OSU’s Todd Hubbs writes: On Thursday, June 11, USDA released the Crop Production and WASDE reports. The June Crop Production report confirmed the poor winter wheat crop, but prices remain weak. Initial reports of an agreement between the U.S. and Iran led to a drop in energy prices and will hopefully bring a risk-on scenario that can find support for agricultural commodities. The reports were not particularly bullish for any crops. This newsletter reviews the major takeaways and implications from those reports.

Wheat Market Outlook: Hard red winter wheat prices continue to struggle for purchase despite the supportive USDA June Crop Production report. HRW July futures price sits at $6.40 after the close on Monday. Despite minor support after the USDA reports last Thursday, wheat futures prices sit in the range of $6.15 – $6.40 last seen in March. At present, HRW prices finding strength over the near term appears limited as international supplies and competitor prices limit rally potential. Wheat prices continue to work through the information from geopolitical events. In combination with expectations of lower production, HRW prices should remain sensitive to developing crop potential around the globe and any developments with spring crops. In Oklahoma, cash prices for July delivery converged with prices in the $5.95 – $6.05 range.

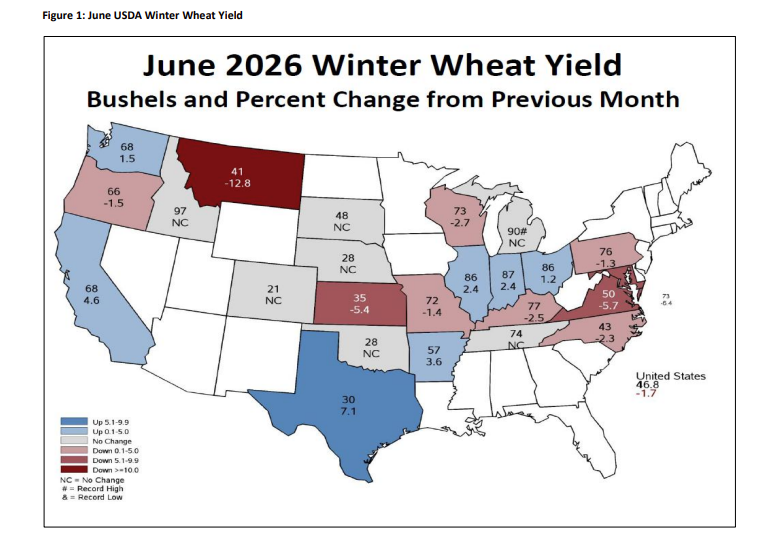

The USDA reports confirmed the poor conditions in HRW countries and corroborated the recent stories about international crops circulating. Domestically, the USDA winter wheat production report for June came in at the lower range of analysts’ estimates. At 1.03 billion bushels, the estimated winter wheat crop sits 26.5 percent lower than last year. All classes of winter wheat dropped in total production except for soft white wheat. HRW production fell another 17.9 million bushels to 497 million bushels. A substantial drop from last year’s 804 million production level. HRW’s production drop encapsulated the production losses for winter wheat as the total winter wheat crop fell 17.8 million bushels, with minor changes to the other classes.

Harvested acreage remains unchanged in the June production report as potential acreage adjustments focus on the June Acreage report due out on June 30. As shown in Figure 1, winter wheat yield is estimated at 46.8 bushels per acre. Yield changes from the May report varied, with a 2-bushel-per-acre drop in Kansas yield significantly impacting HRW production. Texas HRW yield increased by 2 bushels, with Oklahoma remaining at 28 bushels per acre. Soft red winter production totaled 300 million bushels, down .6 million bushels from last month’s forecast. Higher yields in Illinois, Indiana, and Ohio offset issues elsewhere, limiting losses.

On the domestic balance sheet, the WASDE report left the 2025-26 balance sheet unchanged as usage continues to converge on the estimates. Lower winter wheat production is reflected in the new-crop balance sheet for wheat. Wheat production is forecast at 1.54 billion bushels, with supply at 2.62 billion bushels, down 346 million bushels from last marketing year. To incorporate the 18-million-bushel drop, ending stocks for the 2026-27 marketing year were lowered to 742 million bushels. Usage was left unchanged. A tendency among the trade to discuss a tightening balance sheet for wheat is understandable, but the global picture right now lessens the bullishness associated with the U.S. crop.

2026-27 world wheat production came in at 30.13 billion bushels, down 892 million bushels from the 2025-26 crop. Smaller projected crop output in Australia, Pakistan, and the U.S. was offset by higher expectations for Russia, Ukraine, and Turkey. Expect a major amount of discussion about the “Super El Niño” along with the Australian and Argentine wheat crops later this year. USDA currently places Australian production at 1.03 billion bushels, down almost 300 million from last year. While Australian crop potential could deteriorate further, the overall production level will probably not see a large change given the current expectations already incorporated into the world balance sheet. The Russia crop totaled 3.23 billion bushels, up 73 million bushels from last month. Turkey’s production increased to 826 million bushels, bringing potential price pressure in the Black Sea, EU, and MENA regions into focus in the near term.

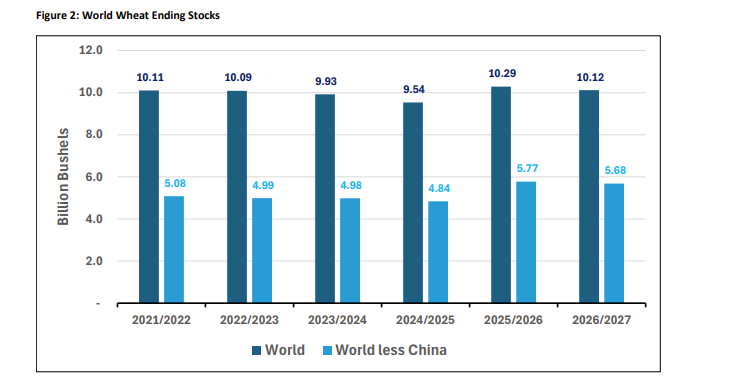

As shown in Figure 2, ending stocks outside of China are forecast at 5.68 billion bushels, a slight increase from last month. Ending stocks sit well above the levels seen from 2021 to 2024 marketing years, despite issues with major crop producers. In compensation for lower production, global trade in wheat is expected to fall, with trade-year exports for 2026-27 totaling 7.8 billion bushels. Domestic consumption of wheat for feed usage around the globe is expected to fall as well.

Corn/Milo Outlook: Corn prices reflect the improvement in weather domestically along with improved global supplies. July corn futures moved up two cents to close at $4.15 per bushel on Monday. December corn futures followed suit to close at $4.42. Both prices have fallen to marketing year lows. The outcome from the stocks and acreage reports at the end of the month will set the tone into pollination. Corn in Oklahoma was priced on average around $3.70 per bushel with harvest prices in the $4.06 – $4.16 range.

The corn balance sheet saw a couple of changes to the old crop balance sheet. Corn usage for ethanol dropped 25 million bushels to 5,575 million bushels, reflecting a slower pace through the first seven months of the marketing year. The lowered ethanol usage was offset by a 25 million bushel increase in exports. At 3,325 million bushels, the corn export forecast reflects the continued strength in corn export sales. While sales have slowed over the last month, current levels remain robust enough to meet the new projection. Imports were raised 3 million bushels to 28 million which moved ending stocks slightly higher. No changes occurred to the new crop balance sheet other than the three-million-bushel increase in beginning stocks moving down into ending stocks for the new crop marketing year. Crop conditions continue to improve with good and excellent conditions through June 14, sitting at 58 percent. Speculation around the Acreage report appears set to set the tone for price action, barring a sudden deterioration in weather.

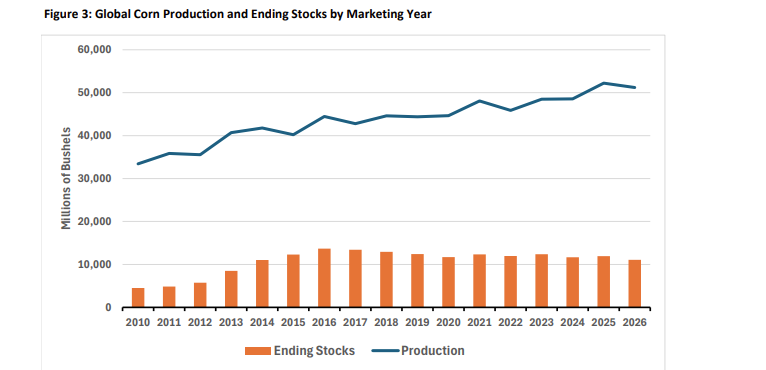

As seen in Figure 3, corn global production is forecast at 51.2 billion bushels, down 1,035 million bushels from the last marketing year. Back year corn production jumped 550 million bushels on larger corn crops projected for Argentina (up 2 MMT), Brazil (up 3 MMT), and India (up 8.9 MMT). The 2025-26 corn crop saw a reduction for Mexico but pales in comparison to the larger crops that add to global ending stocks for 2025-26. The 2026-27 corn crop saw a 5 MMT increase in India. The substantial changes to India’s last two crops were due to acreage adjustments. The results of these changes place ending stocks at 11.1 billion bushels for 2026-27, down 871 million bushels, and indicate tightening to the global balance sheet. Growing crops in South America, hitting the global market, along with the prospect of a good U.S. crop, places pressure on corn prices.

Soybean Market Outlook: Soybean futures prices moved higher yesterday providing a minor recovery after dropping almost 75 cents over the last two weeks. Soybeans fell marginally after the June WASDE as the large soybean crops in South America come to fruition. The July soybean contract moved six cents higher to sit at $11.19 and the November contract closed at $11.34, up two cents. Soybean prices remain under pressure due to large harvests in South America and weakening exports domestically. While crush levels appear sustainable at recent elevated levels, U.S. competitiveness on global markets will be impacted by elevated domestic prices. Cash prices in Oklahoma sat at $10.34 – $10.39 for delivery. Harvest prices came in at $10.44.

Old crop soybean balance sheet saw crush raised another 20 million bushels to 2.65 billion as crush pace in the 2025-26 marketing year remains at an elevated level. Exports were lowered 20 million bushels to offset the crush change and give a hat tip to the massive crops coming out of South America. Ending stocks stayed at 340 million bushels. The new crop soybean balance sheet remained unchanged from the initial forecast in May. Barring a major change in the soybean crop production potential, the new crop balance sheet will remain stable.

Soybean oil production increased 180 million pounds on stronger crush with soybean oil use for biofuels forecast to hit 14.55 billion pounds this marketing year, up 350 million pounds. USDA’s increased projection for biofuel usage implies a monthly usage of 1,405 million pounds a month for the remaining six months of the soybean oil marketing year. The ambitious forecast is based on the potential for biomass-based diesel production under the new renewable volume obligations. The monthly rate is beyond anything that has ever been achieved in soybean oil biofuel use. Decreased exports of 150 million pounds offset the drop in biofuels usage and underscores the poor pace of oil exports with U.S. prices well above global prices.

Soybean meal production is up 425 thousand short tons under the new projection. Domestic usage (up 250 thousand) and exports (up 200 thousand) combined to use the increased production, with a 25 million-bushel increase in imports. Increased imports may seem strange given the massive crush and domestic usage, but soybean meal imports classified as organic tend to absorb those import tons. Lower prices for meal are expected to drive a strong demand in 2026-27 and an expectation of U.S. market share in export markets maintaining the current levels is in place with intense competition from South America.

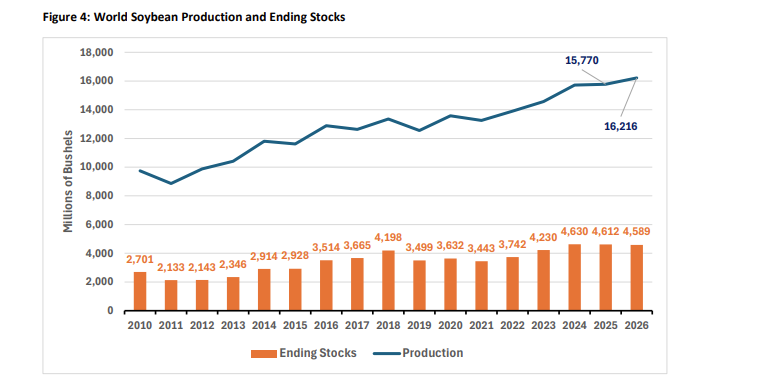

As shown in Figure 4, global soybean production for 2025-26 was forecast at 15.77 billion bushels, up 59 million bushels from May. The change was driven by an increase in the Argentine bean crop by 2 MMT to 50 MMT. One should not be surprised if the Argentine crop grows further still before it is finalized. Major exporters in South America are expected to produce 8.96 billion bushels with ending stocks in the region (Brazil, Paraguay, and Argentina) coming in at 2.3 billion bushels, on par with 2024-25 levels. Global ending stocks are projected to fall slightly in old crop and new crop marketing years and remain well above levels seen even during the trade war years in the late 2010’s. The prospect of South American production slowing over the next few years seems slim, despite discussions of energy and fertilizer costs in the region.