In his weekly newsletter, OSU’s Todd Hubbs writes: Crop markets struggle to gain bullish sentiment as weather and geopolitical developments combine to keep prices under pressure. Rain events across the Corn Belt and Southern Plains place spring crops on a firm footing. While the Iran conflict still appears in flux, the prospect of a resurgence in hostilities looks remote as the administration attempts to extract the U.S. from the situation. A mandatory joint review of the USMCA after six years is due to kick off on July 1. The prospect of the administration injecting trade and geopolitical uncertainty into crop markets seems high given recent rhetoric. USDA releases the Acreage and Stocks reports on June 30 as well. Next Tuesday’s reports will set the tone for prices leading into summer.

Wheat Market Outlook: Hard red winter wheat harvest reports confirm the poor crop conditions and forecast for the 2026 crop from USDA. Despite the smallest HRW crop since 1957, HRW prices strain to gain purchase. Prices in the HRW markets moved higher relative to the domestic market and international prices recently on the poor crop. However, HRW price will find it difficult to disconnect from competitor prices and take another leg up. The release of the stocks and acreage reports next week should not hold any major surprises for the HRW market.

Usage in the 2025-26 marketing year looks on pace to be around USDA’s ending stocks number of 935 million bushels. New crop export sales for HRW sit at total commitments of 45 million bushels through June 11, down from 90 million bushels at the same point last year. The lower export pace comes as no surprise given the crop size and price competitiveness at ports. The potential for lower harvested acreage in HRW states is acute. The magnitude of acreage changes points toward minor adjustments. It will take a major acreage change to drive prices higher. Given the underlying global fundamentals, a price rally due the reports or on deteriorating weather in the EU should be regarded as sale opportunities.

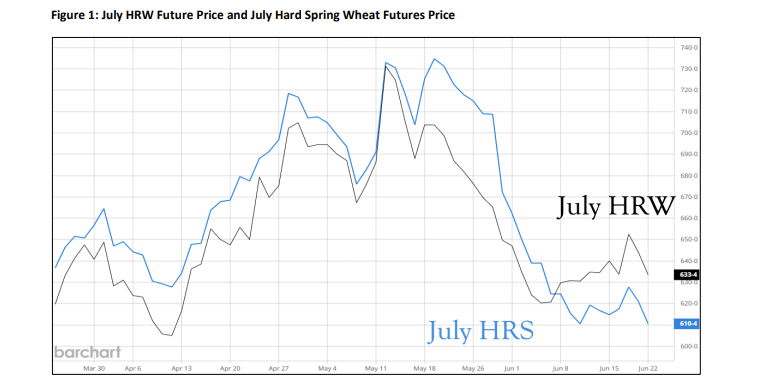

July HRW futures moved above July hard red spring wheat futures last week which is a rare occurrence. July HRW prices closed yesterday at $6.33 per bushel, in the middle of the $6.15 – $6.50 range seen recently. A breakout for futures increasingly relies on weather in the EU and export prices becoming more competitive on the global market. HRW cash prices around Oklahoma vary in the $5.88- $5.93 range after Monday’s close. Basis remains stable.

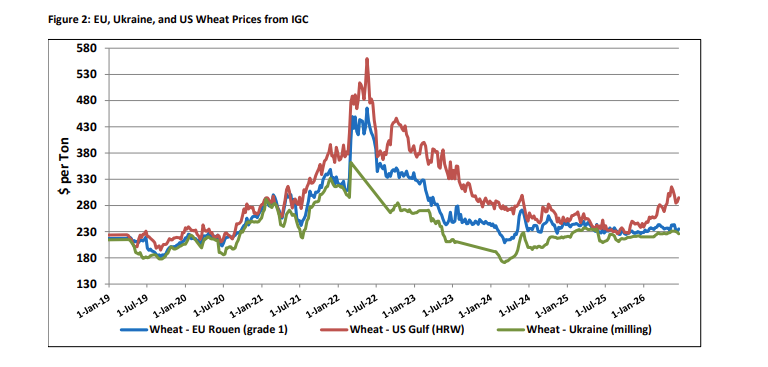

HRW Gulf prices sit above Northern Hemisphere competitors. The potential for EU prices to move higher has been the subject of significant amounts of speculation in the trade recently as a heat wave is expected to impact the end of the growing season across Europe. The projected magnitude of the heat wave is quite severe and holds the potential of impacting the wheat crop in Germany and Poland in particular.

Market observers have already begun to move EU wheat production levels below USDA’s forecast of 136 MMT. It may be premature to move production forecast significantly lower at this point. The uncertainty around the impact muted the addition of a large weather risk premium into the EU wheat market. If the market has not built a weather premium in for the event, an expectation of movement should be in place. It is important to remember that current forecasts for Germany (808 million bushels) and Poland (480 million bushels) are already lower than last year, and U.S. port prices sit above EU and Black Sea locations at present.

Corn Market Outlook: Corn prices indicate plentiful supplies and a positive outlook for the 2026 crop in the U.S. The forward curve carry from July to December sits around 80 – 95 percent of full carry depending on how one calculates storage and interest costs. This is a heavy carry set up indicating ample supply. It also gives an indication of why prices are having difficulty rallying. Weather in the Corn Belt has been particularly supportive of new crop potential. Corn area in drought through June 16 fell to 23 percent, down four percent over the last two weeks. Over the last week, rain has moved into previous dry areas and an expectation of the drought levels falling further is in place.

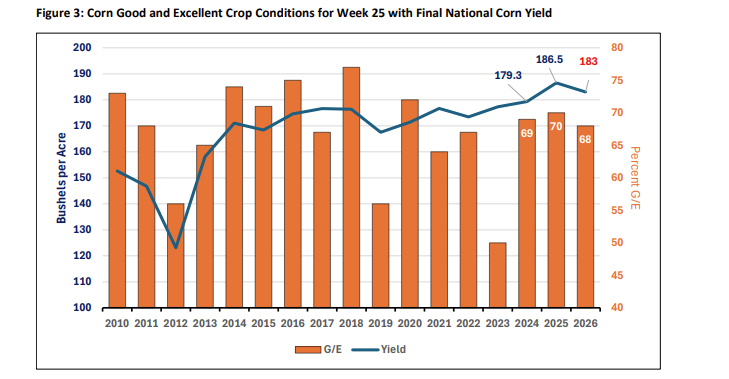

Corn crop conditions continue to improve as we approach the critical period for corn development in July. Good and excellent conditions for Week 25 sit at 68 percent and on par with conditions at this time last year when the U.S. corn crop eventually came in at 186.5 bushels per acre. Good and excellent conditions in Week 25 have little predictive power for final yield but do give a good indication of potential directional magnitude. USDA’s current yield forecast of 183 bushels per acre remains a decent forecast. Acreage at this point is the key question.

Next week’s acreage and stocks reports will frame the market through pollination. USDA’s Prospective Plantings report came under criticism for placing corn acreage at 95.3 million acres. The speculation only increased with the increase in fertilizer prices and fuel costs. The prospect of lower corn acreage in the June report is not clear cut. The possibility of lower corn acreage is an important consideration, but an expectation of a massive acreage switch may be too hopeful.

Less talked about but just as important for prices is the June 1 corn stocks report. Corn demand has been good and yet cash prices are not narrowing across large parts of the Corn Belt. The stocks report will give an indication of feed and residual usage. Exports have been strong with export sales data indicating total commitments of 3,304 million bushels through June 11, on track to hit USDAs recently raised forecast of 3,325 million bushels. While ethanol usage of corn remains strong, USDA lowered the usage total by 25 million bushels to 5,575 million as expected. Feed and residual usage of 6.2 billion bushels is massive and indicates a third quarter feed and residual number in the 930 – 1,130-million-bushel range. A bearish stocks number will be a market mover.

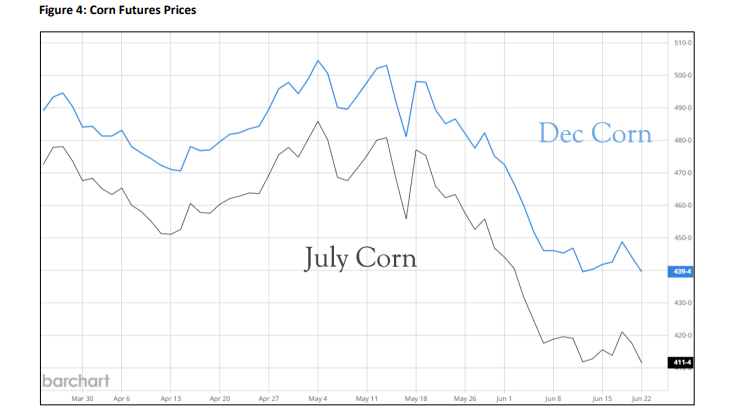

December corn futures moved lower to close at $4.39 yesterday. The December future price sits at the lowest close price for the contract. The July contract closed at $4.11 on Monday, down close to the contract lows seen last week. Cash prices across Oklahoma locations range between $3.66 – $3.71 with higher prices reported in locations.

Milo basis remains weak with basis reports off the July contract coming in at -100 to -120 across the state. Harvest basis sits at -95 to -110.

Milo planting sits at 84 percent of the expected 6.1 million acres revealed in the March Prospective Plantings report. The planting pace is consistent with the five-year average pace at this point in the planting season. Oklahoma came in at 78 percent planted while Kansas and Texas are at 77 and 96 percent, respectively. The initial release of milo crop conditions for the crop year came out yesterday as well. Good and excellent conditions for the six states totaled 51 percent, down 10 percent from last year. Poor and very poor conditions equaled 13 percent, up from six percent last year. Colorado provided the worst conditions by far with 57 percent of the crop coming in as very poor.

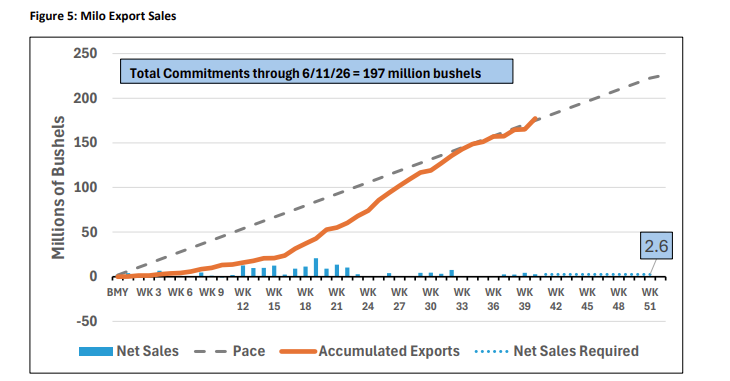

Milo demand is working through the large old crop. Ethanol usage remains robust. Milo stocks will provide further clarification on feed and residual for the old crop marketing year. Export sales data place total commitments of milo at 197 million bushels through June 11. Outstanding sales sit at 19 million bushels of commitments. Sales picked up in late May and early June. Weekly net sales averaged 3 million bushels per week over the period. The Chinese and unknown destinations possess remain the destinations with the most pending sales. China has outstanding sales of 5 million bushels with unknown destinations holding 14 million bushels. Exports continue tracking the forecast of 225 million bushels for the marketing year.