The agricultural commodity markets are navigating a complex landscape of international conflict and domestic weather challenges as the 2025/26 marketing year progresses. In his latest analysis, Dr. Todd Hubbs from Oklahoma State University notes that February ended with “hostilities breaking out once again in the Middle East.” This shift impacted a week that had otherwise seen strength building in agricultural markets due to demand and potential weather issues, causing prices to retreat this past Monday.

“The duration and severity of the conflict remain uncertain,” Hubbs stated. “If the conflict spreads into other regions of the Middle East, the impact on markets could be extended and more severe than expected.” Currently, impacts on maritime trade routes in the region are already limiting movement into the Gulf of Arabia.

Wheat Market: Geopolitics and Persistent Dryness

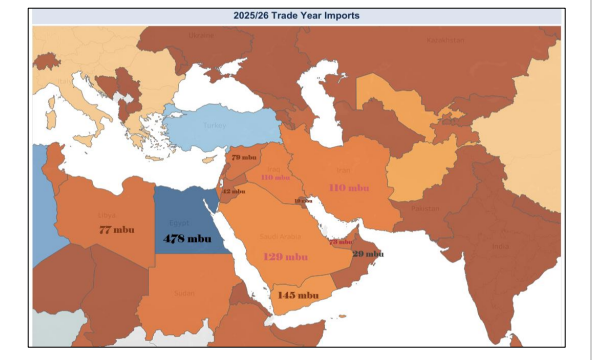

According to Hubbs, “Geopolitics and weather underpin wheat market activity at present.” The escalation of hostilities with Iran is occurring in a region that constitutes large demanders of wheat in the global market. Middle East nations account for over 700 million bushels of trade year imports for 2025/26. Hubbs highlighted that the threat to shipping in the Arabian Gulf via the Strait of Hormuz impacts oil and all bulk shipping, adding, “The impact on wheat markets if the conflict spreads to interference in the Red Sea could be quite profound.”

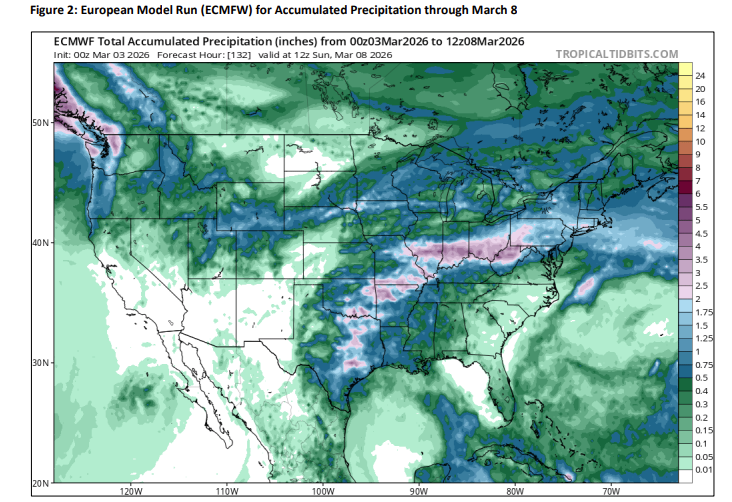

Domestically, dryness remains a prominent issue. While recent model runs have pushed potential moisture further west in Oklahoma, Hubbs remains cautious. “For clarity, my faith in weather models outside of three days is quite low,” he said. Recent conditions for winter wheat show that 50 percent of the acreage is in a level of drought, with abnormally dry areas expanding. “The light totals predicted in western Oklahoma and Kansas are lacking for the level of need,” Hubbs noted.

In the markets:

- HRW Export Pace: Total commitments through February 19 stand at 296 million bushels, which is 91.2 percent of the USDA’s forecast.

- Pricing: May HRW futures closed at $5.75 on Monday. Hubbs pointed out that Oklahoma prices maintain a basis of 80 under cash price and 50 under harvest price for most locations.

Corn and Milo: Demand Strength and Upcoming Reports

Corn demand strength continued through February, but Hubbs looks toward the end of March for more clarity. “March will see significant speculation on 2026 acreage and feed/residual usage with a resolution starting on March 31 with the release of USDA reports,” he explained. “Those reports will set the tone for corn prices throughout the spring.”

Corn Market Highlights:

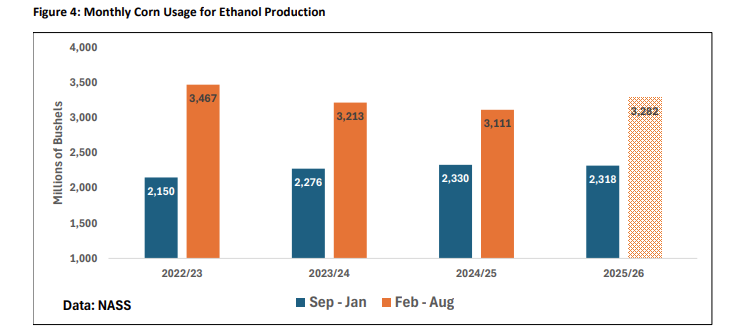

- Ethanol: Corn usage for ethanol totaled 2.318 billion bushels through the first five months of the marketing year. Hubbs notes that the remaining seven months require 3.28 billion bushels to meet USDA’s forecast, which “implies an extremely strong ethanol export program or an increase in ethanol blending.”

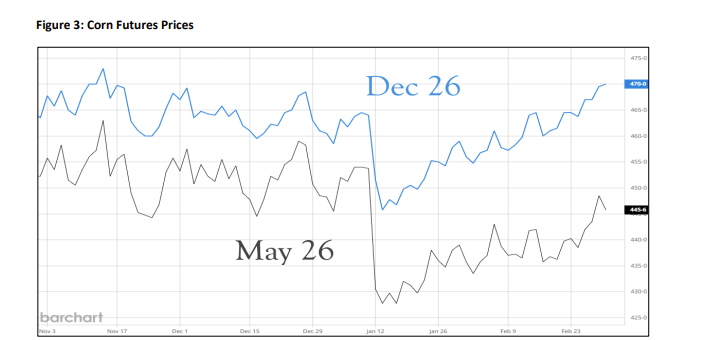

- Futures: December corn futures closed Monday at $4.70, with Oklahoma cash prices for new crop delivery settling between $4.30 and $4.35.

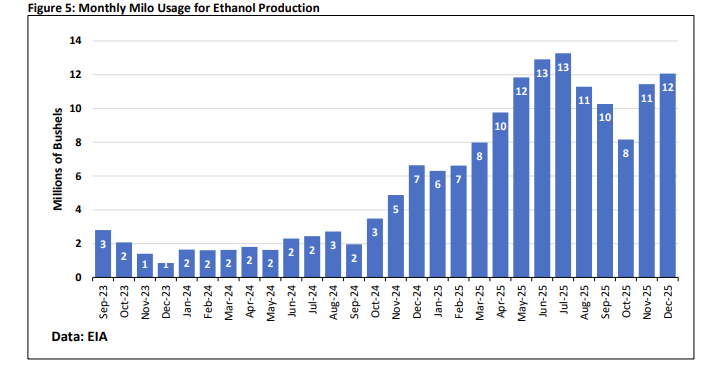

Milo Market Trends: Milo remains dependent on the export market and corn price competitiveness. Hubbs reported that milo basis is “quite weak,” with cash prices ranging from $3.34 to $3.44. China remains the only major player in U.S. milo export markets, and while industrial usage was up in December, the outlook remains tied to international trade. “Recent developments on the geopolitical front add more uncertainty to this outcome,” Hubbs concluded.