Grain and oilseed futures prices dropped dramatically over the last week, driven primarily by a strong technical move from funds and speculators liquidating long positions. Grains disconnected from oil as the geopolitical premium evaporated. An expectation of favorable crop conditions in the Corn Belt, along with uncertainty regarding the U.S.-China trade situation, exacerbated the price move. However, the market should be nearing a bottom in this oversold situation.

Wheat Market Outlook

HRW futures markets closed lower for 12 straight trading days before clawing back a few cents on Monday. July prices closed at $6.30, remaining in the lower part of the range seen in March and early April before the price runup associated with the deteriorating winter wheat crop. Improving weather conditions in the U.S., along with better-than-expected production from Northern Hemisphere crops, helped to create the bearish conditions. July delivery basis sits at -45 to -55 across the state and remained stable during the price drop. The prospect of the bottom being set is quite high given the issues with the winter wheat crop.

Wheat exports slowed a bit over the last month as the market enters the next marketing year. Outstanding sales for 2026-27 for all wheat are 113 million bushels, down from 123 million at this point last year. The prospect of a much smaller HRW crop this year is showing up in next marketing year sales as U.S. prices moved higher. HRW outstanding sales for the next marketing year sit at 30.4 million bushels through May 28, down from 43.6 million bushels at this time last year.

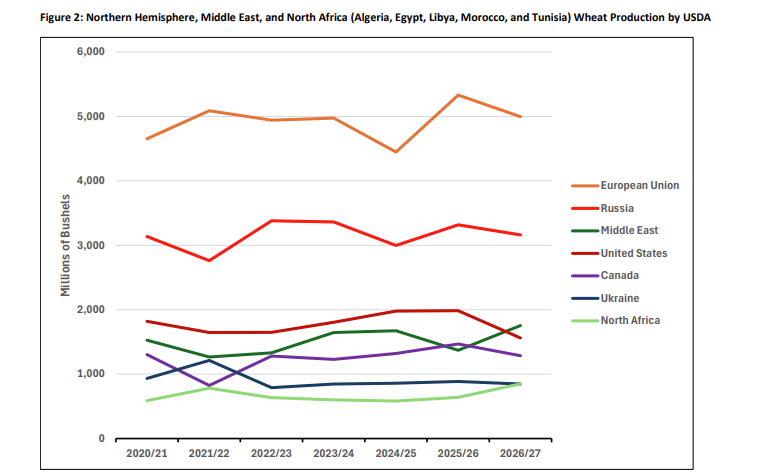

Despite the drastic decline in prices in the U.S. over the last two weeks, U.S. port prices remain above those of major global competitors. USDA’s wheat production forecasts for the 2026-27 marketing year in the Northern Hemisphere, Middle East, and North Africa show that while many areas are down from last year, they still sit at or above longer-term production levels after last year’s large global crop.

- European Union: Forecast at 4.9 billion bushels by USDA, though recent analysis in the EU places the crop at 4.7 billion bushels with ratings falling slightly in France and Germany.

- Black Sea Region: The trade places crop expectations in a positive light, with Russia’s crop pegged between 84 and 88 million metric tons (3.08 to 3.2 million bushels). The USDA number falls in the middle of this range. Ukraine’s crop maintains expectations of 840 to 850 million bushels.

- Canada: Spring wheat crop planting is catching up in the Prairie provinces, and the slight decline in acreage fits with current production forecasts. The spring wheat crop is typically around 96 percent of Canadian wheat production.

- Middle East and North Africa: Crops in Algeria, Egypt, Libya, Morocco, and Tunisia came in higher this year. These countries typically demand wheat in trade, and the larger crops have subdued demand for EU and Black Sea locations.

While overall production is lower this marketing year around the globe, tightening global stocks are still above levels seen from the 2021-2024 marketing years.

Soybean Market Outlook

Soybean futures prices moved sharply lower over the last week despite strong crush data. July futures dropped over 60 cents per bushel during the week to close at $11.16 on Monday, while the November contract closed at $11.35. Futures prices dropped to levels not seen since early March. Cash prices in Oklahoma are around $10.31 to $10.41 with a -85 to -95 basis. Harvest prices came in near $10.45 with basis at 90 under the November contract.

Soybean planting sat at 92 percent as of June 7, which is 4 percent above the five-year average. Crop conditions came in at 67 percent good and excellent, down one percent from the initial report last week, compared to 68 percent at this time last year. The crop is going in at a timely pace with little concern this early in the crop year, particularly with rains forecast across the heart of the Corn Belt.

Soybean Crush and Demand

USDA released soybean crush data for April on June 1, totaling 218.45 million bushels. Crush through April came in at 1,784 million bushels, which is 345 million bushels above last marketing year’s pace. Crush needs to average 211.5 million bushels a month to hit USDA’s forecast of 2,630 million bushels. The monthly average thus far totals 223 million bushels per month. The potential for crush to exceed USDA’s forecast is supported by the fact that strong crush margins favor a continuation of record crush volumes. The current market environment represents a buying opportunity for end users of soybean crush products.

Soybean meal demand remains on track to hit USDA’s forecast in both domestic and export categories. Meal prices fell around $20 per short ton in futures markets last week to close yesterday at $306. Lower prices could spur soybean meal demand to even higher levels. Export sales data show soybean meal total commitments at 17,580 thousand short tons through May 28, remaining on pace to hit the USDA forecast.

Soybean Oil and Exports

Soybean oil (SBO) prices touched 79 cents per pound early last week before selling off to 73 cents yesterday. Prospects for increased SBO usage in biomass-based diesel production are high given obligated party production under the RFS sits well below what is necessary to meet volume obligations in 2026. SBO exports continue to contract as expected due to prices sitting above global levels and strong domestic demand. A recovery in SBO prices is expected moving forward.

Soybean export sales data through May 28 place U.S. total commitments for soybeans at 1.468 billion bushels. Weekly new sales ticked up in May, but exports appear destined to miss USDA’s current forecast. Brazilian exports since harvest began in earnest in March are up year over year. However, the recent price drop saw U.S. Gulf soybean prices narrow to 21 cents a bushel higher than port prices in Paranaguá. An expectation of China bargain shopping for U.S. soybeans should be in place given this dramatic price change.

Meanwhile, Argentina announced soybean export duties, currently at 24 percent, will be lowered by 0.25 percent a month in 2027 and accelerated on a monthly basis in 2028. Whether this policy holds and comes into effect remains an open question that bears monitoring.