Following the highly anticipated release of today’s USDA acreage report, significant revisions are sparking discussion across the agriculture industry. Farm Director KC Sheperd sat down with Allendale’s Rich Nelson to break down the surprise shifts in corn, soybean, and wheat acreage and what these numbers mean moving forward.

Old Crop Stocks Shrink More Than Anticipated

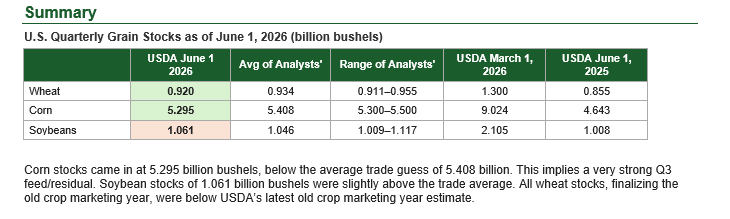

The dynamic data landscape started with a clear trend in old crop leftover supplies. The grain stocks report exposed an aggressive consumption rate for corn, drawing down ending stocks faster than market analysts projected.

“Corn stocks as of June 1, 5.3 billion bushels, that was over 100 million smaller than the trade estimate,” Nelson said. “So, we now have three quarters in a row of very strong feed residual, so a little positive news there.”

Conversely, soy and wheat numbers highlighted opposite directions for old crop lines:

- Soybeans: “Just almost 1.1 billion bushels of old crop, a little larger than the trade expected,” Nelson noted.

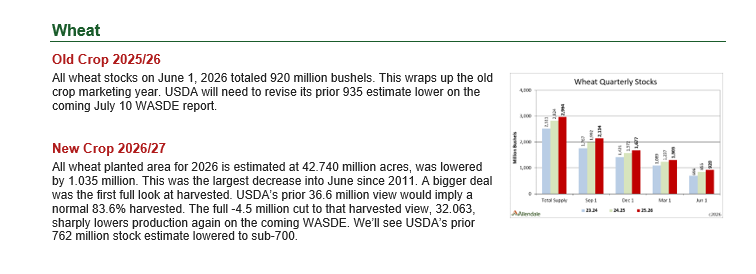

- Wheat: “USDA’s prior estimate for old crop ending stocks was 935… today, they finalized that with a 920. So a good 15 million bushel hit to that number.”

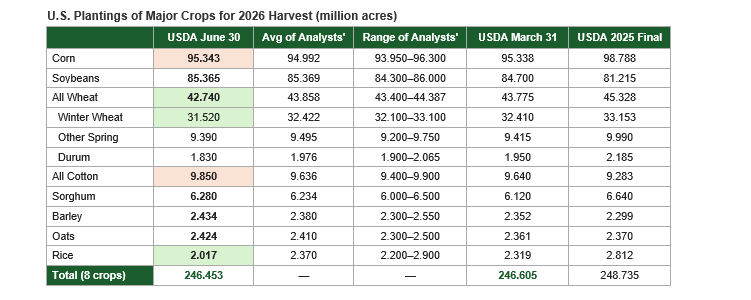

Total Acreage Shrinks Despite Replanting Theories

While regional concerns about winter wheat abandonment led some producers to hypothesize that unplanted acreage would shift toward heavy alternative row-crop varieties, aggregate acreage actually contracted.

“On this report, well, USDA lightly lowered a crop total acreage,” Nelson explained. “So 246.5 million, just minimally lower than the March estimate… this is about 2 million lower than last year’s.”

This unexpected stabilization disproved speculations about an influx of late-season minor crops.

2026 KEY ACREAGE SUMMARY

+------------------+--------------------+--------------------+

| Crop | Reported Acreage | Change vs. March |

+------------------+--------------------+--------------------+

| Corn | 95.3 Million | No Change |

| Soybeans | 85.4 Million | +700,000 Acres |

| Sorghum | 6.3 Million | +150,000 Acres |

+------------------+--------------------+--------------------+

Sorghum and Minor Crops Hold Steady Against Drought Expectations

Due to regional weather conditions across the Plains, rumors circulated that drought-tolerant sorghum would see a large expansion in acreage. However, the data revealed a much more subdued shift.

“Not a big increase,” Nelson emphasized. “The sorghum side of things, they saw a net increase of about 150,000 acres, so bringing it to 6.3 million. So, that was one big question for us, so not really a big sorghum increase.”

Nelson also brought attention to the long-term trend, noting that “this is still a net decline. We’re at 6.3 now; last year was 6.6… so still a net drop on that side.” Minor crops like barley and oats similarly showed only minimal gains, failing to support a major regional acreage resurgence.

Critical July Weather Holds the Key to Yield Trends

Looking past the baseline acreage data, the conversation shifted toward weather and its immediate impact on structural yield potential. Mid-July temperatures and moisture levels remain the premier focus for the primary producing states.

“For the Midwest states, they’re doing about 83% of corn and soybean production,” Nelson stated. “They are dealing with this high temperature story for July. They’re actually okay for now. As long as rains remain above normal for July, which is the current short-term forecast, we can argue yields lightly above trend for corn and soybeans.”

However, if these moisture patterns do not persist, current yield assumptions will require swift re-evaluation. “If that forecast changes, then we immediately remove the above-trend story, and therefore we can have higher prices,” Nelson added, while cautioning that it “doesn’t really mean we’re going to get a lot of fix though for the Plains… we certainly have in some areas still a drought in place.”

International Pressures: “Godzilla El Niño” Risks Dominate Global Supply

On the global stage, atmospheric changes are poised to impact international exporters. The presence of a severe El Niño pattern signals direct production risks for key regions across both hemispheres.

“El Niño typically means dryness for India, Southeast Asia… as well as Australia,” Nelson explained. “So that means India and Australia for lower wheat potential. And this means Southeast Asia for that Indonesia and Malaysia palm oil production.”

Conversely, South American growing regions could face a completely different operational challenge from the same system. “El Niño typically brings above-normal moisture to Argentina,” Nelson remarked. “And the thing we’re watching for is, typically it means more rain than needed and actually a yield detriment. So our main focus is perhaps in the second half of the year, we might have some support for these U.S. prices based on concerns with production.”

Cotton Gains Acreage at the Expense of Rice

Domestically, shifting dynamics in the Southern regions showcased how competitive market prices and local weather conditions altered final planting selections.

“Cotton acreage actually rose about 200,000 from that prior March estimate,” Nelson observed. “So cotton still sees a net increase of over a half million on this discussion. So higher cotton, despite the fact we had concerns about drought.”

This growth directly impacted competing regional options. “The rice side of things, which had an even worse drought story, we saw those acres drop by 300,000,” Nelson noted. This created an interesting dynamic of “lower rice by about 300,000, a net increase into cotton of about 200,000.”

Preparing for the July WASDE Report

Looking ahead to the upcoming July WASDE report, these updated acreage positions will directly reframe domestic balance sheet expectations. Nelson target-focused where the immediate revisions will hit first.

“Typically, we’re going to see mainly changes to the old crop story,” Nelson noted. “On the corn side, we will have higher feed residual posted for old crop… and we also will see lower old crop ending stocks due to the fact that exports are still wildly beating USDA’s hopes.”

While the old crop adjustments will tighten the corn ledger, the soybean balance sheet faces a completely different supply outlook. “When you throw these extra acres on the new crop side for soybeans, this balance sheet is going to look a little heavy,” Nelson warned. “You can now argue numbers to 400 [million], or maybe just a little above, so that new crop soybeans balance sheet will look a little tough.”

Ultimately, the market will continue to trade its own assumptions ahead of official adjustments. “The market is trading its own yield numbers right now, as it always does,” Nelson concluded. “The market is trading above-trend yields, even though USDA won’t show that for corn and soybeans.”

For those looking for more insight or additional data, contact Allendale at 1-800-2MARKET or visit their website at allendalehub.com.