Commodity markets continue to respond to press conferences and social media posts about the Iran war. The status of the Strait of Hormuz remains unclear with timelines for the ending of the conflict ranging from a week to months. Regardless of the timeline, elevated energy prices look to hold well into the fall. Greater volatility in agricultural markets stays as the base scenario as we enter spring planting season. USDA releases a WASDE report on Thursday with expectations of minor changes across commodity balance sheets.

Wheat Market Outlook

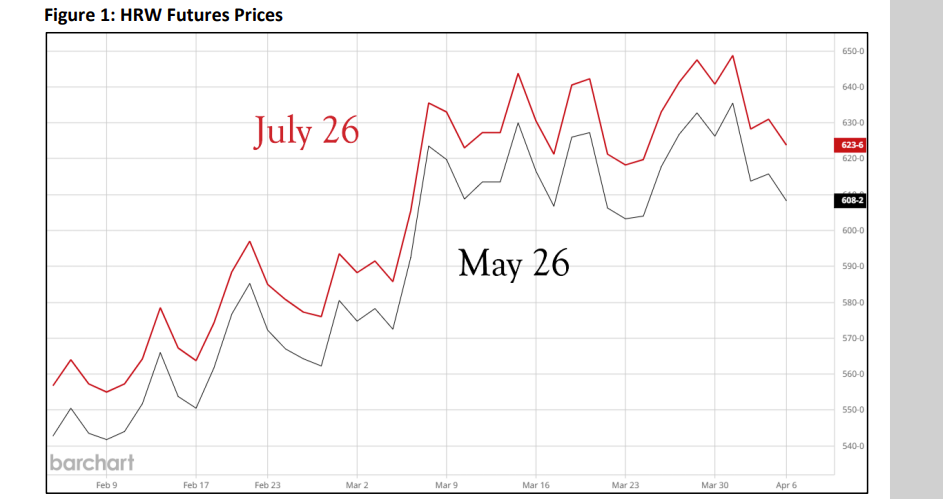

Futures prices across the wheat complex moved lower on Monday. Prices moved higher on the Prospective Plantings report last week due to lower acreage across wheat classes. Since that price run up, HRW futures moved lower on weather and weakness in exports. May HRW futures closed at $6.08 on Monday in the lower end of the $6-$6.50 range prices moved in since early March. After climbing as high as $6.48 following the USDA reports, May HRW prices lost momentum. July harvest contract prices closed at $6.23 and, like the May contract, sits in the lower part of the $6.20-$6.60 range it has occupied since early March.

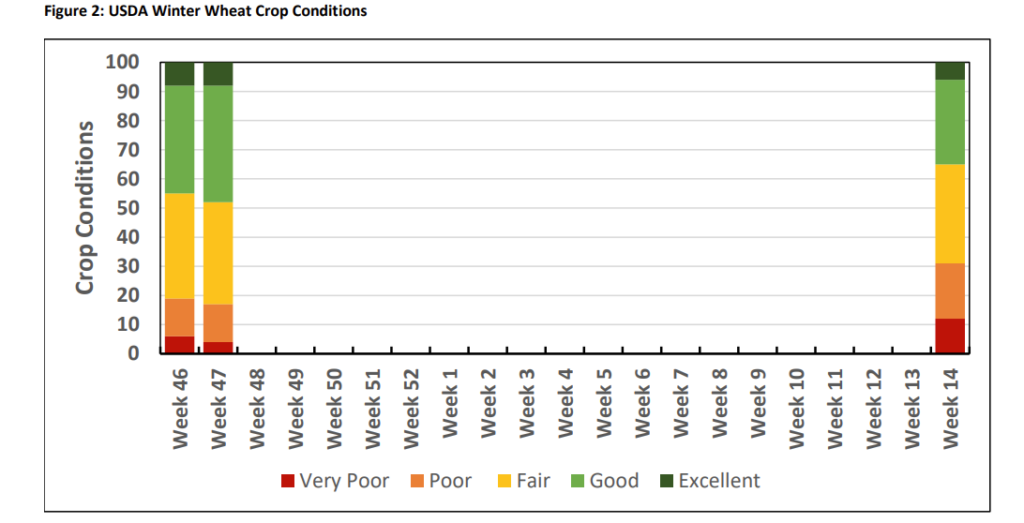

Despite recent rains for portions of the driest winter wheat areas, weather remains an issue. Last Thursday’s drought readings for March 31 placed 65 percent of the winter wheat crop in various levels of drought with expansion in the extreme drought category. The area in drought increased by eight percent from the previous week. USDA crop conditions reflected the poor weather over the last few months. The percentage of the national crop rated poor or very poor expanded to 31 percent from the prior 17 percent. Oklahoma’s poor and very poor categories tallied 54 percent, a 30 percent increase from last fall. The crop condition index fell 37 points to 298, well below the five-year average of 316 for this point in the growing season.

Hard red wheat winter export sales data places total commitments at 315 million bushels through March 26. Outstanding sales make up 47.3 million bushels of the commitments total for the year. Mexico is on record for holding 17.9 million bushels of those outstanding sales, while Japan, Taiwan, and other Asia destinations have 12.1 million bushels. Total commitments for all wheat equal 886 million bushels through March 26.

Corn/Milo Market Outlook

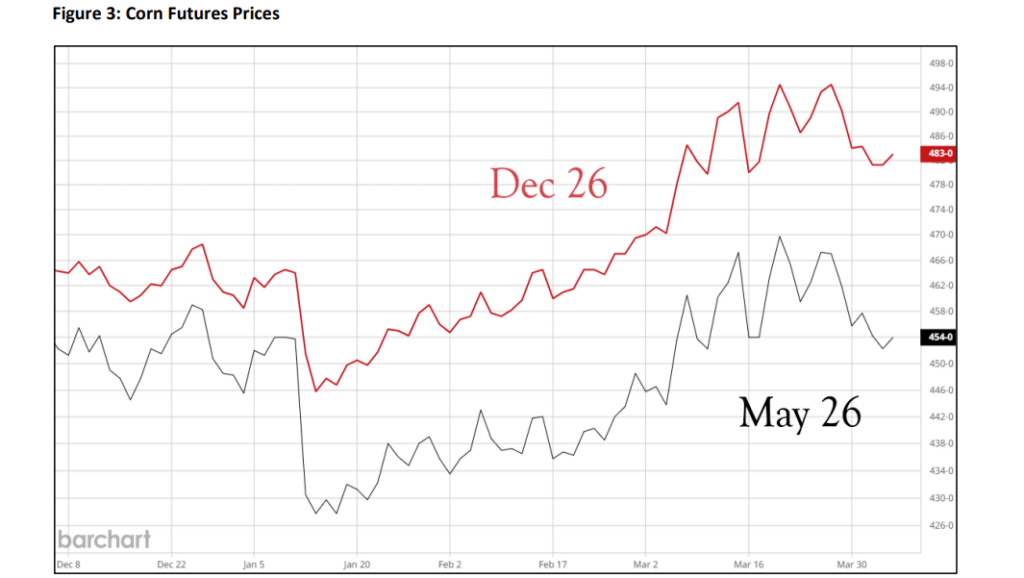

December corn futures came under slight pressure after the USDA report suggested 95.3 million acres this year. December prices settled at $4.83 per bushel yesterday. Corn prices continue to reflect a massive crop despite the strong demand. The May contract closed at $4.54 on Monday, down marginally from last week. Cash prices across Oklahoma locations range between $3.99-$4.24.

USDA’s projection of 16.47 billion bushels of corn usage remains feasible after the March 31 stocks report. Export sales data for corn through March 26 place total commitments at 2.76 billion bushels with outstanding sales consisting of 901 million bushels. Corn exports need to average 24.7 million bushels per week for the remainder of the marketing year to hit the forecast.

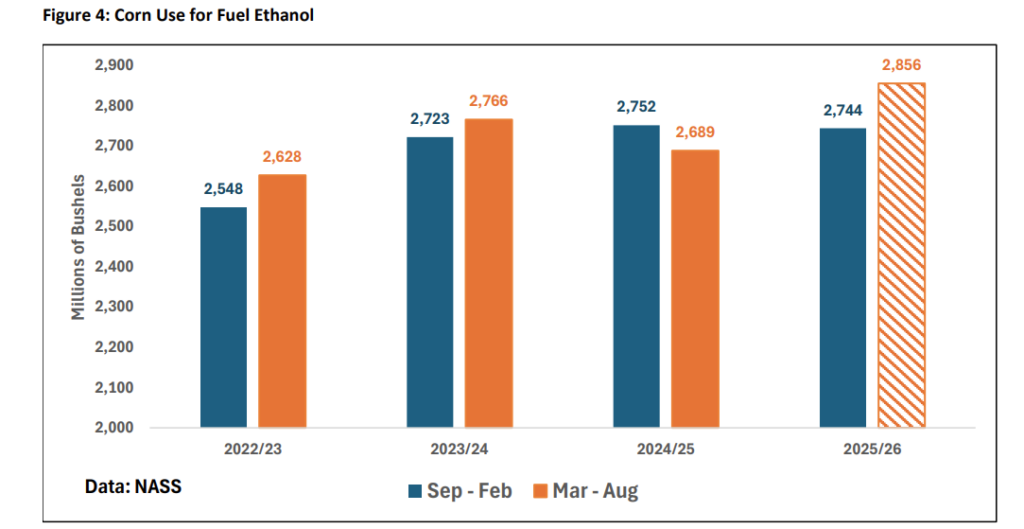

Ethanol grind for corn needs to pick up the pace to meet USDA’s 5.6-billion-bushel forecast. The first half of the 2025-26 marketing year of corn use for fuel came in at 2.744 billion bushels, down eight million bushels from last marketing year. To hit the current forecast, 2.856 billion bushels are necessary for the second half of the marketing year.

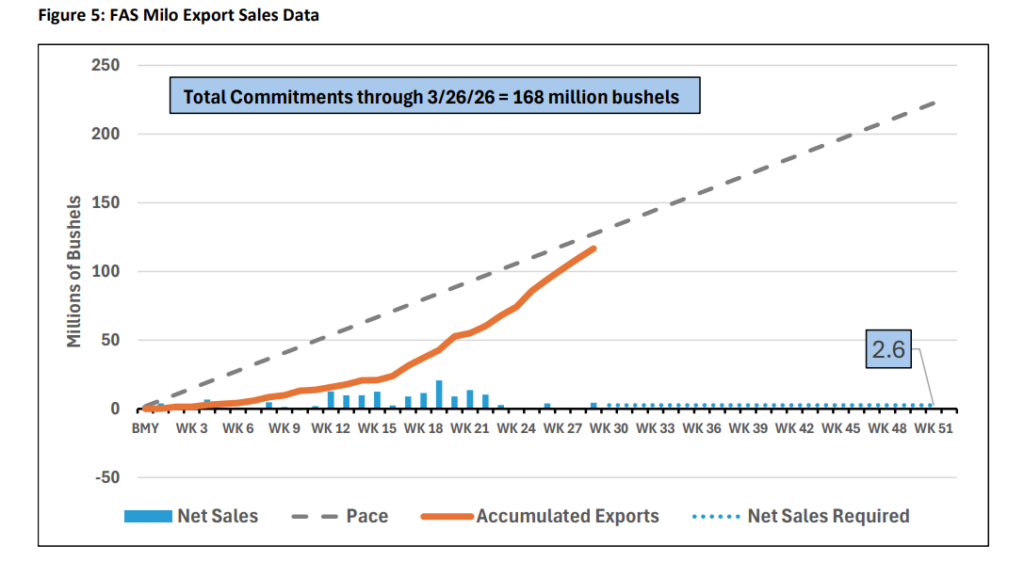

Milo basis ranges from -105 to -115 off the May corn contract across substantial portions of the state. Cash prices ranged from $3.39-$3.49. Harvest prices ranged from $3.73-$3.88. Milo usage for ethanol totaled 54 million bushels through five months of the marketing year. Export sales data place total commitments of milo at 168 million bushels through March 26. Weekly sales need to average 2.6 million bushels a week to hit the forecast