OSU’s Todd Hubbs writes in his weekly market letter: Commodity markets remain sensitive to outcomes in the Middle East. Weather issues are starting to move to the forefront as spring planting gets underway. As has been stated over the last few weeks, expect higher volatility in agricultural markets over the near term with large price swings possible on any given day depending on the news. This week’s newsletter provides a brief update on farm diesel prices.

Wheat Market Outlook

Hard red winter wheat markets in Oklahoma reflect the impact of weather on this year’s crop. July basis has strengthened in most locations across Oklahoma over the last month. Depending on the location, basis has moved 5–10 cents for harvest contracts. Crop conditions and geopolitical considerations will drive prices over the near term.

Table 1: Oklahoma cash hard red wheat prices select locations

| Date | Pond Creek (May) | Pond Creek (July) | Weatherford (May) | Weatherford (July) |

| 23-Mar | $5.28 (-75) | $5.68 (-50) | $5.23 (-80) | $5.48 (-70) |

| 31-Mar | $5.60 (-75) | $5.99 (-50) | $5.61 (-75) | $5.84 (-65) |

| 6-Apr | $5.33 (-75) | $5.74 (-50) | $5.33 (-75) | $5.59 (-65) |

| 13-Apr | $5.28 (-75) | $5.72 (-45) | $5.33 (-70) | $5.57 (-60) |

| 20-Apr | $5.60 (-75) | $6.03 (-45) | $5.65 (-70) | $5.88 (-60) |

Futures prices in HRW moved sharply higher last week on weather issues and the rally grew as technical trading came to dominate. News of a potential resolution with Iran saw prices fall at the end of last week only to recover slightly on Monday. The veracity of statements about the conflict will remain central to price movements.

July HRW futures closed at $6.47 on Monday after climbing last week to a high not seen since this time last year. The July contract is witnessing the most volume at this point in the marketing year and continually moving with news out of the Middle East and weather announcements. May HRW contract prices closed at $6.35 and sits in the upper part of the $6.02–$6.50 range prices have been bouncing around in since early March.

Crop Conditions

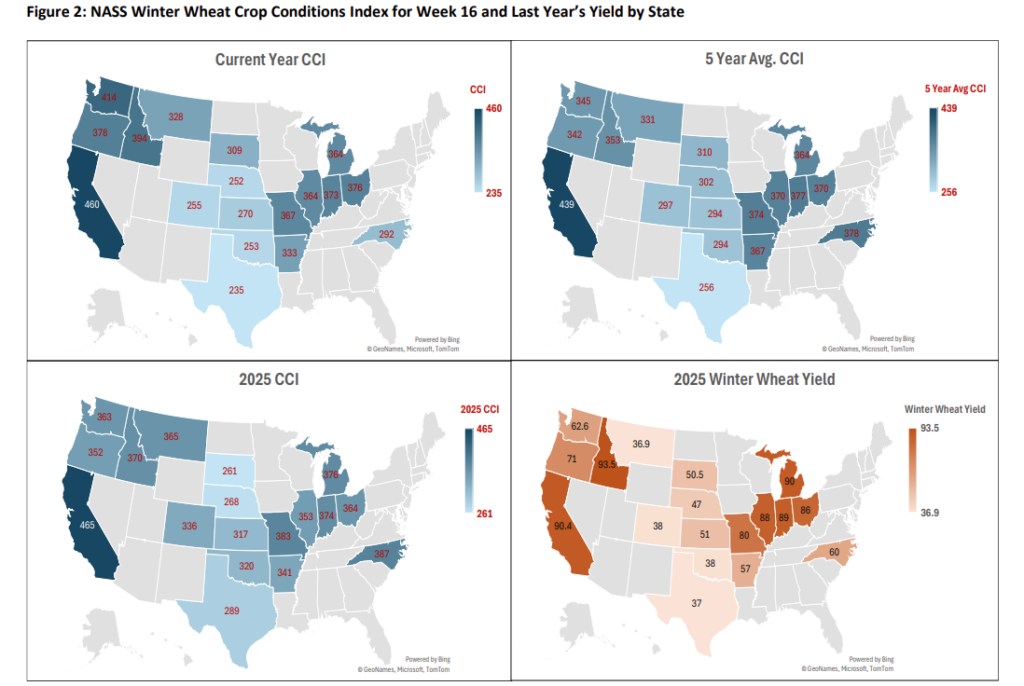

Indicators of winter wheat crop conditions continue to show the potential for a poor crop this year. Last Thursday’s drought readings for April 14 placed 68 percent of the winter wheat crop in various levels of drought with expansion in the extreme drought category to 11 percent. USDA crop conditions remain poor despite recent precipitation events moving through the southern plains.

The percentage of the national crop rated poor or very poor came in at 33 percent. The crop conditions index nationally moved five points lower to 290, well below the five-year average of 316. Oklahoma’s poor and very poor categories tallied 45 percent. Areas growing predominantly hard red winter wheat—Kansas, Oklahoma, Colorado, and Texas—are seeing particularly poor conditions. At this point, it is hard to imagine yields not suffering dramatically given the reported conditions across HRW areas.

Demand and Exports

Demand remains on pace to hit USDA’s forecast. Export sales data for HRW places total commitments at 317 million bushels through April 9. All wheat export sales data shows total commitments for wheat equal 896 million bushels. Commitments sit slightly above the average pace for this time of the marketing year while exports are tracking on normal pace at 84 percent.

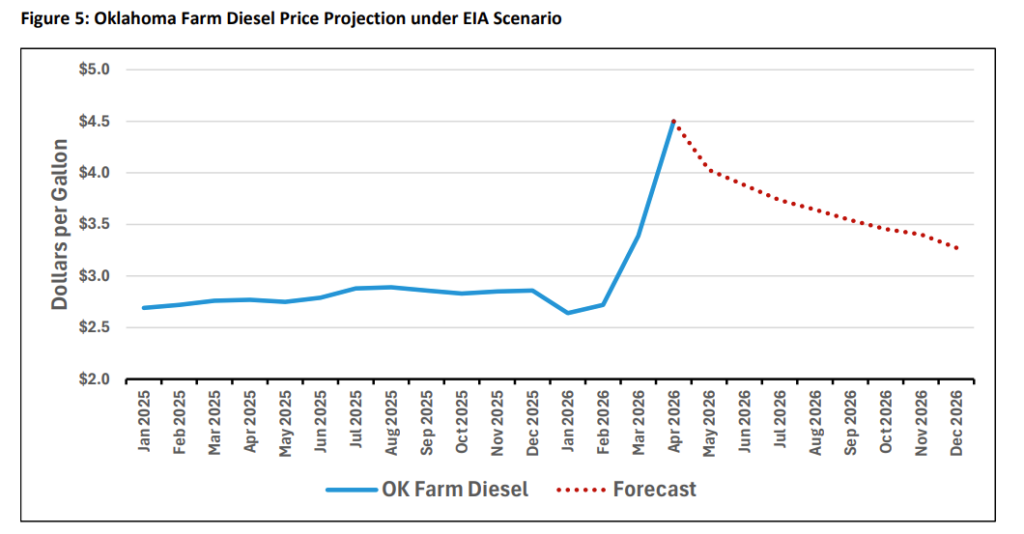

Farm Diesel Outlook

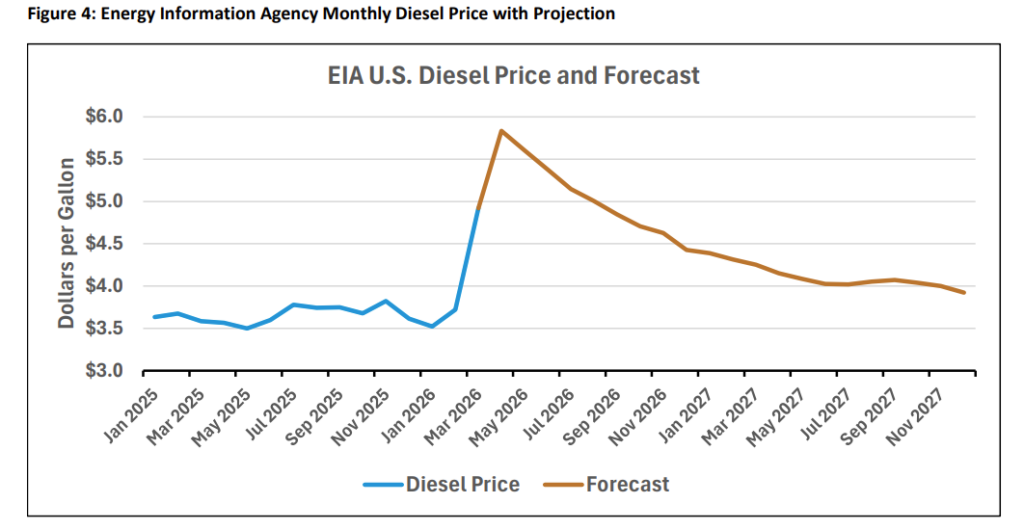

The onset of the conflict in Iran and subsequent shutting of the Strait of Hormuz created an energy price shock rarely witnessed on global markets. Diesel markets around the globe have been particularly impacted. Farm diesel in Oklahoma moved higher as higher world prices drew diesel out of the U.S. onto world markets.

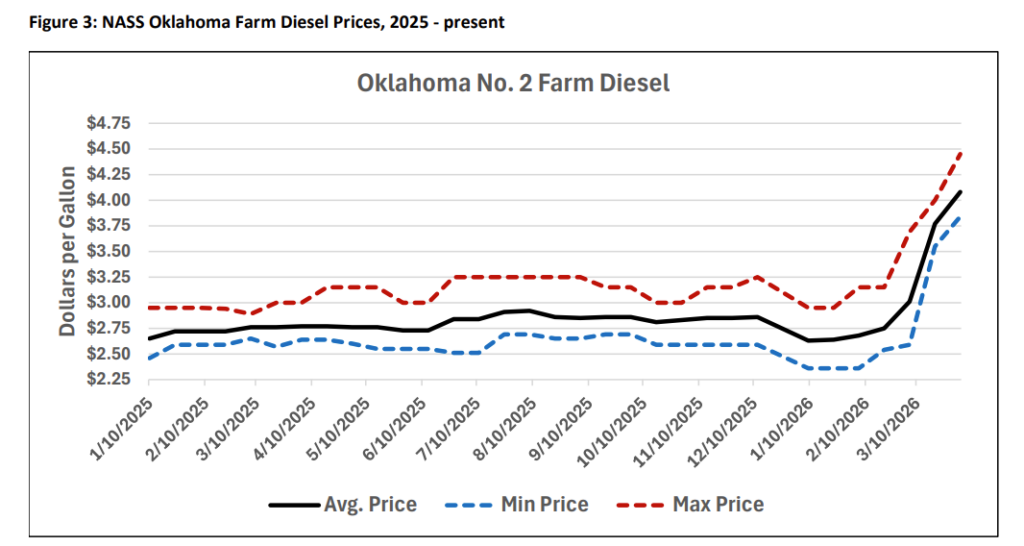

Average farm diesel prices in Oklahoma rose from $3.01 to $4.08 dollars per gallon between March 6 and April 3. Since the last report, prices moved higher with price reports near $4.50. Like most energy shocks, a long tail looks probable for energy prices with gradual relief over the remainder of the year if the conflict gets settled soon.

EIA’s latest projections see diesel prices peaking in April and gradually falling for the remainder of the year, assuming a prompt resolution to the conflict. However, prices are not expected to return to previous levels by the end of 2027. An expectation of elevated prices is in place through fall with prices staying above $3 per gallon and not falling below $4 per gallon until late June.