A combination of favorable weather forecasts and geopolitical factors drove agricultural commodity markets lower over the past week. Grain markets are currently caught in a tug-of-war between strong demand signals and bearish supply realities, including an improving moisture outlook for the U.S. Corn Belt and ample global stocks.

Wheat Market Outlook: A Challenging Week for Futures

Hard Red Winter (HRW) wheat futures completed a difficult week in the July contract, with prices closing lower every single day. Following Monday’s close, July HRW futures dropped to $6.47, retreating to a price range last seen before the market rallied around the May Crop Production report.

Local Cash Prices and Crop Conditions

In Oklahoma, HRW cash prices settled into a range of $5.97 to $6.17 following Monday’s close, while local basis remains relatively stable.

Despite persistent poor crop conditions across the Plains, wheat prices are struggling to gain traction. The domestic market is contending with a poor local crop while facing a large global carryover and minimal crop disruptions elsewhere in the Northern Hemisphere. For HRW prices to find room for another upward move, the market will likely need support from other sectors, such as corn, or from potential crop disruptions in the Southern Hemisphere, where an extraordinarily strong El Niño event is forecast for later in the year.

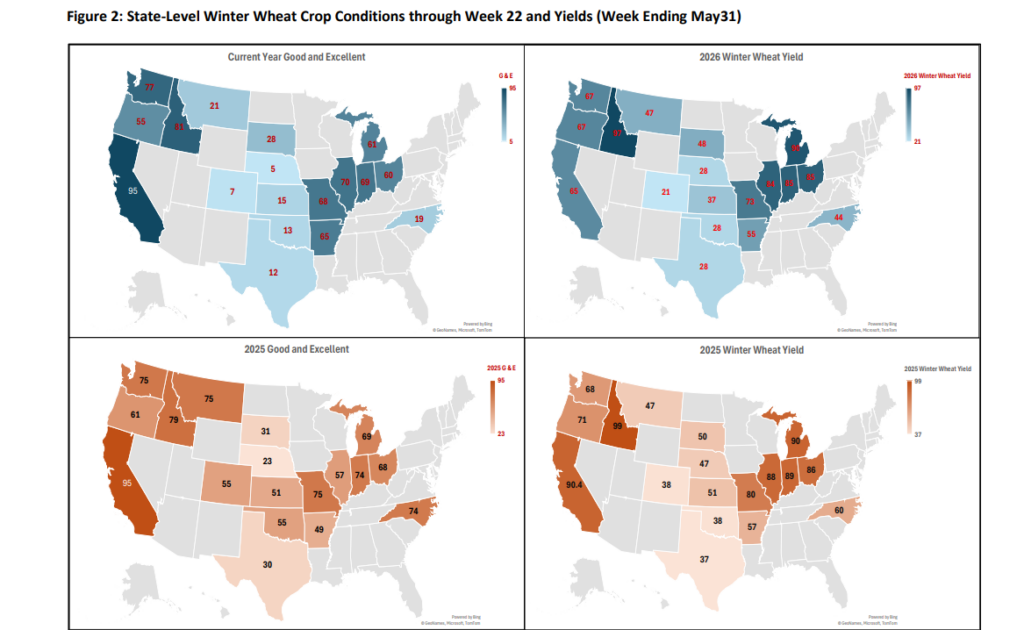

The national winter wheat crop condition index increased by one point from last week to 269, though it sits well below the five-year average for this week of the year. The total percentage of the national winter wheat crop rated good or excellent held steady at 26 percent. Locally, Oklahoma’s good-to-excellent ratings tallied 13 percent, representing a slight increase from the previous week.

Export Pace and Forward Sales

Hard red winter wheat exports remain on track to hit the USDA’s target of 320 million bushels as the end of the marketing year draws near. Total commitments for the current marketing year sit at 319 million bushels, with cancellations and sales roll-overs beginning in earnest as the market transitions to the next marketing year.

Outstanding sales for the 2026-27 marketing year stood at 19.9 million bushels through May 21, down significantly from the 48 million bushels reported at the same point last year. Leading buyers for the upcoming marketing year include Mexico, Japan, and Korea. This year-over-year lag in forward sales is a commonly expected outcome given the sharp reduction in overall domestic production.

Corn Market Outlook: Favorable Weather Cools Prices

U.S. corn futures also moved lower, with December corn closing at $4.72. This puts the December contract at the lower end of the $4.70 to $5.00 range it has maintained since early March. The July contract felt a sharper decline, closing at $4.44 on Monday. Across Oklahoma, local cash corn prices ranged from $3.89 to $3.94, with higher prices reported at select locations.

Crop Progress and Hydration Levels

At this early stage in the season, the U.S. corn crop is progressing without any serious setbacks. Planting is 93 percent complete, and emergence is 75 percent—both metrics are tracking slightly ahead of their respective five-year averages. Pennsylvania and Michigan are currently showing the slowest progress, trailing in both planting and emergence, though this is not yet considered a critical concern. With nationwide planting surpassing the 90 percent mark, the year’s first crop condition ratings were released, indicating a crop on par with last year at 67 percent good-to-excellent (down two percent from the same period last year).

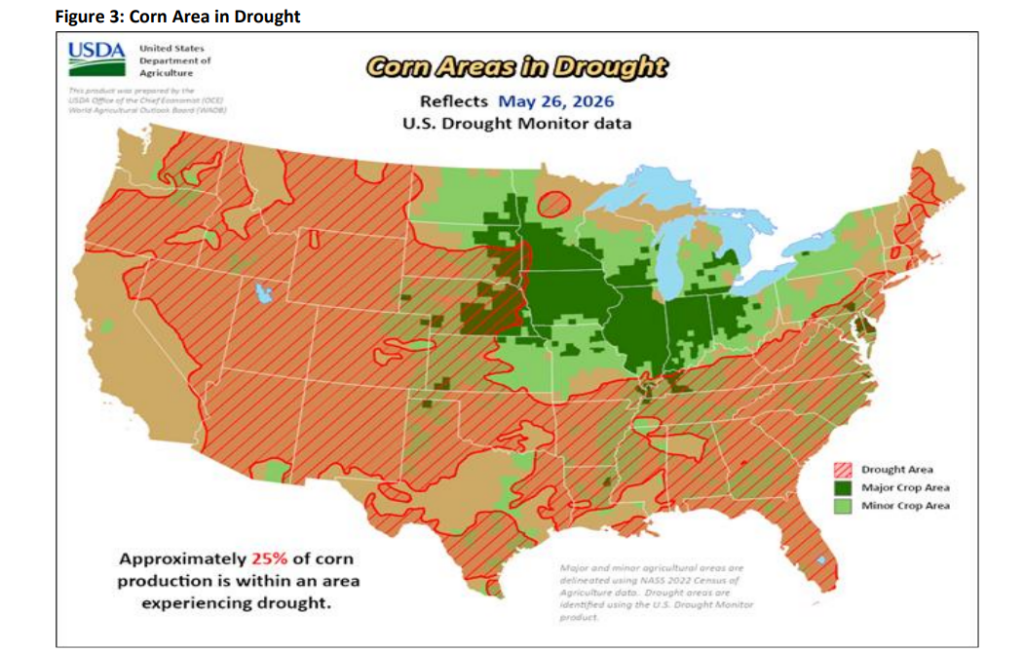

As of May 25, approximately 25 percent of the national corn acreage was situated in drought-affected areas. While recent rainfall improved the driest corn areas in the Deep South and the Plains, dryness has begun creeping into the heart of the Corn Belt over the last few weeks. Weather developments in this region will be critical to monitor, as any increase in extreme dryness could spark speculation about yields and acreage. At present, weather models indicating rain for Nebraska and eastern South Dakota later this week have served as a primary driver of the recent price weakness.

Global Supply Dynamics and Ethanol Demand

U.S. corn demand continues to be sustained by steady ethanol grind and export sales. Export commitments through May 21 reached 3.18 billion bushels, which includes 788 million bushels in outstanding sales. To hit forecasted totals, corn sales and exports must average 8.3 million bushels per week for the remainder of the marketing year. Over the past month, weekly net sales averaged a strong 51 million bushels per week, bringing total commitments to 96 percent of the forecasted total—matching the five-year average.

The U.S. crop is moving through its peak sales window just as South American production begins hitting the international market. In Brazil, the safrinha harvest has begun in parts of Mato Grosso. The full-season crop, which accounts for roughly 24 percent of Brazilian corn production, is mostly harvested with good yields reported. Meanwhile, Argentina raised its corn crop potential in its May report to a record 2.75 billion bushels on higher overall acreage. On the global stage, U.S. Gulf corn prices remain below Brazilian port prices, while Argentinian port prices sit approximately 36 cents a bushel below U.S. Gulf prices of $5.58 per bushel.

Domestically, corn processing for ethanol reached 427.68 million bushels in April, up 4 million bushels from last year. Total corn usage for fuel ethanol through April sits at 3.653 billion bushels, outpacing last year’s year-to-date total by 25 million bushels. To reach the USDA’s full-year forecast of 5.6 billion bushels, corn usage must total 1.947 billion bushels over the remainder of the marketing year (compared to the 1.812 billion bushels used from May to August 2025). Current gasoline consumption trends show little sign of a consumer slowdown, supporting the likelihood of meeting these targets.

Milo Market Outlook: Strong Ethanol Demand vs. Weak Basis

Sorghum (milo) basis remains quite weak across the state, coming in at -90 to -110 off the July futures contract. Local milo prices continue to track corn price competitiveness and overall export market opportunities.

Milo planting has reached 44 percent of the expected 6.1 million acres projected in the March Prospective Plantings report. While the planting pace has lagged the five-year average by 1% for several weeks, it does not currently pose a major concern. Regionally, Oklahoma is 36 percent planted, while Kansas stands at 26 percent and Texas leads at 84 percent complete.

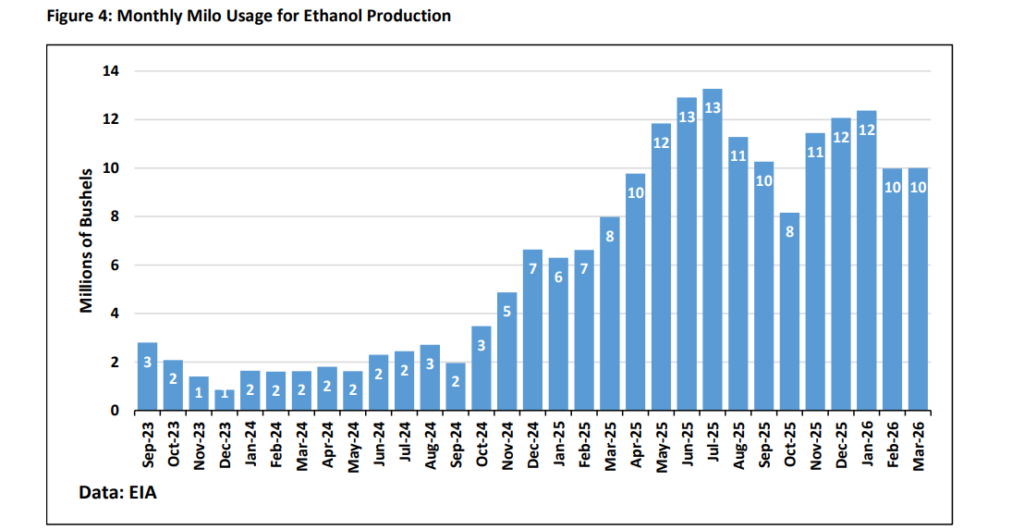

Demand for Milo remains solid, propped up by lower pricing. March data from the Energy Information Administration (EIA) showed that 10 million bushels of milo were used for ethanol production, maintaining a recent trend of increased milo crushing for fuel. To meet the USDA’s current full-year ethanol grind forecast of 113 million bushels, milo usage needs to average 7.7 million bushels per month over the final five months of the marketing year. Because a slowdown of that size seems unlikely, the current pace suggests the market may eventually see stronger feed and residual usage or higher export volumes.

This Crop Outlook Newsletter update is provided by Oklahoma State University Extension Grain Marketing Specialist Dr. Todd Hubbs.