Grain markets continue to reflect the ample supply available around the globe with volatility emerging on an event driven basis due to geopolitics, weather, and trade. As the markets move into spring planting season, an expectation of recent price dynamics continuing seems a reasonable assumption given the uncertainty in place. Farm Director KC Sheperd notes that these shifts remain critical for Oklahoma producers as the season progresses.

Wheat Outlook

USDA’s WASDE report provided slightly bearish to neutral information for wheat markets last week. Prices moved lower in hard red winter wheat contracts after the release of the data. On Monday, HRW futures contracts popped higher on geopolitical issues as the Iran war negotiations fell apart and the U.S. announced intentions to blockade the Strait of Hormuz. KC hard red winter wheat prices jumped yesterday to close at $6.03 in the May futures contract with basis in Oklahoma strengthening slightly and ranging from 70 to 75 cents below the May contract. July futures prices closed at $6.16, up 11 cents. July HRW price still sits in the lower end of the $6.05 – $6.60 range seen since the onset of the conflict. Expect more volatility. July contract basis narrowed a bit as well to 40-50 cents under in many locations of Oklahoma.

On the domestic balance sheet, the WASDE report lowered seed usage by one million bushels on lower acreage from the Prospective Plantings report. Imports were increased by five million bushels on pace thus far in the marketing year. Projected ending stocks came in at 938 million bushels, up seven million from last month. The changes were not a surprise to the market and did not change expectations for demand during the remainder of the marketing year.

Exports remained at nine hundred million bushels. All wheat export sales data through April 2 shows total commitments at 892 million with 149 million bushels constituting outstanding sales. Hard red winter wheat export sales data has commitments at 316 million bushels with 44 million of outstanding sales. Exports remain on pace for current forecasts on the marketing year.

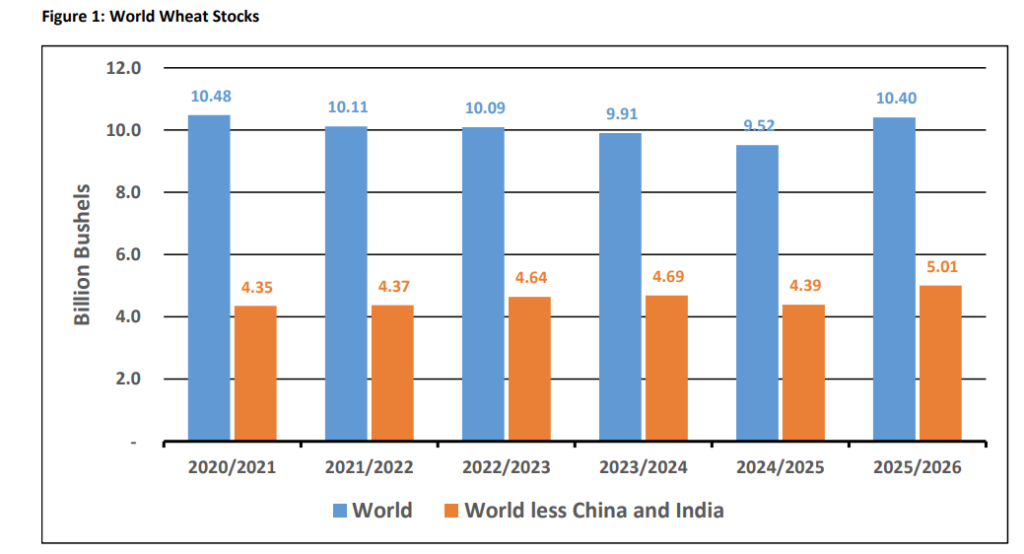

The global picture from the WASDE report increased world wheat stocks to 10.4 billion bushels, an increase of 244 million bushels from last month. Most of this increase in ending stocks (174 million bushels) came from India due to a larger than expected stocks total in the last national report. Larger projected crops in the EU, Argentina, and Russia led to the production increase of 75 million bushels. The Argentinian crop increased marginally to 1.025 billion bushels. The Russia crop totaled 3.32 billion bushels, up an additional thirty million bushels. Production in major exporters is up to 13.35 billion bushels on the trade year with exports down marginally to 8.15 billion bushels.

The growth in stocks driven by India provides marginal impact to the global trade picture with recent sales to Bangladesh reported and much of the wheat remaining in country. The growth in ending stocks outside of China and India during the trade year reflect reduced exports from Ukraine, a slight increase in U.S. stocks, and a plethora of marginal changes around the world. Expect wheat prices to reflect weather and geopolitical events over the near term.

Yesterday’s crop progress report reflected weather developments with the winter wheat crop on the Plains. Conditions saw the excellent category fall one point while the poor category increased by one. This resulted in the crop condition index commonly used in industry falling from 298 to 295. On a state level, Oklahoma’s crop conditions showed marginal improvements as the very poor and poor categories fell six points to 48 percent. Kansas conditions deteriorated from the previous week with very poor and poor conditions increasing to 32 percent from 24 on the week ending April 5. Weather models continue to forecast 2-3 inches of rain along similar routes previous systems have traversed across the Southern Plains over the next two weeks.

Soybean Outlook

Soybean May futures prices continue to move in a narrow range seen since mid-March. May contract price closed at $11.62 yesterday coming off the range highs to close out last week. The prospect of May prices moving out of the $11.55- $11.80 seem unlikely over the near term. November prices have gradually ground higher since mid-March and closed yesterday at $11.50, down eight cents from Friday. Since biofuel policy saw some closure in the uncertainty surrounding policy implementation, soybean prices look set to focus on geopolitical issues, trade uncertainty, and weather. Cash prices in Oklahoma for delivery came in at $10.67 – $10.72 around the state.

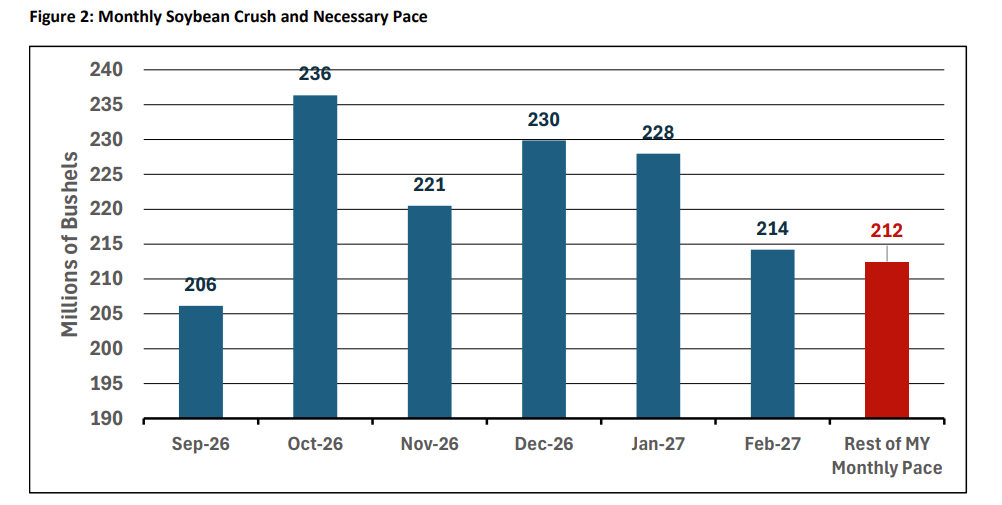

USDA raised crush 35 million bushels and lowered exports by an offsetting amount to keep ending stocks at 350 million bushels. At 2.61 billion bushels, the increase in soybean crush expectations reflects the soybean crush pace through the first half of the marketing year. Monthly crush levels averaged over 222 million bushels per month through February and totaled 1.33 billion bushels. A monthly pace of 212 million bushels per month is necessary to hit the expanded crush total for the marketing year. Due to differences in days per month, the actual monthly totals will vary over the remainder of the marketing year, but the ability to hit 1.275 billion bushels over the last six months is very feasible.

Exports being lowered to 1.535 billion bushels reflects the recent pace and expectations of intense competition out of South America. Export sales data places soybean export pace at 90 percent of the new forecast, which is behind the average pace of 95 percent of commitments at this point in the marketing year. Brazilian exports continue to ramp up with March estimates at 533 million bushels, slightly behind last year’s level. Brazilian exports in April are forecast at 580 million bushels, up 54 million bushels from last April. USDA left major exporter production levels for the 2025-26 marketing year unchanged with an increase of Brazilian exports to 4.22 billion bushels. The international picture for soybeans changed little in the last WASDE.

Soybean meal supply increased on the change in crush by 800 thousand short tons. All the increase in soybean meal supply went into domestic usage as recent data reflects the strong usage of meal inside the U.S. Soybean meal exports stayed at 19,400 thousand short tons as export data places pace right on track to hit that total.

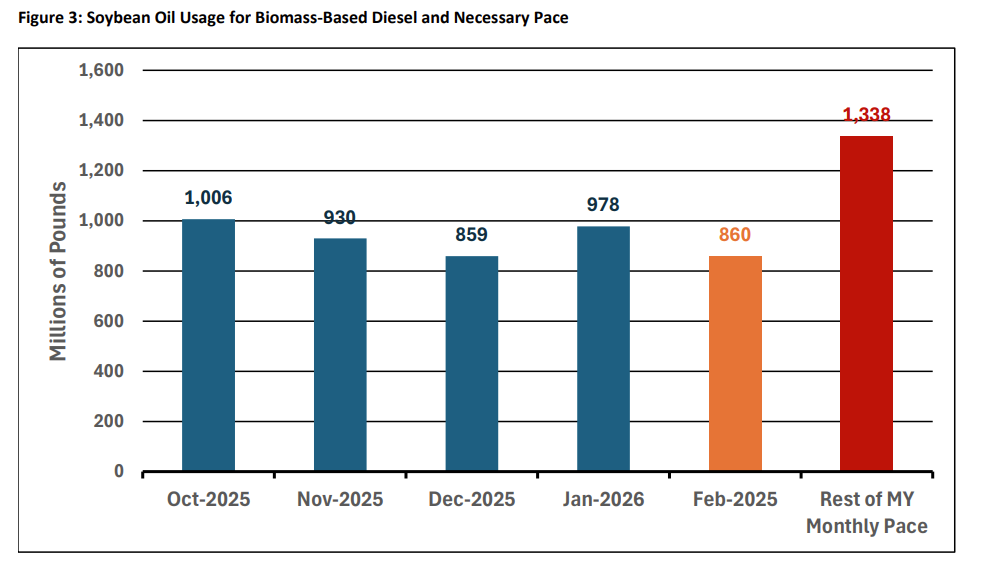

The adjustment to soybean crush saw USDA increase soybean oil production and reduce imports to place supply up 360 million pounds. Domestic usage other than biofuels saw 300 million pounds added to the usage total with the other 60 million pounds of supply going to ending stocks. Soybean oil use for biofuels remains flat at 14 billion pounds.

The growth in crush is related directly to expectations of a bullish policy around biofuels usage that has happened with the release of the renewable volume obligation late last month. Despite that, the ability to hit the 14 billion pounds remains tentative given the slow start to the marketing year under all the policy uncertainty. Current EPA data shows that soybean oil usage for biofuels needs to average approximately 1.355 billion pounds per month for the remainder of the marketing year to reach targets. Every month would be a new record for soybean oil usage for biofuels. Biomass-based diesel production needs to pick up to meet the mandates put forth in the Renewable Fuels Standard. Soybean oil prices climbing above 65 cents per pound reflects this reality.