winter, retreat back to levels before we got that really bullish May crop production report. It’s a lot of technical moves, KC.”

Hubbs noted that external factors, including energy markets, are also dragging grain prices down.

“A little bit of spillover from oil as we see the Strait of Hormuz thing look like it may come to some kind of resolution… It’s a little bit technical, the weakness is a little bit of a spillover and we’re just sort of mozying lower to the lower part of the range we’ve been in since early March for wheat,” Hubbs said.

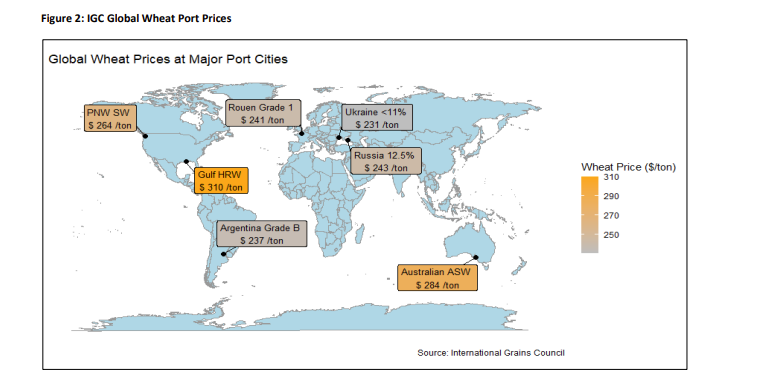

On the international stage, the market remains focused on production in the Northern Hemisphere, specifically within the European Union and the Black Sea region. While the EU is experiencing localized dryness in eastern nations like Poland and the Baltic States, the overall global supply looks stable, cushioned by previous record-breaking years. Russia’s crop is currently projected to come in around 90 million metric tons.

Global Trade Disruptions and the El Niño Factor

International trade dynamics are shifting, particularly with speculative reports that Turkey may institute a wheat import ban following a strong domestic harvest. Because the United States produces a smaller hard red winter wheat crop and maintains slightly elevated prices on the world market, direct export volumes may not shift dramatically, but the broader global trade ecosystem will feel the impact.

“Turkey’s talking about putting—there’s speculation they might put an import ban on wheat because they’ve had a good crop,” Hubbs explained. “That sort of throws off all those trade flows out of Europe and the Black Sea area. Maybe puts a little bit more wheat on the world market.”

Looking further down the road, the arrival of the El Niño weather phenomenon this summer introduces long-term uncertainty, particularly for Southern Hemisphere producers.

“We’ve still got this El Niño phenomenon coming down the pike this summer… That has really strong implications for the Southern Hemisphere, but that’s months away, KC,” Hubbs noted.

While Australia’s acreage is down and dry conditions plague Western Australia, Hubbs believes a smaller Australian crop will eventually provide a late-year boost to the world market as global stocks tighten. However, for domestic hard red winter wheat prices to break out of their current pattern, the market will require a new macroeconomic trigger or geopolitical shock.

Soybeans Supported by Record-Breaking Domestic Crush

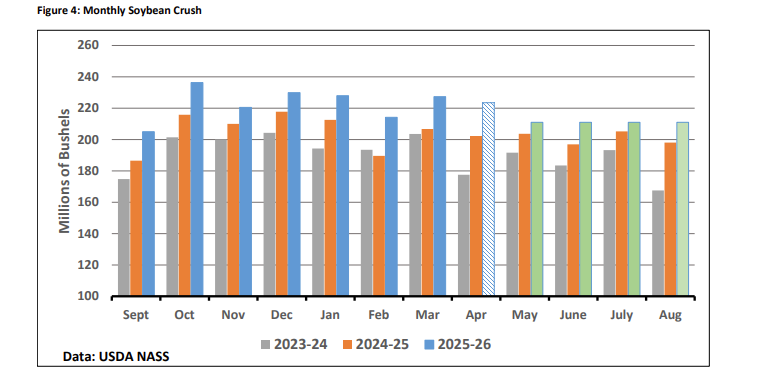

In contrast to the drifting wheat market, the soybean sector is experiencing robust domestic demand. Even as planting progresses smoothly—reaching 67% across tracked states—and prospective acreage remains high, booming domestic processing is keeping the market grounded.

“We’re just absolutely setting record crush numbers every month,” Hubbs said. “USDA raised their crush in the last WASDE, lowered exports a little bit. I expect that to continue as we continue to see record monthly crush numbers to feed the biofuel RVOs (Renewable Volume Obligations).”

This domestic processing boom has generated a massive supply of soybean meal, which has found a eager market both at home and abroad.

“We’ve had really strong demand for soybean meal, both domestically and internationally,” Hubbs emphasized. “There was a lot of concern that we wouldn’t be able to move that much soybean meal as we expanded crush. I was always optimistic we would, and so far we have been.”

While an extended energy crisis or logistical blockages in trade routes could eventually slow economic growth and impact meat demand in East Asia, Hubbs remains confident that the modernized livestock sectors in these importing nations will continue to favor high-quality U.S. soybean meal.

The China Wildcard: A “See It to Believe It” Outlook

When asked about potential trade breakthroughs regarding agricultural purchases from China, Hubbs expressed a highly cautious perspective, noting a lack of official confirmation from Chinese authorities regarding statements made by the U.S. administration.

“I haven’t heard anything out of the Chinese really to confirm what the President and the administration said,” Hubbs remarked regarding rumors of a $17 billion purchase outside of normal soybean commitments. “It sounds like there’s something there… They always buy our milo, I can’t see that stopping. Maybe they get a little bit of corn, maybe they take some wheat, I don’t know.”

Ultimately, Hubbs advises producers to maintain a realistic view of international trade announcements until concrete orders materialize.

“I’m a big ‘see it to believe it’ person when it comes to China… I’m glad the markets took some, but I think that’s all disappeared to be honest with you, KC,” Hubbs concluded.